Fact-checked by the MyFinancial101 editorial team

Quick Answer

The sinking fund strategy works by dividing a known future expense by the months until it’s due, then saving that amount automatically each month. For example, a $1,200 annual car insurance bill becomes just $100 per month. Most beginners can build their first sinking fund fully funded within 6 to 12 months by identifying categories, calculating contributions, and automating transfers to a separate account.

A sinking fund is a dedicated savings bucket you fill gradually to cover a specific, predictable future expense, and the sinking fund strategy for beginners is one of the most practical shifts you can make to stop treating normal life costs like financial emergencies. The concept is simple: divide what you’ll owe by the months remaining, save that slice every payday, and the bill arrives already paid. According to Bankrate’s 2026 emergency savings report, 24% of Americans have no emergency savings at all, and a large part of why people drain what little cushion they have is that they’re using emergency funds to pay for expenses that were never actually surprising.

That pattern is getting harder to sustain. Insurance premiums, car maintenance, and home repair costs have all climbed steadily over the past several years, meaning the gap between what people budget monthly and what they actually spend annually keeps widening. The households that manage this gap most effectively aren’t necessarily earning more, they’re planning differently. Sinking funds are the tool that makes that planning concrete.

This guide is written for anyone who has ever ended a month confused about where the money went, or felt blindsided by a bill they technically knew was coming. By the end, you’ll be able to identify your categories, calculate exact monthly contributions, choose where to hold the funds, and build a system that runs with minimal effort once it’s set up.

Key Takeaways

- 24% of Americans carry no emergency savings at all, according to Bankrate’s 2026 report, sinking funds prevent the behavior that drains whatever savings do exist.

- Only 46% of Americans have enough saved to cover three months of expenses, per Bankrate (2026), meaning most households cannot absorb a large irregular bill without going into debt.

- A $1,200 annual insurance premium broken into $100 monthly contributions eliminates the lump-sum shock entirely and requires zero willpower once automated.

- Adding a 10% buffer to your calculated monthly amount protects against price increases, especially relevant in 2026, when insurance and utility costs continue rising faster than general inflation.

- High-yield savings accounts currently offer 3–5% APY, so sinking fund balances can earn modest growth while remaining fully accessible when the expense comes due.

- Sinking funds and emergency funds serve different purposes; mixing them, as many beginners do, is a primary reason emergency reserves get depleted by non-emergency costs.

In This Guide

- What Is a Sinking Fund and Why Beginners Need One

- Sinking Funds vs. Emergency Funds: What’s the Difference?

- How Do I Figure Out Which Sinking Fund Categories I Need?

- How Do I Calculate and Set Up My Monthly Contributions?

- Where Should I Keep Sinking Fund Money and How Do I Automate It?

- How Do I Track Progress and Avoid the Most Common Beginner Mistakes?

- Frequently Asked Questions

Step 1: What Is a Sinking Fund and Why Beginners Need One

A sinking fund is a savings account, or sub-account, designated for a single, known future expense. You name the expense, estimate the cost, divide by the months until it’s due, and contribute that exact amount each month until the bill arrives. The expense gets paid in full without touching your regular checking balance or your emergency fund.

The Core Concept

The name comes from accounting: businesses have long used “sinking funds” to retire debt or replace assets in an orderly way rather than scrambling when the obligation comes due. Personal finance borrows the concept for the same reason, replacing reactive scrambling with proactive planning. A car registration fee, a holiday gift budget, an annual streaming subscription: none of these are truly surprising, but without a sinking fund, they often feel that way.

The mindset shift this requires is subtle but real. Instead of asking “where am I going to find $800 for car registration?” you ask “how many months until this is due, and how much do I set aside each month?” That shift from reactive to scheduled changes your entire relationship with irregular expenses.

Why Beginners Specifically Benefit

If you’re new to budgeting, your first instinct is usually to track monthly spending, groceries, rent, utilities. But a significant portion of real-world spending happens in spikes: once a year, once a quarter, or every few years when an appliance breaks. Sinking funds are how you flatten those spikes into predictable monthly contributions. They work on any income level, though beginners earning under $50,000 annually may need to be selective at first about which categories they fund, prioritizing the largest or most certain costs and adding categories as their budget stabilizes.

The term “sinking fund” dates to 18th-century British government finance, where Parliament used dedicated funds to pay down national debt. The personal finance application is newer, but the logic is identical: commit small, regular amounts now so a large obligation doesn’t arrive as a crisis.

