Fact-checked by the MyFinancial101 editorial team

Quick Answer

A single mom earning $55,000/year can pay off $18,000 in debt without a second job by identifying roughly $500–$750/month in budget surplus, applying the debt avalanche method to save up to $1,200 in interest, directing annual tax credits and refunds directly to balances, and maintaining a $1,000 emergency buffer to avoid recharging debt mid-payoff.

Paying off debt on a single income is a math problem with real solutions, but the margin is tight. A woman earning $55,000 as a head-of-household filer takes home roughly $3,600–$3,900 per month after federal and payroll taxes, depending on her state. According to Debt.org’s analysis of Bureau of Labor Statistics 2024 data, the median full-time yearly wage for women is $55,244, which means this scenario describes a real and common financial situation, not an optimistic outlier.

What makes it difficult is not the $18,000 balance. It’s the cost structure of raising a child alone: no partner to split rent, no backup income when something breaks, and no easy line item to cut. This article walks through how to find a workable surplus inside a single-income household budget, which tax credits at this income level can accelerate a payoff timeline, and why a second job is often not the right move when childcare costs are factored in.

Key Takeaways

- The median income for single-mother-led families is $41,305, well below the $55K threshold where structured debt payoff becomes achievable with deliberate budgeting (Single Mother Guide, 2025).

- The average APR on credit card balances is 21.52% as of Q1 2026, making interest-rate order of payoff a decision worth hundreds of dollars, not just a stylistic preference (LendingTree, citing Federal Reserve G.19 data, 2026).

- A single mom at $55K with one child can realistically generate a combined tax benefit of $3,000–$6,000 per year through the Child Tax Credit, EITC, and Child and Dependent Care Credit, applied directly to debt, this covers 17–33% of an $18K balance in one payment.

- People who maintain zero savings buffer during debt payoff take an estimated 40–60% longer to finish because unexpected expenses force new credit charges, erasing months of progress.

- The average non-mortgage consumer debt per American reached $21,603 as of late 2025, underscoring that an $18K balance sits below the national average and is fully payable within 24–30 months on a structured plan (The Motley Fool, citing Experian 2025 data).

In This Guide

- What $55K Actually Looks Like After Taxes and Childcare

- Getting Clear on Every Dollar Owed Before Touching the Budget

- Building a Budget That Works Around Kids, Not Against Them

- The Specific Cuts That Freed Up $500+ Per Month

- Tax Credits and Benefits She Was Already Entitled To

- Why She Didn’t Take a Second Job, and What She Did Instead

- How She Stayed on Track Without Burning Out

What $55K Actually Looks Like After Taxes and Childcare

At $55,000 gross, a head-of-household filer pays a lower effective federal tax rate than a single filer at the same income, but payroll deductions for Social Security, Medicare, and health insurance premiums still pull take-home pay down to roughly $3,600–$3,900 per month in most states. That’s the ceiling. Everything else comes out of it.

The Real Budget Squeeze

Housing, transportation, food, and childcare together consume 70–80% of take-home pay for most single-mother households. That leaves $400–$700 per month as the actual workable margin, and that number is what this entire article is about. According to the Single Mother Guide’s 2025 analysis of U.S. Census Bureau data, 31.3% of single-mother families live below the poverty line, and 36.8% experience food insecurity. At $55K, a single mom sits above those thresholds, but not by a margin that makes financial stress abstract.

One variable that shifted meaningfully in 2026: enhanced Affordable Care Act marketplace subsidies expired on December 31, 2025. A single mom who previously paid $80–$120/month for a marketplace plan may now pay $200–$350 or more for comparable coverage, depending on her state and plan tier. That $100–$200 monthly increase is real money against a $500–$700 surplus, and any debt-payoff plan that ignores it will underperform. Factor it in before setting a monthly payoff target.

The median income for single-mother-led families is $41,305, less than a third of the $132,959 median for married-couple families. At $55K, a single mom earns above the median for her peer group, which is precisely why a structured system can work where improvisation cannot.

Getting Clear on Every Dollar Owed Before Touching the Budget

Most people underestimate their total interest cost until they write every balance, rate, and minimum payment in one place. That single step, a debt inventory, is not administrative busywork. It’s the moment the problem becomes a solvable math problem rather than an ambient source of dread.

