Fact-checked by the MyFinancial101 editorial team

The Verdict

A tax loss harvesting strategy is worth running if you hold a taxable brokerage account, are in the 22% federal bracket or higher, and have unrealized losses available to sell. It is not worth the effort if your investments live entirely in tax-advantaged accounts like a 401(k) or IRA, or if you are in the 10% to 12% bracket where capital gains may already be taxed at zero.

Most investors know they should minimize taxes, yet the single factor that determines whether a tax loss harvesting strategy actually pays off is your marginal tax rate on capital gains. At the 20% long-term rate plus the 3.8% Net Investment Income Tax that applies to high earners, harvesting a $10,000 loss is worth nearly $2,380 in real cash, before you factor in years of compounding on that deferred tax. According to IRS Topic No. 409, any net capital losses beyond what you use to offset gains can reduce ordinary income by up to $3,000 per year, with the remainder carrying forward indefinitely.

The strategy matters more right now than it did five years ago. Market volatility in 2025 and early 2026 left plenty of portfolios with positions sitting below cost basis, and with the April 15 filing deadline behind us, investors finally have full visibility into their 2025 tax picture and can harvest deliberately for the current year.

| Factor | Reasons to Harvest Losses | Reasons Not to Harvest |

|---|---|---|

| Tax savings | Offset capital gains dollar-for-dollar; reduce ordinary income by up to $3,000/year | Savings are minimal or zero if you are in the 0% capital gains bracket (income below ~$47,025 single in 2025) |

| Carryforward value | Unused losses carry forward indefinitely with no expiration under IRS rules | Carrying losses forward only helps if you have future gains to absorb them |

| Market exposure | Replacement securities keep you invested; no meaningful change to long-term returns | Poor replacement picks can cause portfolio drift and tracking error |

| Short-term gains | Short-term losses offset short-term gains taxed at ordinary income rates up to 37% | Triggering short-term gains while harvesting long-term losses can backfire |

| Account type | Works well in taxable brokerage accounts with diversified holdings | IRAs, 401(k)s, and Roth accounts offer no tax benefit from loss harvesting |

| Complexity | Robo-advisors and direct indexing platforms automate the entire process | DIY execution risks triggering wash sales across spousal or retirement accounts |

Key Takeaways

- Your federal marginal rate is at least 22%, meaning harvested losses produce real tax savings rather than negligible ones.

- You hold a taxable brokerage account with at least one position currently sitting below its cost basis.

- You can identify a suitable replacement security that is not substantially identical to the one you are selling, avoiding the 30-day wash-sale window.

- You have realized or expected capital gains of any size in the current tax year to offset, or you will accept the $3,000 ordinary income deduction as a consolation.

- You are prepared to track the new cost basis in the replacement security, or you are using a platform that does it automatically.

- You have checked all accounts you control (including a spouse’s IRA) to make sure the replacement purchase will not trigger a wash sale.

- You understand that harvested losses defer taxes rather than eliminate them permanently, since the lower cost basis in the replacement raises future gains.

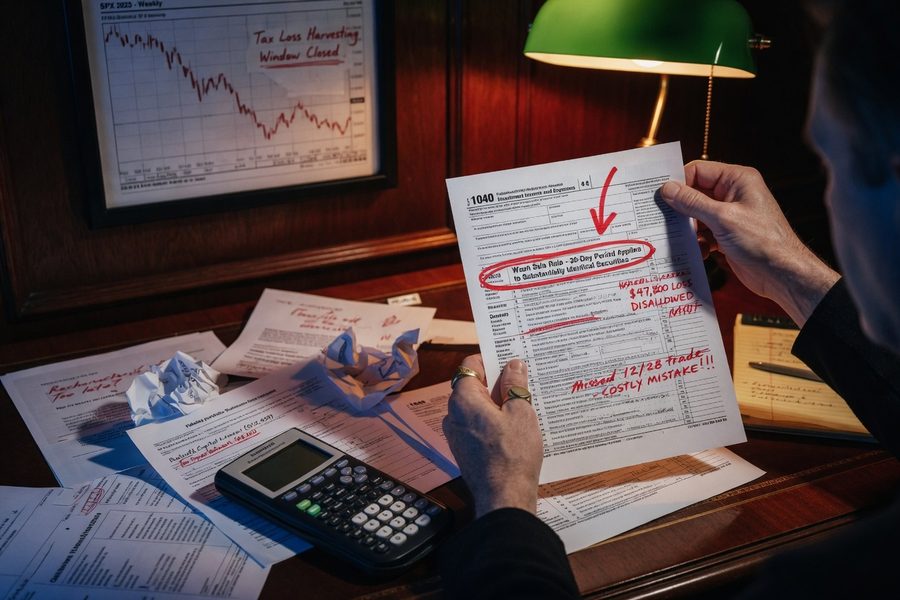

What the IRS Rules Actually Say, and Where Investors Get Burned

The wash-sale rule is the rule most investors underestimate, and violating it silently erases the entire benefit of a harvest. Under IRS Publication 550, you cannot claim a loss on a security if you buy a “substantially identical” security within 30 days before or after the sale, in any account you control. That includes your spouse’s IRA. Fidelity and Vanguard both highlight this cross-account trap explicitly, and it catches do-it-yourself investors more than any other single mistake.