Step 2: Sinking Funds vs. Emergency Funds: What’s the Difference?

Sinking funds cover expenses you know are coming; emergency funds cover expenses you genuinely cannot predict. Confusing the two is one of the most damaging habits in beginner budgeting, because it turns a true safety net into a general-purpose slush account that never stays full.

Planned vs. Unplanned Costs

An emergency fund exists to absorb a job loss, a sudden medical diagnosis, or a car engine failure you had no warning about. According to Bankrate’s 2026 data, only 46% of Americans have enough emergency savings to cover three months of expenses, a fragile cushion that evaporates quickly when it’s used to pay for car insurance renewals or holiday travel that was scheduled all along.

A sinking fund, by contrast, covers your car’s annual registration, your homeowner’s insurance premium, your child’s back-to-school supplies, or the vacation you’re taking in October. You know these are coming. The only question is whether you save for them in advance or scramble for cash when the date arrives.

Why Mixing Them Backfires

When you use emergency savings to pay for predictable expenses, two things happen. First, your emergency fund balance stays perpetually low, which means a real emergency (a layoff, an ER visit) leaves you with almost no buffer. Second, you never develop the planning habit that sinking funds build, so the cycle repeats. If you’ve been struggling with credit card debt from irregular expenses landing without warning, separating your sinking fund from your emergency fund is often the structural fix that stops the cycle.

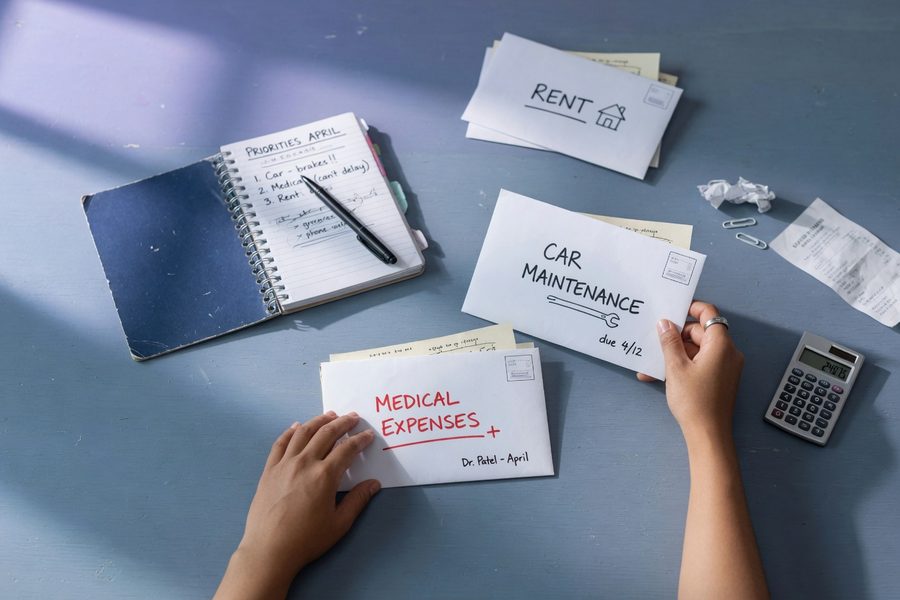

A clean rule: if you can write the expense on your calendar today with a dollar estimate, it belongs in a sinking fund. If you genuinely cannot know the when or the how much, it belongs in your emergency reserve.

Do not let your emergency fund do double duty as a sinking fund. Once you’ve depleted it for a car insurance payment, a real emergency, a layoff, an unexpected medical bill, will force you onto a credit card. Keeping these pots separate is what makes both of them work.

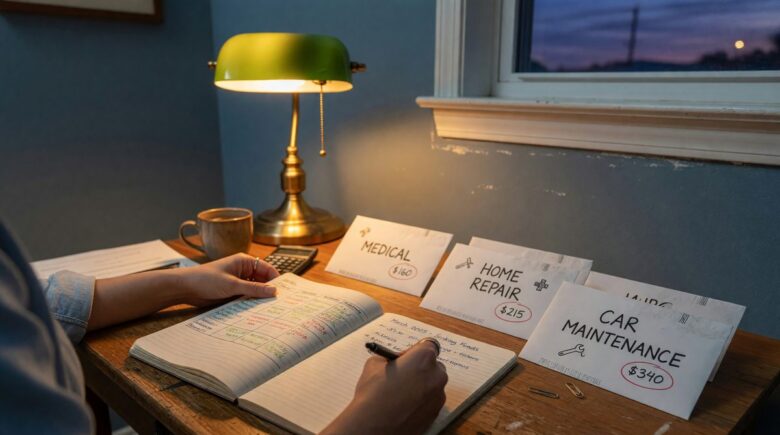

Step 3: How Do I Figure Out Which Sinking Fund Categories I Need?

