Fact-checked by the MyFinancial101 editorial team

The Verdict

Maxing out a Roth IRA on a $55,000 teacher salary is realistic if you can redirect $625 per month toward the account, roughly 14% of after-tax take-home pay. It stops making sense only if high-interest debt or a missing emergency fund demands attention first. Most teachers hit the threshold faster by pairing budget cuts with a single income boost.

The biggest misconception about trying to max out a Roth IRA is that it requires a six-figure income. On a $55,000 gross salary, federal and state taxes, a pension contribution of roughly 8–10%, and health insurance premiums leave a teacher with somewhere between $3,400 and $3,700 per month in take-home pay. The IRS 2026 annual Roth IRA contribution limit of $7,500 divided over 12 months equals $625 per month. That is roughly 17–18% of take-home pay, tight but achievable without extreme sacrifice.

Rates on savings accounts are no longer the free gains they were in 2023 and 2024, and market volatility has rattled even experienced investors. That is precisely why locking in tax-free growth through a Roth IRA matters more now, not less.

| Factor | Reasons to Max Out Roth IRA on $55K | Reasons to Wait or Contribute Less |

|---|---|---|

| Tax treatment | Contributions grow tax-free; qualified withdrawals never taxed | Benefit is delayed, won’t matter for 20+ years |

| Income eligibility | $55K is well below the $153,000 phase-out for single filers in 2026 | A significant salary increase could phase you out later |

| Monthly cost | $625/month is under 18% of a $3,500 take-home | Leaves limited buffer for irregular expenses or emergencies |

| Flexibility | Contributions (not earnings) can be withdrawn penalty-free anytime | Earnings are locked until age 59½ without a 10% penalty |

| Pension overlap | Roth IRA adds tax diversification alongside a defined-benefit pension | Teachers with strong pension tiers may have genuinely less need |

| Debt situation | Worth prioritizing over extra mortgage payments at low rates | High-interest credit card debt (above 7%) should come first |

| Compounding timeline | A teacher at 30 has 30+ years for tax-free compounding to work | Starting in your late 50s compresses the payoff window significantly |

Key Takeaways

- Your gross income is below $153,000 as a single filer, making you fully eligible for Roth IRA contributions in 2026

- You can consistently free up at least $625 per month after housing, food, transportation, and minimum debt payments

- Housing costs stay below 25% of your monthly take-home pay

- You have or are building a 3-month emergency fund simultaneously, Roth contributions should not replace this

- Any high-interest debt (credit cards above 7% APR) is already under a payoff plan or eliminated

- You have access to at least one income supplement, a stipend, side work, or annual tax refund, worth $2,000 or more per year

- You are willing to automate contributions so the money moves before you can spend it

What Does $55K Actually Leave You to Work With?

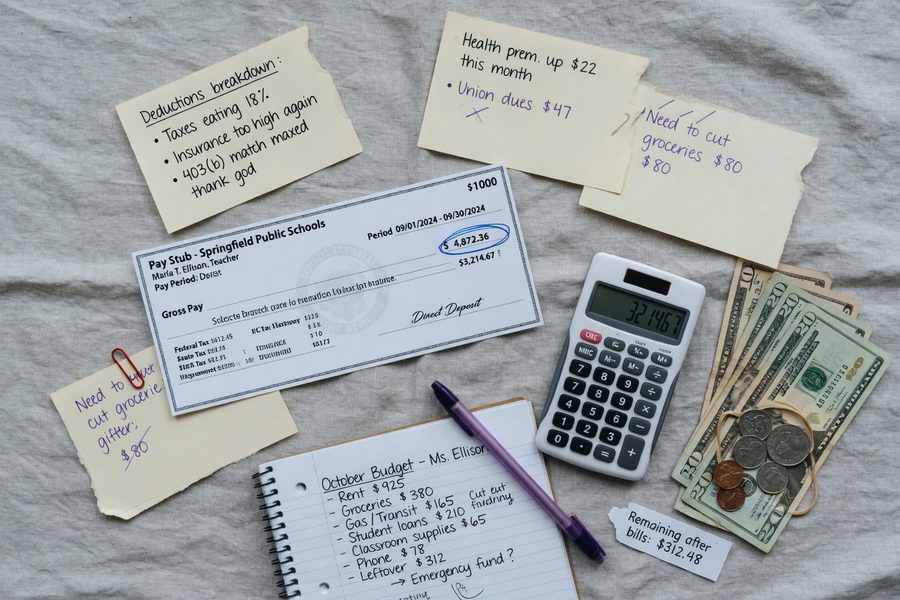

After realistic deductions, a $55K teacher salary produces about $3,450–$3,600 per month in spendable income, and that math changes everything about whether $625/month is crushing or doable. A typical public school teacher in a mid-cost state pays roughly $400–$500 monthly in combined pension and health insurance premiums before federal and state income tax hits. Federal income tax at this wage bracket runs approximately $350–$430 per month. The result: somewhere between $3,400 and $3,700 lands in the checking account each pay period cycle.