The short-term versus long-term distinction matters in a specific order. The IRS requires you to net short-term losses against short-term gains first, then net long-term losses against long-term gains. Only after that netting can losses cross categories. Fidelity notes that short-term losses deliver the greatest immediate value because short-term gains are taxed at ordinary income rates, as high as 37% for top earners, rather than the 15% or 20% long-term rate. A dollar of short-term loss harvested by a top-bracket taxpayer is worth roughly twice what a long-term loss is worth in that same year.

Any net capital losses that exceed your gains can offset up to $3,000 of ordinary income per year ($1,500 if married filing separately). Everything beyond that carries forward without limit. This carryforward is a genuine asset: a taxpayer who harvests $30,000 in losses in a flat year has a decade of $3,000 ordinary income deductions locked in, or a ready offset for the next time markets surge and gains pile up. The deferred tax liability in the replacement security is the price, when you eventually sell the replacement at a gain, the lower cost basis means a larger taxable gain. The strategy defers taxes; it does not make them disappear.

Is December Really the Best Time to Harvest?

No, and waiting until December is one of the most common mistakes in loss harvesting. The trade date determines the tax year, and losses are available whenever a position is below its cost basis, not just in Q4. Morgan Stanley, Investopedia, and multiple direct indexing providers confirm that a year-round monitoring approach catches far more losses than the annual December scramble.

The window right after the April 15 filing deadline is particularly underused. By mid-April, you know your exact 2025 tax outcome: realized gains already booked, the size of any carryforward from prior years, and your projected bracket for 2026. That information lets you harvest with precision. If you already have a large carryforward from 2022 or 2023’s volatility, for example, additional harvesting in June 2026 may have diminishing value unless you are also generating new gains this year. Pairing that knowledge with any mid-year market dip is the most controlled way to execute.

Robo-advisors like Wealthfront and Betterment run automated daily or near-daily scans precisely because opportunities are episodic. Wealthfront reported delivering $161 million in estimated tax savings to clients through tax-loss harvesting in 2025, a strong equity year, demonstrating that losses appear even in bull markets, just in individual positions rather than across whole indexes. As Fidelity’s guidance on tax-loss harvesting puts it, volatile markets create episodic opportunities, and losses taken in down years can act as a buffer against taxable gains for years afterward.

What the Numbers Look Like in Practice

The gap between DIY and automated harvesting is larger than most investors expect. Range Advisory’s 2025 data shows that accounts using standard tax-loss harvesting harvested an average of $13,281 in capital losses per taxable account. Accounts that combined tax-loss harvesting with direct indexing averaged $18,281 in harvested losses, on average account sizes of $413,759. ETF-only TLH portfolios came in at $4,808 on average. That spread illustrates a concrete hierarchy: direct indexing gives you more individual securities to harvest from, ETF-only gives you fewer, and that limits your raw material.

Here is a simple worked example. Suppose you harvested $13,281 in net long-term capital losses in 2026 and you have $13,281 in long-term gains from selling a fund that appreciated. At the 15% long-term capital gains rate, those gains would have cost you $1,992 in federal tax ($13,281 × 0.15). With the harvest, that bill drops to zero. You reinvest the full $13,281 in a replacement position, keeping your market exposure intact. That $1,992 stays in your account, compounding. At a conservative 6% annual return, it grows to roughly $3,566 in ten years, a tax benefit that compounds well beyond the year of harvest. If you are in the 20% rate plus 3.8% NIIT, the immediate savings on the same loss would be $3,159, and the ten-year value climbs higher still.

The psychological barrier here is real and worth naming. Selling a position at a loss feels like admitting defeat. Many investors hold losing positions longer than they should because they are waiting to “get back to even,” forfeiting the tax asset in the process. The loss is already reflected in your portfolio’s value, harvesting it simply converts a paper loss into a documented tax benefit you can carry forward indefinitely.