Start by pulling three to twelve months of bank and credit card statements and highlighting every charge that didn’t happen in every single month. Those irregular charges are your sinking fund candidates.

Reviewing Your Statements

Most people, when they do this exercise, discover that their “unexpected” expenses follow a predictable calendar. Car repairs cluster in spring after winter driving wears down brakes and tires. Holiday spending spikes in November and December. Annual insurance renewals hit on the same date every year. The exercise converts vague anxiety about money into a specific list with dollar amounts attached.

Common beginner-friendly categories include:

- Auto insurance (annual or semi-annual premium)

- Car registration and inspection fees

- Home or renters insurance

- Holiday gifts and travel

- Vacations or planned trips

- Annual subscriptions (streaming bundles, software, warehouse memberships)

- Back-to-school or back-to-work expenses

- Routine car maintenance (tires, oil changes, wiper blades)

- Medical copays or dental work not covered fully by insurance

Prioritizing When Your Budget Is Tight

Don’t try to fund every category simultaneously in your first month. If you’re earning under $50,000 annually with high fixed expenses, start with two or three categories that carry the largest lump-sum amounts or arrive soonest. A $1,800 insurance premium due in four months is a higher priority than a $300 holiday budget due in eight. Fund the urgent and expensive first; add categories as your contributions become automatic and your cash flow opens up.

For beginners who are simultaneously working on paying down debt, the sinking fund strategy doesn’t have to compete with your repayment plan. If you’re using the debt snowball or avalanche approach to tackle credit card balances, sinking fund contributions for truly non-negotiable expenses (insurance, registration) can run in parallel at a minimal amount, then scale up once balances are cleared.

After your first 12 months of running sinking funds, revisit your category list every January. Insurance premiums, utilities, and maintenance costs tend to increase annually. Adjusting your monthly contributions at the start of each year, even by $5 or $10 per category, prevents a shortfall from catching you off guard at renewal time.

| Category | Typical Annual Cost | Monthly Contribution Needed | Priority for Beginners |

|---|---|---|---|

| Auto Insurance | $1,200 – $2,400 | $100 – $200 | High (non-negotiable) |

| Home / Renters Insurance | $600 – $1,800 | $50 – $150 | High (non-negotiable) |

| Holiday Gifts & Travel | $500 – $1,500 | $42 – $125 | High (date-certain) |

| Car Maintenance | $400 – $1,000 | $33 – $83 | Medium |

| Vacation / Travel | $800 – $3,000 | $67 – $250 | Medium (lifestyle goal) |

| Annual Subscriptions | $100 – $400 | $8 – $33 | Low (small amounts) |

| Appliance Replacement (multi-year) | $600 – $2,000 per appliance | $17 – $56 over 3 years | Low-to-medium (long horizon) |

Step 4: How Do I Calculate and Set Up My Monthly Contributions?

The formula is direct: take the total amount the expense will cost, divide it by the number of months until it’s due, then add 10% as a buffer. That final number is your monthly sinking fund contribution.

Here’s the arithmetic in plain terms. Suppose your car insurance premium is $1,200 and renews in 12 months. Divide $1,200 by 12 to get $100 per month. Add 10% ($10) for the buffer, and your actual monthly contribution is $110. Over 12 months, you accumulate $1,320, enough to absorb a modest premium increase at renewal without needing to find extra cash on short notice. The buffer matters more now than it did several years ago because insurance premiums in particular have climbed faster than general consumer prices, and a 5–8% increase at renewal is not unusual in 2026.

For multi-year sinking funds, an appliance you expect to replace in three years, or a home project you’re planning for five years from now, the same formula applies over a longer horizon. A $1,800 refrigerator replacement in 36 months costs you $50 per month plus a 10% buffer, or $55 per month. Starting early dramatically reduces the monthly burden and removes any urgency to finance the purchase when the time comes.