Run the actual arithmetic: $7,500 per year divided by 12 equals $625 per month. Against a $3,500 take-home benchmark, that is 17.9%. It leaves $2,875 for everything else. That sounds thin. It is not impossible, but it does require housing costs below $875 (25% of take-home), which is realistic in lower cost-of-living districts and many suburban teaching markets. Teachers living in high-cost metros face a harder version of this problem and may need the income boost strategy described later.

One detail most articles skip: teachers on 10-month contracts who elect to receive pay only during the school year get larger monthly checks than colleagues spread across 12 months. That structure can actually help, because the summer gap forces a planning discipline that prevents lifestyle drift.

The Budget Cuts That Actually Freed Up $600 Per Month

Three categories do most of the work: housing, transportation, and food. Cutting across all three is more effective than slashing any single one. A teacher paying $800 in rent (or a mortgage PITI under $900), driving a paid-off car, and keeping groceries and dining combined under $400 per month can reach $625 in Roth contributions without touching other spending. That is the model, not a fantasy scenario.

Here is a concrete monthly snapshot for a single teacher earning roughly $55K gross and taking home $3,500:

- Rent or mortgage: $850

- Transportation (car payment, insurance, gas): $320

- Groceries and household supplies: $300

- Utilities and internet: $175

- Dining out and entertainment: $100

- Subscriptions and miscellaneous: $80

- Emergency fund top-up or sinking funds: $50

- Roth IRA contribution: $625

- Remaining buffer: $0–$100

That buffer is real. It is also thin. The budget above works because it front-loads savings and treats the Roth IRA contribution as fixed, not optional, before any discretionary dollars are counted. Automation is the mechanism that makes this stick. Setting up an automatic monthly transfer to a brokerage like Fidelity or Vanguard on payday means the $625 never sits in a checking account where it can be spent.

Cutting dining out to $100 per month sounds aggressive. In practice, it means cooking at home most nights and using strategies like coupon stacking to beat grocery inflation, which can cut a food budget by $50–$100 per month with minimal effort. For teachers who find subscription costs ballooning, using the library to replace paid streaming and media services is a zero-sacrifice swap worth $30–$60 monthly.

Do Teachers Actually Earn Enough Extra to Speed This Up?

Yes, and the sources are more common than most outside the profession realize. Coaching stipends typically run $1,500–$4,000 per season. Department head stipends often add $2,000–$3,500 annually. Tutoring outside school hours at $40–$75 per hour is straightforward to pick up, particularly in math and science. Summer school contracts pay a separate daily rate on top of the base salary. For teachers looking for additional income options beyond the classroom, local school and event jobs are an underused path that does not require a second career.

The strategy that compresses the timeline from five years to under three: redirect every dollar of windfall or supplemental income directly into the Roth IRA. A $2,500 tutoring income in a given year covers four months of Roth contributions instantly. A $1,800 federal tax refund covers nearly three. A $1,200 coaching stipend covers almost two. Stack those in a single year and the regular $625 monthly contribution needs to carry only the remaining gap.

One overlooked source specific to educators: tuition reimbursement. Many districts reimburse graduate coursework, which frees dollars that would otherwise go to student loan payments or out-of-pocket education costs. That freed cash can be rerouted to the Roth IRA without changing gross spending habits at all. Even the micro-freelancing economy offers teachers a realistic path to $200–$500 extra per month through curriculum design, online tutoring platforms, or test prep work.

Front-Load or Monthly: Which Contribution Strategy Wins?

Monthly contributions beat waiting for a lump sum in almost every real-world scenario for a teacher at this income level. Front-loading, depositing the full $7,500 in January, gives the money more time in the market, but it requires having $7,500 liquid at the start of the year, which most teachers on $55K do not. The cost of waiting to save a lump sum is higher than the cost of monthly dollar-cost averaging.

The IRS contribution eligibility rules confirm that single filers with a modified adjusted gross income below $153,000 in 2026 can make the full Roth IRA contribution. At $55K, there is no phase-out concern. The full $7,500 is available regardless of contribution timing.