For investors who are also managing cryptocurrency investments, note that the IRS currently treats crypto as property, which means crypto losses are subject to the same capital gain and loss netting rules, but the wash-sale rule does not yet apply to crypto under 2026 law, which gives crypto holders a meaningful harvesting advantage over stock investors.

Who Should and Who Should Not

Good candidates

Tax-loss harvesting produces the clearest benefit for investors with taxable brokerage accounts, meaningful gains to offset, and marginal rates that make every dollar of loss count.

- A W-2 earner in the 24% bracket or above who is also investing in a taxable brokerage account, harvesting even modest losses cuts a real tax bill.

- A retiree with a large taxable portfolio taking required minimum distributions (RMDs) from an IRA who is generating short-term gains on rebalancing trades.

- An investor using a direct indexing platform with a portfolio over $250,000 in taxable accounts, the individual stock exposure maximizes harvestable positions even in up markets.

- Anyone with a large capital gain event on the horizon (selling a business, vesting RSUs, or liquidating concentrated stock) who can bank losses now to offset that gain.

- A taxpayer carrying forward losses from 2022 or 2023 who wants to understand how those interact with 2026 gains before rebalancing, reviewing this with a CPA before year-end is worth the fee.

Who should skip it

The strategy adds friction without payoff for a defined set of investors.

- Anyone whose entire investment portfolio sits in tax-advantaged accounts (401(k), IRA, Roth), losses inside those accounts produce no tax benefit whatsoever.

- Single filers with taxable income below approximately $47,025, where the 0% long-term capital gains rate already wipes out most of the tax on realized gains.

- Investors holding highly appreciated positions in taxable accounts where harvesting would require selling securities with massive embedded gains to fund replacements, the tax cost exceeds the benefit.

- Anyone who cannot reliably track wash-sale rules across multiple accounts (their own, a spouse’s, IRAs) without automated help, one accidental wash sale can disallow the loss entirely.

Frequently Asked Questions

Does tax-loss harvesting actually save money, or does it just delay taxes?

Both, and that distinction matters. Harvesting defers the tax on gains by lowering the cost basis of the replacement security, so when you eventually sell, a larger gain is taxable. The real benefit is the time value of the deferral: keeping that tax money invested and compounding for years is worth real dollars, especially at higher rates. If you never sell the replacement (say, you donate it or pass it through your estate with a stepped-up basis), the deferred tax may never be owed at all.

What is the wash-sale rule and how do I avoid triggering it?

The wash-sale rule disallows your claimed loss if you buy a substantially identical security within 30 days before or after the sale, in any account you control, including an IRA or a spouse’s account. Avoid it by replacing the sold security with something correlated but not substantially identical: sell an S&P 500 index fund and replace it with a total market fund or a large-cap ETF from a different provider, for example. Wait at least 31 days before buying back the original if you prefer it.

Can I harvest losses in a year when markets are up overall?

Yes, and this is one of the most overlooked aspects of the strategy. Even in a strong equity year, individual positions within a diversified portfolio frequently dip below their cost basis due to sector rotation, earnings misses, or short-term volatility. Wealthfront’s 2025 results, $161 million in estimated client tax savings during a broadly positive year, confirm that losses are available year-round for investors who monitor at the position level rather than looking only at portfolio-wide performance.

Is tax-loss harvesting worth it if I manage my own investments without a robo-advisor?

It can be, but the effort scales with portfolio complexity. A DIY investor with five to ten ETFs in a taxable account can scan positions quarterly, identify losses, and execute replacements manually without much friction. The critical steps are keeping clean cost-basis records, tracking the 30-day wash-sale window across all accounts, and reporting correctly on Schedule D and Form 8949. If you are already preparing your own taxes and filing accurately, adding loss harvesting is a reasonable extension of that process, and pairing it with a solid understanding of tax season preparation will keep you from missing deadlines or paperwork. Where DIY breaks down is in portfolios with dozens of individual positions; at that scale, automated platforms earn their fee.

Investors who are just getting started and want to understand the broader context before implementing any tax strategy should read up on how to start investing with zero experience first, the mechanics of tax-loss harvesting only make sense once you understand what you own and why. And if high-interest debt is still a factor in your finances, resolving that through options like credit card debt prioritization typically delivers a better guaranteed return than any tax strategy can.

Sources

- IRS, Topic No. 409: Capital Gains and Losses

- IRS Publication 550, Investment Income and Expenses (Wash-Sale Rules)

- Fidelity Viewpoints, Tax-Loss Harvesting: How It Works

- Wealthfront, Tax-Loss Harvesting Results 2025

- Range Advisory, Tax-Loss Harvesting and Direct Indexing Results 2025

- MyFinancial101, Save For Retirement Over College