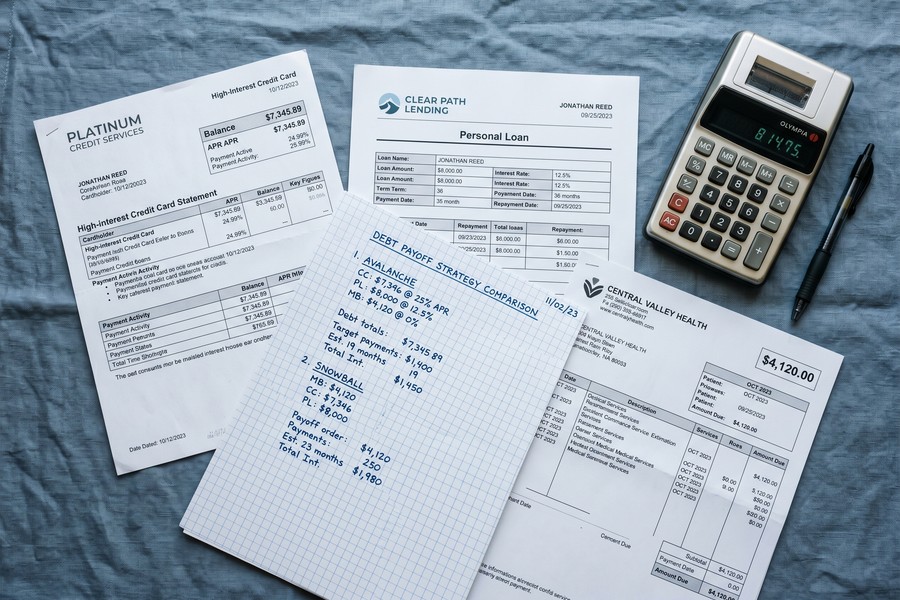

Snowball vs. Avalanche: The Dollar Difference on a Real $18K Balance

Consider a realistic $18K mix: a credit card carrying $7,000 at 22% APR, a personal loan with $8,000 at 12%, and a medical bill of $3,000 at 0% (most hospital systems will negotiate a zero-interest payment plan on request). The debt avalanche method, paying off the highest-rate balance first while making minimums on the rest, directs every extra dollar at the credit card first, then the personal loan, then the medical bill. The debt snowball method, paying off the smallest balance first for psychological wins, would target the medical bill first, then the personal loan, then the credit card.

On this specific balance mix, the avalanche saves approximately $800–$1,200 in total interest compared to the snowball, depending on how much monthly surplus is applied. The Consumer Financial Protection Bureau outlines both approaches, recommending that consumers keep paying minimums on all debts while directing any extra funds toward the priority debt. The avalanche is the better financial choice when the rate spread between debts is wide, as it is here. The snowball is defensible if motivation is the binding constraint, but that concession should be made with eyes open to its cost.

For a deeper look at negotiating down existing balances before you even start the payoff clock, the strategy guide on how to prioritize and negotiate with creditors covers the practical conversation with lenders.

Many single mothers delay the debt inventory step because the total feels shameful. It is not a character verdict. It is a number, and numbers can be worked with. Acknowledging the full balance is the precondition for every strategy that follows.

Building a Budget That Works Around Kids, Not Against Them

The standard 50/30/20 budget rule breaks down for single-income parents before you even get to the “wants” category. When childcare alone runs $800–$1,500 per month and housing eats 30–35% of gross income, needs consistently exceed 50% of take-home pay. A 60/20/20 or even 65/15/20 split, needs, wants, and debt/savings, is a more honest starting point for this income level.

The Line Items Generic Budgets Miss

Back-to-school clothes, school field trip fees, activity registration, and after-school program costs are not optional and not predictable month-to-month. They are mandatory and seasonal, which means a monthly budget that doesn’t account for them will blow up every August and September like clockwork. The fix is a dedicated irregular-expense line item: estimate annual child-related costs, divide by 12, and treat that amount as a fixed monthly expense, even in months when nothing is due.

Paycheck-by-paycheck budgeting, assigning every dollar of each paycheck to a specific purpose before it arrives, works better for single-income parents than monthly budgeting precisely because income and kid-related expenses don’t distribute evenly across a month. Software like YNAB or a simple spreadsheet both work; the method matters more than the tool. The constraint is clarity: every dollar needs a destination before it lands.

The Specific Cuts That Freed Up $500+ Per Month

Canceling a streaming subscription saves $15. Finding a smaller apartment saves $300. Those are not equivalent levers, and most debt-payoff advice treats them as if they are.