Inside the account, a single low-cost index fund, a total market fund or an S&P 500 fund through Fidelity, Vanguard, or Schwab, handles the investment decision for most teachers at this stage. Expense ratios on flagship index funds at these providers run as low as 0.03% annually. Over a 30-year horizon, that difference in cost between an index fund and an actively managed fund compounds to tens of thousands of dollars. Keep the investment choice simple. The account mechanics matter far more than the specific holdings at this income and timeline.

For teachers who already have access to a 403(b) or 457(b) through their district, the Roth IRA still deserves priority for one reason: flexibility. Roth IRA contributions, not earnings, just what you put in, can be withdrawn at any time without penalty. That flexibility matters during a career that may include moves, family changes, or a gap year. The pension is the anchor. The Roth IRA is the portable, tax-free supplement. If you want to understand how Roth IRA stacks up against other investment options early in your journey, this beginner investing guide covers the core tradeoffs without overwhelming jargon.

Who Should and Who Should Not

Good candidates

Teachers who can hit the checklist above without eliminating their emergency fund are strong candidates for maxing out right now.

- A single teacher, age 25–40, earning $50K–$65K in a district where rent is below $900 per month, the contribution math works cleanly with room for one income supplement

- A teacher with a paid-off car, no consumer debt, and a 3-month emergency fund already in place, the $625/month flows to the Roth without structural budget risk

- Any teacher receiving a coaching stipend, department chair supplement, or tuition reimbursement, that extra income makes it easy to contribute an additional $1,500–$3,000 annually beyond the monthly automatic transfer

- Teachers who already contribute to a district 403(b) or 457(b) but want tax-free withdrawal flexibility later, the Roth IRA adds a layer that a traditional pension and pre-tax plan cannot replicate

Who should skip it

Some situations genuinely call for a different priority order, and forcing the Roth IRA contribution in these cases creates more financial risk than it solves.

- A teacher carrying credit card balances at 20%+ APR, paying down that debt first delivers a guaranteed 20% return, which beats any projected market gain; see how to prioritize and negotiate credit card debt before redirecting cash to retirement accounts

- A teacher with less than one month of expenses saved, an unexpected car repair or medical bill would trigger either Roth withdrawal (losing tax-free growth) or high-interest borrowing

- A teacher in a high cost-of-living metro where rent alone exceeds 40% of take-home pay, the arithmetic does not work without a significant second income

- Anyone within five years of retirement who expects pension income to cover most expenses, the Roth’s core advantage (decades of tax-free compounding) is compressed, and paying off remaining debt may produce better retirement cash flow

Frequently Asked Questions

Can a teacher on $55K really max out a Roth IRA without a side hustle?

Yes, in lower cost-of-living areas where housing stays below 25% of take-home pay. The monthly requirement is $625 toward the 2026 limit, achievable on a lean budget without supplemental income. A side hustle simply accelerates the timeline or creates a buffer when months run short.

Does a teacher pension affect Roth IRA eligibility?

Pension contributions reduce take-home pay but do not affect Roth IRA eligibility. Eligibility is based on modified adjusted gross income, not net pay. A teacher earning $55K gross remains well below the $153,000 single-filer phase-out threshold set by the IRS for 2026.

What happens to Roth IRA contributions during summer if a teacher has no income?

Nothing happens automatically, contributions pause unless you front-loaded earlier in the year. Teachers on 10-month pay structures who receive checks only September through June need to contribute $750 per month during those 10 months rather than $625 spread over 12, or keep a cash buffer from the school year to cover summer contributions. The IRS requires only that total contributions not exceed annual earned income, summer gaps do not disqualify previous contributions.

Is a Roth IRA better than a 403(b) for teachers?

For most early-career teachers, the Roth IRA wins on flexibility, contributions can be withdrawn penalty-free at any time, which a 403(b) does not allow. A 403(b) with an employer match changes the calculus: capture the full match first, then fund the Roth IRA. If your district offers no match, the Roth IRA typically comes first because of its tax-free growth and withdrawal advantages. Thinking through whether to prioritize retirement savings over other long-term goals is a related decision worth making explicitly.

Sources

- Internal Revenue Service, 401(k) Limit Increases to $24,500 for 2026, IRA Limit Increases to $7,500

- Internal Revenue Service, Retirement Topics: IRA Contribution Limits

- Internal Revenue Service, Amount of Roth IRA Contributions You Can Make

- Investment Company Institute, U.S. Retirement Assets Q4 2025 Statistical Report

- NerdWallet, Roth IRA Contribution and Income Limits 2026

- Consumer Financial Protection Bureau, An Essential Guide to Building an Emergency Fund

- U.S. Department of Labor, Understanding Retirement Plan Fees and Expenses

- Bureau of Labor Statistics, Occupational Outlook Handbook: Elementary and Middle School Teachers