Reviewed by the MyFinancial101 Editorial Team

Our Take

For recent graduates with thin or no credit files, the fastest path to a strong profile is a two-track approach: start student loan repayment immediately to activate your existing installment account, and open one secured or student credit card within the first month. Together, these two moves can push most graduates from no score to a 680-720+ FICO range within 18 months. The case against this approach is the case for graduates carrying unstable income, if missing a payment is a real risk, holding off on new credit until employment stabilizes is the smarter call.

Building credit after college is less optional than it used to be. Landlords in competitive rental markets now routinely pull credit reports, and LendingTree’s analysis of College Board data shows that 47% of 2024 bachelor’s degree recipients from four-year public and private nonprofit colleges graduated with student loan debt, meaning millions of new graduates already have an active installment account on file, they just haven’t started using it strategically. That’s a significant head start most people ignore.

This article is written for graduates who finished school in the last year or two and want a concrete, time-anchored plan rather than generic advice. What makes the recommendation work is consistency across exactly two score drivers; what makes it fail is income instability during the critical first six months of reported activity.

Key Takeaways

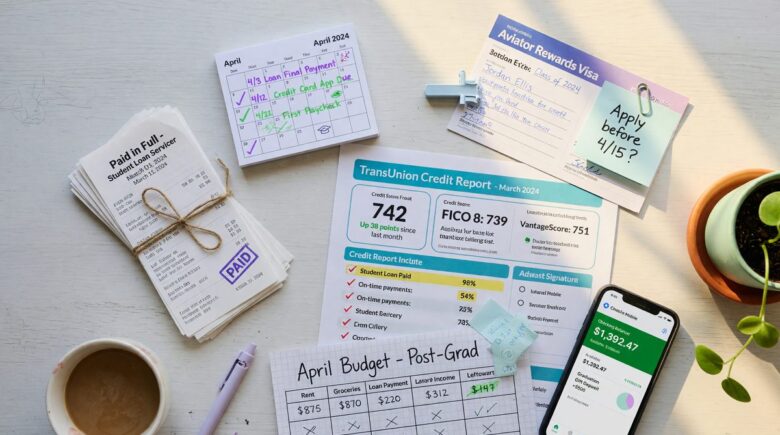

- The average FICO score for Gen Z (ages 18-28) is 678, compared to a national average of 713, according to Experian’s 2025 data, closing that gap is achievable inside 18 months with disciplined habits.

- Payment history accounts for 35% of your FICO score, making on-time payments on even a single loan or card the single highest-leverage action available to a new graduate, per Experian’s score factor breakdown.

- Most FICO scores require at least one account open for six months with reported activity before a score can even be generated, meaning the clock starts on Day 1, not when you feel financially settled.

- A secured card with as little as a $200 deposit can be opened with no prior credit history and begins reporting positive data to the bureaus immediately, according to the CFPB’s credit-building guidance.

- In my experience reviewing reader questions, the graduates who reach the 700+ range fastest are almost always those who opened their first card within 30 days of graduation and never carried a balance above 20% of their credit limit.

Where You Actually Stand Right After Graduation

Here’s what underwriters know that most new graduates don’t: a thin credit file is not the same as a bad one. Many graduates have no FICO score at all, not because anything went wrong, but because no account has reported six months of payment activity yet. That’s a very fixable problem.

Your first move is pulling all three of your free credit reports from AnnualCreditReport.com, which is the only federally authorized source for free reports from Equifax, Experian, and TransUnion. Review each one for existing accounts, open errors, or any fraudulent accounts that may have been opened in your name. Student loans in deferment almost certainly appear on your reports already, but deferment means zero payment activity is being reported, which means zero contribution to your score.

Set realistic expectations. Most graduates won’t see a generated FICO score until roughly month six or seven, and scores in the 630-660 range are typical at that point. The 680-720 range is achievable by month 15-18 with consistent behavior. The 678 average FICO score for Gen Z reported by Experian in 2025 reflects exactly this population, many have started building, but few have optimized.