A household with a $1,200 annual car insurance bill that saves $100/month reaches the full amount with no financial stress. Add a 10% buffer ($10/month) and that same household has $120 in reserve for premium increases, accumulated at virtually no additional effort once the transfer is automated.

Step 5: Where Should I Keep Sinking Fund Money and How Do I Automate It?

The best place for sinking fund money is a high-yield savings account (HYSA) that you can label or sub-divide by category. As of mid-2026, competitive HYSAs offer between 3% and 5% APY, which means your car insurance sinking fund earns a few dollars in interest while it sits, modest, but meaningfully better than a standard savings account paying 0.01%.

Choosing Your Account Structure

Several online banks, including Ally, Marcus by Goldman Sachs, and SoFi, allow you to create multiple sub-accounts or “buckets” within a single savings account, each with its own label and running balance. This lets you hold all your sinking funds in one place without mixing the balances together. If your current bank doesn’t offer sub-accounts, a budgeting app like YNAB (You Need a Budget) or EveryDollar can track allocations virtually, even if the money physically lives in one account.

Keep sinking funds separate from your everyday checking account. The goal is friction: money that requires a deliberate transfer to access is money you won’t spend casually. You don’t need a separate bank, but you need a visible wall between spending money and saving money.

Automating the Contributions

Set up automatic transfers from your checking account to your sinking fund account on the day after your paycheck posts. Automation is not optional, it’s the mechanism that turns good intentions into reliable results. When the transfer happens before you have a chance to spend the money, the system runs on its own. If you’re looking for ways to boost income with micro-freelancing to fund these accounts faster, channeling that extra income directly into your sinking funds on receipt is the most effective use of irregular earnings.

Schedule your sinking fund transfers for the day after payday, not the last day of the month. Pay-yourself-first automation removes the behavioral risk entirely: you never see the money in checking, so you’re never tempted to spend it before the transfer happens.

Step 6: How Do I Track Progress and Avoid the Most Common Beginner Mistakes?

Tracking doesn’t need to be daily or complex. A monthly balance check, logging into your HYSA once a month to confirm each sub-account is on track, is all most people need. The real discipline comes in the adjustments and in avoiding the behavioral traps that derail beginner savers.

Simple Tracking Methods

A spreadsheet works well for beginners: one row per sinking fund, columns for the target amount, months remaining, monthly contribution, and current balance. Update it monthly in five minutes. Alternatively, the sub-account labels in your HYSA show the running balance at a glance. The key metric is whether your current balance equals your monthly contribution multiplied by the number of months you’ve been saving. If it’s lower, you’ve either been contributing too little or spending from the fund early.

Annual Adjustments for Inflation and Rising Costs

Review every sinking fund category once a year, ideally in January or whenever a renewal bill arrives. Insurance premiums in particular have risen significantly in 2026, and a contribution amount that was accurate last year may fall short this year. Add 5–10% to any category where costs have visibly increased, and fund that higher amount going forward. This annual recalibration is something most beginner guides skip, but it’s what separates a sinking fund system that holds up over time from one that starts to leak.

The Most Common Beginner Mistakes

Three mistakes appear most consistently:

- Underestimating the total, always check last year’s actual bill, not a round-number guess. Actual costs almost always exceed estimates.

- Raiding the fund early, spending from a sinking fund on a different expense than the one it was built for effectively resets your progress and leaves you short when the real bill arrives. Label your sub-accounts clearly so the purpose is always visible.

- Opening too many categories at once, five underfunded sinking funds are less useful than two fully funded ones. Build depth before width.

If motivation becomes an issue after the initial setup, a simple accountability tactic is tracking your total sinking fund balance as a single number and watching it grow. Small milestones, reaching half the target for your car insurance fund, for example, are worth noticing. Some people find a visual progress tracker (a simple bar chart in a spreadsheet) helpful. The goal isn’t elaborate celebration; it’s just keeping the system visible enough that you notice when it’s working. If you’re building this system alongside a broader savings goal, resources like our guide on starting to invest with no prior experience can help you see how these building blocks connect into a full financial picture.

Using a sinking fund to cover a different expense than the one it was intended for is the single most common way beginners derail their system. Once you’ve transferred money out for the “wrong” reason, the fund is short when the actual bill arrives, and you’re back to scrambling. If a genuine financial emergency arises, use your emergency fund, not your sinking funds.