The Big Three, Honestly

The cuts that actually generate $500/month in surplus come from housing, transportation, and food, in that order. Moving to a smaller apartment or a lower-cost neighborhood is disruptive and sometimes feels like failure. It is neither; it is a deliberate trade of space for financial progress. Paying off a car loan aggressively to eliminate that monthly payment removes a $250–$400 recurring obligation, which compounds the surplus available for debt. Cooking at home and packing lunch adds up to $200–$400 per month for many households, less glamorous than any other tactic, and consistently more effective than any micro-cut strategy. For concrete ideas on stretching a grocery budget without sacrificing meals, the guide on seasonal foods that keep grocery bills manageable has practical options.

Some cuts feel punishing. That’s honest. The right frame is a defined sprint of 18–24 months, not a permanent lifestyle. Framing it as temporary, with a clear end date tied to the debt payoff, makes the sacrifice sustainable in a way that open-ended deprivation is not.

| Cost Category | Before (Monthly) | After (Monthly) | Monthly Savings |

|---|---|---|---|

| Housing (smaller unit) | $1,450 | $1,100 | $350 |

| Food (home cooking + lunch) | $700 | $450 | $250 |

| Car loan (paid off early) | $320 | $0 | $320 |

| Subscriptions + extras | $120 | $45 | $75 |

| Total monthly surplus freed | $995 |

Tax Credits and Benefits She Was Already Entitled To

Tax credits at this income level are a legitimate debt-payoff accelerator. For 2026, a single mom with one qualifying child can claim the Child Tax Credit of $2,200, the Child and Dependent Care Credit covering 20–35% of up to $3,000 in care expenses, and the Earned Income Tax Credit, which for one child phases out above $49,084 for single filers, meaning a $55K earner may not qualify for the EITC at this income level and should verify her specific situation with a tax professional or a free IRS free filing resource before counting on it.

One benefit that goes almost entirely unmentioned in single-mom debt advice: the Dependent Care FSA. Contributing up to $7,500 pre-tax in 2026 to a DCFSA reduces taxable income directly, lowers the federal tax bill, and effectively frees up cash that can be redirected to debt payoff. On a $55K salary, a full $7,500 DCFSA contribution can reduce taxable income enough to generate $900–$1,500 in additional take-home resources over the year. That’s real payoff acceleration that requires no lifestyle change, only enrollment during open benefits season.

The benefits cliff is a real planning variable at this income level. A raise, a bonus, or a one-time payment could push a single mom over eligibility thresholds for state childcare subsidies or other assistance. Before accepting a raise or applying a windfall, it’s worth checking whether the income increase nets out positively after subsidy changes. The article on rising 2026 poverty guidelines and who qualifies for benefits covers the current thresholds in detail.

Apply the full annual tax refund directly to debt the week it arrives. On an $18K balance, a $4,000 refund applied in February reduces the remaining principal by 22% in a single payment, the equivalent of eight months of $500 surplus contributions, without eight months of sacrifice.

Why She Didn’t Take a Second Job, and What She Did Instead

The second job is the default recommendation in almost every debt-payoff article. For a single mom without a co-parent, it frequently doesn’t pencil out. A second job paying $15/hour for 10 hours per week generates $600/month gross. If covering those hours requires paid childcare at $12–$18/hour, the net gain ranges from $0 to roughly $120/month, less than what careful grocery planning produces, at a far higher personal cost.

Found Money as a Real Accelerator

The more effective moves were one-time and structural rather than ongoing. Selling unused household items, furniture, electronics, children’s clothes they’ve outgrown, generated $800–$2,000 in lump-sum payments that came straight off the highest-interest balance. Negotiating a raise at her existing job, or targeting a role with a higher salary at a new employer, increased income without adding hours. And redirecting windfalls, tax refunds, a small bonus, a birthday check, entirely to debt rather than absorbing them into spending shaved an estimated 6–9 months off the payoff timeline.

If additional income is genuinely needed without childcare costs, flexible options like micro-freelancing through platforms that allow asynchronous remote work can generate $200–$500/month on a child’s school schedule. The overview of how micro-freelancing has expanded as an income option covers realistic earning ranges and platform options. The key condition: the hours must not require paid childcare coverage to offset them.

How She Stayed on Track Without Burning Out

An $18K payoff on a $500–$750/month surplus takes 24–36 months without windfalls, or 18–24 months with them. Motivation collapse is the most common reason people stop midway, not insufficient income, not poor strategy.

The Emergency Buffer Question

Maintaining a $1,000 emergency buffer throughout the payoff period is not a detour from the plan. It is the plan. Without it, a single car repair or an unexpected medical bill forces new credit card charges at the current average APR of 21.52%, erasing months of progress and extending the payoff timeline by the 40–60% that research consistently shows. The buffer is funded first, before debt payoff begins, and replenished immediately if used.