What I see in practice: Readers who wait until they feel “financially stable” to open their first card often delay six to nine months unnecessarily. The clock for generating a score starts when an account opens, not when life feels settled. Waiting costs real time, and time in credit history is one factor you genuinely cannot rush.

Your Student Loans Are Already Working For You, If You Let Them

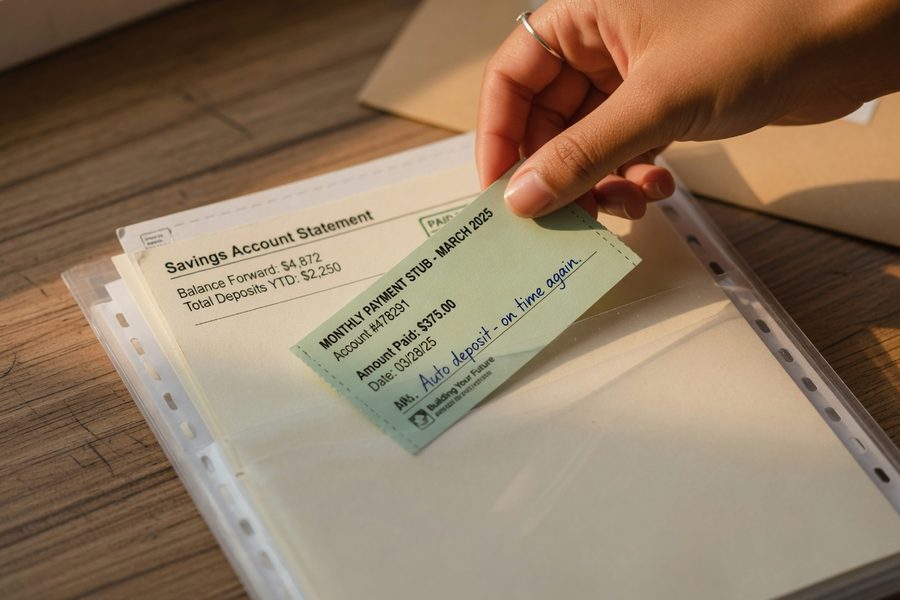

Switching out of deferment and into repayment is the single fastest action most graduates can take to activate an existing credit-building asset. Every on-time payment on a federal or private student loan reports to all three major credit bureaus, Equifax, Experian, and TransUnion, and begins stacking payment history immediately.

Choosing the Right Repayment Plan

For graduates worried about cash flow, income-driven repayment (IDR) plans through the Federal Student Aid office can reduce monthly obligations significantly while still generating positive payment reports. The key point: a $50 on-time payment builds your score exactly as well as a $500 on-time payment. The bureau doesn’t care about the dollar amount; it cares about the binary outcome, paid on time, or not.

The average 2023-24 bachelor’s degree recipient who borrowed left school with $29,560 in student loans, according to College Board’s 2025 data. That balance, managed responsibly over 18 months, contributes meaningfully to your payment history, which, at 35% of your FICO calculation, is the dominant factor in your score.

One quick arithmetic check: if a graduate starts repayment at month one with a $250/month IDR payment and hits 100% on-time over 18 months, that’s 18 consecutive positive payment marks on an installment loan, a pattern that credit scoring models weight heavily by month 12.

Getting Your First Credit Card When You Have No History

Three products genuinely work for graduates building credit after college with no existing score: secured cards, student credit cards, and authorized-user status on a parent’s or family member’s established account. Each has a different cost and eligibility profile.