One honest limitation worth naming: the sinking fund strategy requires stable, predictable income to work smoothly. If your income is highly variable, freelance or gig work with inconsistent months, your monthly contributions may need to flex. In low-income months, you may not be able to contribute the full calculated amount. That’s a real constraint. The adaptation is to contribute a minimum floor amount in lean months and make up the shortfall in higher-income months, rather than skipping contributions entirely. If variable income is your reality, consider exploring hourly jobs currently hiring above $19 to create a more consistent income base under your sinking fund contributions.

Frequently Asked Questions

How many sinking funds should I start with as a beginner?

Start with two to three sinking funds covering your largest, most certain upcoming expenses. Most beginners do well opening funds for auto insurance, home or renters insurance, and a holiday or gift budget first, since these three categories tend to cause the biggest one-time cash crunches. Once those contributions are automatic and your budget has absorbed the shift, add one new category at a time.

Can I start a sinking fund if I’m also paying off credit card debt?

Yes, with conditions. You don’t have to choose between debt repayment and sinking funds; the two can run at the same time at different scales. Fund only your most non-negotiable categories (insurance, registration) at a minimal monthly amount while focusing the bulk of available cash on debt repayment. As balances clear, redirect freed-up minimum payments into additional sinking fund categories. Stopping sinking fund contributions entirely while in debt repayment risks running up new credit card charges when irregular bills arrive.

What’s the difference between a sinking fund and just having a savings account?

A general savings account has no designated purpose; a sinking fund has one specific goal with a target amount and a deadline. The distinction matters behaviorally: money in a labeled fund for “car insurance” is harder to spend casually than money in an unnamed savings balance. The math and automation work the same way, but the naming and separation are what prevent the money from being redirected to other uses.

Where should a beginner keep sinking fund money?

A high-yield savings account with sub-account or bucket features is the most practical choice. Banks like Ally, Marcus by Goldman Sachs, and SoFi offer labeled sub-accounts within a single savings account, currently earning 3–5% APY. This gives your money modest growth while keeping it fully liquid when the expense comes due. Avoid investing sinking fund money in stocks or volatile assets, you need it accessible on a specific date, not subject to market timing.

How do I handle a sinking fund for expenses that change in price each year?

Add a 10% buffer to your calculated monthly contribution, then review and adjust the amount once a year when you receive your renewal notice. For categories with known cost trends, homeowner’s insurance and auto insurance have both risen substantially in recent years, consider adding 5–8% annually even before you see the new bill. A small over-contribution is far less disruptive than arriving at a renewal short by $100–$200.

Should I use a budgeting app or a spreadsheet to track my sinking funds?

Either works; the right choice is whichever you’ll actually check monthly. YNAB assigns every dollar a job and handles multiple sinking fund categories cleanly, but costs roughly $15 per month. A free spreadsheet with one row per fund, updated after each payday, is functionally equivalent for most beginners. The tracking method matters far less than the consistency of your monthly contributions.

What if I can only afford $20 or $30 per month for a sinking fund?

Start there. A $25/month contribution to a car maintenance fund accumulates $300 in a year, not enough to cover a major repair, but enough to cover an oil change, a tire rotation, or a small unexpected fix without going to a credit card. Small contributions build the habit and the sub-account structure; you scale the amounts up as your income and budget allow. Progress at a slow pace is still progress, and the behavioral shift of proactive saving matters even at modest dollar amounts.

Can I use sinking funds for long-term goals like replacing an appliance in three years?

Sinking funds work well for multi-year goals, and the math is the same. A $1,800 refrigerator replacement in 36 months requires $50 per month plus a 10% buffer, or $55 per month. Starting three years out means you never need to finance the appliance or disrupt your budget when it fails. Multi-year sinking funds are worth holding in a HYSA where the balance earns interest over the longer horizon.

How do sinking funds help with financial stress specifically?

The stress relief comes from removing uncertainty. When you know your car insurance is already funded, the renewal notice triggers a transfer, not a scramble. Over time, as more categories are funded, the number of moments each year where money feels tight drops significantly. This is separate from income: the sinking fund strategy for beginners often improves how a budget feels before it changes what the budget earns. If you’re also managing broader cost pressures, pairing sinking funds with tools like utility assistance programs such as LIHEAP can reduce the total number of irregular bills you need to fund independently.