The National Foundation for Credit Counseling recommends that the first step for anyone carrying debt is a full financial review with a nonprofit credit counselor, particularly useful for single-income households with limited margin. A Debt Management Plan through an NFCC member agency can reduce interest rates and consolidate payments, which is worth evaluating if high-interest debt is consuming more than 15% of take-home pay each month. Before engaging any debt-relief company, the Federal Trade Commission’s consumer guidance on debt relief identifies the warning signs of services that take fees without delivering results.

Milestone rewards, something small and budget-friendly after every $3,000–$5,000 paid off, are a documented motivational tool, not an indulgence. A $25 dinner, a movie night, a day trip. The framing matters: the reward is a recognition that the system is working, not a break from it. And when the final payment clears, the monthly surplus that was going to debt goes directly into a starter emergency fund the following month. The same discipline that paid off $18K in debt is the same discipline that builds the financial cushion that prevents the next $18K from ever accumulating.

According to Experian’s 2025 consumer debt report, the average total debt per person, including mortgages, reached $105,444. An $18K non-mortgage balance, while significant, is a tractable target with a structured repayment plan and the right payoff order.

After the debt is gone, the redirect is immediate: the same $600/month that was going to balances goes into a 3-month emergency fund, then toward a workplace 401(k) contribution large enough to capture any employer match, then toward longer-term goals. For readers thinking about what sequencing looks like beyond debt payoff, the guide on how to start investing with no prior experience covers the first realistic steps for a $55K income household.

Frequently Asked Questions

Can you really pay off $18K in debt on a $55K salary without a second job?

Yes, but only with a surplus of $500–$750 per month consistently applied. At $55K gross filing as head of household, take-home pay runs roughly $3,600–$3,900/month depending on state; the strategy is about identifying that surplus through housing, food, and transportation changes, then protecting it with a $1,000 emergency buffer so unexpected expenses don’t reverse progress. With annual tax credit windfalls applied directly to debt, the timeline shortens to 18–24 months.

Which is better for a single mom, the debt snowball or the debt avalanche?

On a mixed $18K balance with a high-interest credit card, the avalanche method saves $800–$1,200 in total interest. The snowball is worth considering if maintaining motivation is the primary obstacle, but that trade-off should be made deliberately. The CFPB recommends continuing minimum payments on all debts while directing any surplus to the priority balance, regardless of which method you choose.

What tax credits can a single mom at $55K claim in 2026?

At $55K with one qualifying child, the Child Tax Credit ($2,200), the Child and Dependent Care Credit (20–35% of up to $3,000 in care costs), and the Dependent Care FSA (up to $7,500 pre-tax) are all available. Eligibility for the Earned Income Tax Credit depends on exact adjusted gross income and number of children; at $55K with one child, a single filer may fall above the EITC income limit, so verification with a tax professional is advisable before relying on that figure.

Is a debt consolidation loan a good option for paying off $18K on a single income?

It depends entirely on whether spending can be controlled first. The CFPB advises that consolidation does not help if spending exceeds income, because the underlying imbalance remains. If a single income genuinely covers all expenses with a surplus, a consolidation loan at a lower rate than the existing credit card APR can reduce total interest cost and simplify payments, but it is not a substitute for the budget work.

How does the benefits cliff affect a single mom trying to increase income at $55K?

At this income level, a raise, bonus, or tax refund can push household income over state eligibility thresholds for childcare subsidies or assistance programs, potentially reducing total resources even as gross income rises. Any income increase should be evaluated against current benefit eligibility before being accepted or applied, a net gain is not guaranteed. Checking the current 2026 federal poverty guidelines and your state’s specific subsidy thresholds before acting is the right sequence.

What should happen to the monthly debt payment after the last balance is cleared?

The same amount goes immediately into a 3-month emergency fund the following month, no lifestyle adjustment, no “treating yourself” with the full surplus. Once the emergency fund reaches 3 months of essential expenses, the amount redirects to a retirement contribution sufficient to capture any employer 401(k) match. The discipline that cleared the debt is what builds the financial stability that follows.

Sources

- Consumer Financial Protection Bureau, How to Reduce Your Debt

- Consumer Financial Protection Bureau, What to Know Before Consolidating Credit Card Debt

- Federal Trade Commission, Credit, Loans, and Debt Consumer Advice

- National Foundation for Credit Counseling, Which Debt Repayment Method Is Right for You?

- Single Mother Guide, Single Mother Statistics 2025 (citing U.S. Census Bureau data)

- LendingTree, Credit Card Debt Statistics 2026 (citing Federal Reserve G.19 data)

- Experian, How to Get Out of Debt: A Step-by-Step Guide