Secured Cards vs. Student Cards vs. Authorized-User Status

| Option | Upfront Cost | Reports to Bureaus | Best For |

|---|---|---|---|

| Secured Credit Card | $200-$500 deposit (refundable) | Yes, all three major bureaus | Graduates with no family support or existing score |

| Student Credit Card | No deposit required | Yes, all three major bureaus | Graduates who still qualify for student products (typically up to 1 year post-graduation) |

| Authorized User | $0 personal cost | Yes, if primary cardholder’s issuer reports authorized users | Graduates with access to a trusted family member’s account in good standing |

The CFPB specifically recommends secured credit cards and credit-builder loans for consumers who are new to credit. Authorized-user status adds positive history with zero personal liability to the primary cardholder, which makes it appealing, but it requires trust on both sides, and not every graduate has that option.

Once you have a card, use it for small, fixed recurring charges: a streaming subscription, monthly gas, or a grocery run. Pay the full balance before the statement closing date. That pattern, spend a little, pay in full, repeat, is what moves scores.

What clients often miss: Paying your card in full after the statement posts, rather than before the closing date, still reports a balance to the bureaus. Paying before the closing date keeps reported utilization near zero, which is a meaningful difference in your score, especially in months 6 through 12 when the model is first assessing you.

The Two Numbers That Control 65% of Your Score

Payment history at 35% and credit utilization at 30% together account for 65% of your FICO score. Everything else, length of history, credit mix, new inquiries, matters, but not as much as getting these two right consistently.

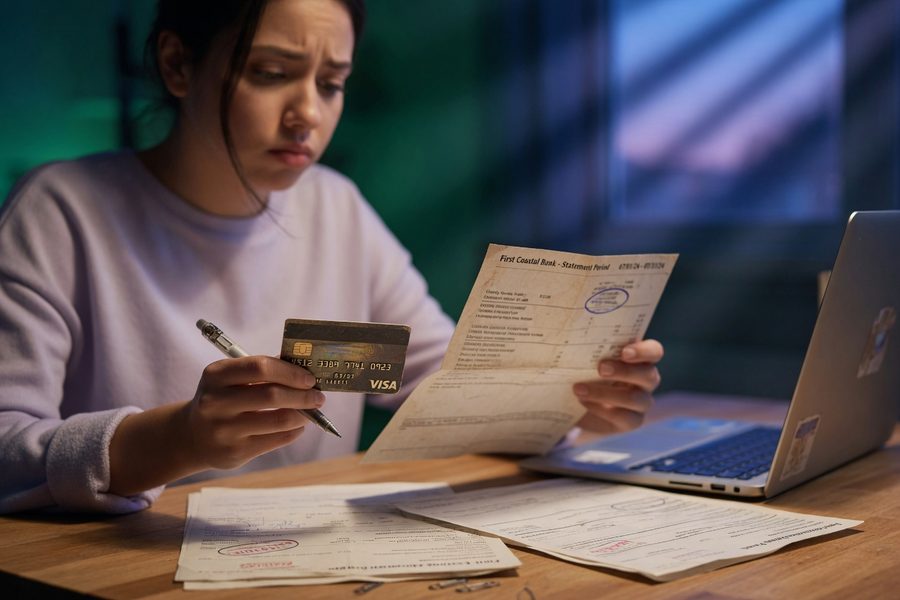

Keep utilization under 30% at all times, and ideally under 10% by the time you’re approaching a major application like a car loan or apartment lease. On a $500 secured card, that means carrying no more than $150 in reported balance, and preferably under $50. Set autopay for at least the minimum payment on every account, then layer calendar reminders to pay the full balance before each statement closes. One missed payment in month eight can suppress a 690 score back below 650. That’s a documented pattern in how FICO models weight recent delinquency, the damage is disproportionate in a thin file. If you’re concerned about managing debt responsibly, our guide to prioritizing and negotiating credit card debt covers the mechanics in detail.

Accelerating Progress With Alternative Reporting

Experian Boost allows consumers to add utility, phone, and qualifying streaming payment history directly to their Experian credit file, for free., this remains one of the fastest zero-cost moves for graduates with limited traditional credit accounts. It does not affect TransUnion or Equifax scores directly, but an improved Experian file is still a meaningful gain for lenders who pull that bureau.

Credit-Builder Loans

Credit-builder loans, offered by many credit unions and online lenders, work differently from traditional loans: the lender holds the funds in a savings account while you make monthly payments, then releases the money to you at the end. The payments report to the bureaus as a positive installment account. The CFPB identifies these products as specifically designed to help consumers new to credit build history. Typical loan amounts run $300 to $1,000 with 12-24 month terms, the cost is low and the credit benefit is real.

One caution: space out any new applications by at least six months. Each hard inquiry trims a few points from a thin file, and the effect is proportionally larger when your history is short. If you’re also trying to build income during this period, our list of $19+ hourly jobs hiring now is worth a look, stable income is what makes consistent payments possible in the first place.

Handling the Obstacles Most Credit Guides Skip

Income volatility is the real threat to an 18-month credit-building plan. Most advice assumes steady employment from month one, which isn’t the reality for a large share of new graduates. Here’s how to handle the gap without derailing your payment history.

When Income Is Uncertain

If you’re between jobs or in a contract role, switch student loans to an IDR plan immediately and reduce your secured card balance to near zero before the next statement closes. Your goal is protecting the payment streak at all costs, even if that means charging almost nothing to the card for two or three months. Strategically, a zero-activity month is far less damaging than a single 30-day late payment. For graduates looking at income options while building their profile, micro-freelancing is worth considering; our coverage of the micro-freelancing surge covers platforms and realistic earnings.

Graduates Without Family Financial Support

Not every graduate has access to authorized-user status or a family co-signer. That’s a real disadvantage, but it’s not an insurmountable one. The secured card plus credit-builder loan combination produces a two-account file with both revolving and installment credit reported, which is sufficient for FICO scoring models to generate a score and begin rewarding consistency. The timeline may run three to four months longer than for graduates with authorized-user access, but the endpoint is the same. For those navigating tighter budgets in the process, the updated 2026 poverty guidelines may affect eligibility for programs that ease living costs during the transition.

Keeping Old Accounts Open

If you move or change banks, resist the impulse to close old accounts. Credit age is a factor in your FICO score, and closing an account reduces your available credit, both moves hurt a thin file. Keep old cards open with a small recurring charge and autopay, even if you’re not actively using them.

Where this gets tricky: Graduates who land a decent job quickly sometimes rush to apply for three or four products in the first year, thinking more accounts means faster progress. What we tell readers: two well-managed accounts in the first 18 months outperform five poorly managed ones, every time. The score model rewards consistency, not volume.

What “Strong” Actually Looks Like at the 18-Month Mark

A realistic, defensible target for an 18-month disciplined graduate: a FICO score in the 690-730 range, two to three accounts in good standing, zero late payments, and utilization consistently below 20%. That profile qualifies for most standard apartment leases without a co-signer, a reasonable auto loan rate, and a credit card upgrade to an unsecured rewards product.

Here’s the comparison that matters: the national average FICO score is 713 per Experian’s 2025 data. A graduate who executes this plan consistently can realistically reach or exceed that average in 18 months, starting from zero. That’s not aspirational; it’s the arithmetic of how FICO models score thin files that execute cleanly. Pair that credit foundation with early investing habits, and our guide on how to start investing with zero experience covers what comes next.

Where This Recommendation Falls Short

The two-track approach I’ve outlined, activate student loan repayment, open one credit card immediately, is the right call for most graduates. But there are clear situations where it is not.

The biggest drawback is the assumption of income stability. A single 30-day late payment in months one through six will suppress a newly generated score significantly, because FICO models weigh recent delinquency heavily when the file is thin. For graduates who are unemployed, in unpaid internships, or in a job search that realistically runs three to six months, opening a credit card before income is secured creates a real risk of missing a payment. In that scenario, the better approach is to activate IDR on student loans (keeping that payment as low as possible), hold off on opening a new card until the first steady paycheck arrives, and use the waiting period to monitor credit reports and pull any errors.

The tradeoff is time. Delaying card opening by three to four months pushes the 18-month milestone back, a 720 score at month 22 instead of month 18. That is a legitimate cost, but it’s far less damaging than a 30-day late payment that can suppress a thin-file score by 60-90 points and takes years to age off fully.

The second concession is the authorized-user strategy. It works cleanly when family dynamics allow it. When they don’t, either because the family member has their own credit problems or because the relationship doesn’t support it, the secured card alternative is slower by roughly one credit cycle but produces the same eventual outcome. Graduates without any family support should budget for the $200-$300 secured card deposit and understand that the 18-month timeline is achievable without any external help; it just requires clean execution.

Finally, graduates with significant existing debt from private loans at high rates face a genuine tension between making larger payments to reduce interest cost and keeping cash available to fund a $200 deposit. If cash is the constraint, a credit-builder loan at a credit union, which builds savings while reporting to bureaus, is the better first move than a secured card. The catch is that credit-builder loans are installment accounts, not revolving credit; a full FICO score benefits from having both types reported eventually.

How We Sourced This

This article draws primarily on Experian’s 2025 average FICO score data for the U.S. and Gen Z specifically, College Board’s 2025 Trends in Student Aid highlights covering 2023-24 borrowing data, LendingTree’s 2024 analysis of College Board student debt statistics, and the CFPB’s consumer guidance on building and maintaining credit scores. Score factor weights reflect FICO’s publicly documented model methodology as reported by Experian. All data cited covers periods through 2025, and this article was written and verified. Sources were selected for institutional authority; no affiliate-compensated product reviews were used as primary data sources.

Frequently Asked Questions

How long does it take to build credit after college with no history?

Most graduates can generate their first FICO score within six to seven months of opening an account and making consistent on-time payments. Reaching the 680-720 range typically takes 12 to 18 months with disciplined use of one to two accounts.

Does paying off student loans help build credit?

Yes, but only once you begin making payments, not while loans sit in deferment. Each on-time payment reports positively to all three credit bureaus and contributes directly to payment history, which is the single largest factor in your FICO score at 35%.

What is the minimum credit score for renting an apartment after graduation?

Most landlords in competitive markets look for scores of 620 or higher, with 650-680 being a common informal threshold for approval without a co-signer. Reaching 690+ within 18 months positions you well for most standard rental applications.

Can I build credit without a credit card?

You can, using student loan repayment and a credit-builder loan alone. However, FICO scoring models reward having both an installment account and a revolving account on file, a combination that most card-free approaches don’t produce. The all-loans path works but runs slower.

Is a secured credit card worth it for recent graduates?

For graduates without existing credit or access to authorized-user status, a secured card is the most accessible and reliable entry point. The deposit, typically $200 to $500, is fully refundable when the account is upgraded or closed in good standing, so the real cost is just the opportunity cost of that cash sitting idle for 12 to 18 months.

How does being an authorized user on a parent’s card affect my credit?

If the primary cardholder’s issuer reports authorized users to the credit bureaus, the account’s full history can appear on your credit report, including its age, credit limit, and payment record. This is one of the fastest ways to gain a positive tradeline with no personal financial liability, though not all card issuers report authorized users to all three bureaus.

Will applying for multiple credit cards hurt my score right after graduation?

Each application triggers a hard inquiry, which typically trims three to five points from a thin-file score. Applying for two or three products within a few months of graduation can suppress a new score by 10-15 points at a stage where every point matters. Spacing applications at least six months apart is the better approach, and one well-chosen card is genuinely sufficient for the first 12 months.

Sources

- Experian, What Is the Average Credit Score in the U.S.? (2025)

- Consumer Financial Protection Bureau, How Do I Get and Keep a Good Credit Score?

- College Board, Trends in Student Aid 2025 Highlights

- LendingTree, Student Loan Debt Statistics (2024)

- myFICO, What’s in My FICO Scores?

- Equifax, How to Build Credit