Fact-checked by the MyFinancial101 editorial team

The Verdict

Buy now pay later vs saving comes down to urgency and cash flow. BNPL is worth it if the purchase is a genuine need, you have zero late payments in your history, and the plan is truly 0% with no fees. Skip it if you carry existing debt, lack a full emergency fund, or are buying something you could wait 30 to 90 days to afford outright.

Most people assume BNPL is a budgeting tool. It is not. It is a credit product, and the single factor that determines whether it helps or hurts you is whether your cash flow can absorb every scheduled payment without strain. Federal Reserve data released in 2026 shows that U.S. lenders originated $156.7 billion in BNPL credit products in 2025 alone, which tells you how normalized this form of borrowing has become. That normalization is exactly what makes it dangerous for the wrong borrower.

The buy now pay later vs saving debate has a real dollar figure attached to it right now because high-yield savings accounts at institutions like SoFi and Ally are still paying competitive rates. The choice is not just psychological; it is arithmetic.

| Factor | Reasons to Use BNPL | Reasons to Save Up First |

|---|---|---|

| Cost | True 0% pay-in-4 plans cost nothing if paid on time | No fees or interest under any scenario |

| Speed | Immediate access to a needed item today | Delays purchase by 30–90 days on average |

| Cash flow | Splits a $400 purchase into 4 payments of $100 | Preserves liquidity until the full amount is saved |

| Savings habit | No direct impact if used as a one-time tool | Builds consistent saving behavior over time |

| Late payment risk | Low if income is stable and plan is tracked | No risk; purchase only happens when money exists |

| Debt stacking | One plan is manageable; multiple plans create blind spots | Zero incremental debt in any case |

| Best use case | Essential purchase, predictable paycheck, strong payment history | Discretionary item, variable income, or thin emergency fund |

Key Takeaways

- Your emergency fund covers at least 3 months of expenses before you add any new payment obligations

- The BNPL plan is genuinely 0% APR with no origination fee, late fee waiver does not apply, and you have read the full terms

- Your existing debt-to-income ratio is below 36% including the new BNPL payments

- You have made zero late payments on any loan or credit account in the past 12 months

- The purchase is a necessity, not a discretionary or impulse buy, and cannot be safely delayed

- You are running only one active BNPL plan at a time, not stacking two or more simultaneously

- Saving up would take fewer than 90 days, in which case waiting is almost always the better financial move

How BNPL Works in 2026 and Why It Feels Cheaper Than It Is

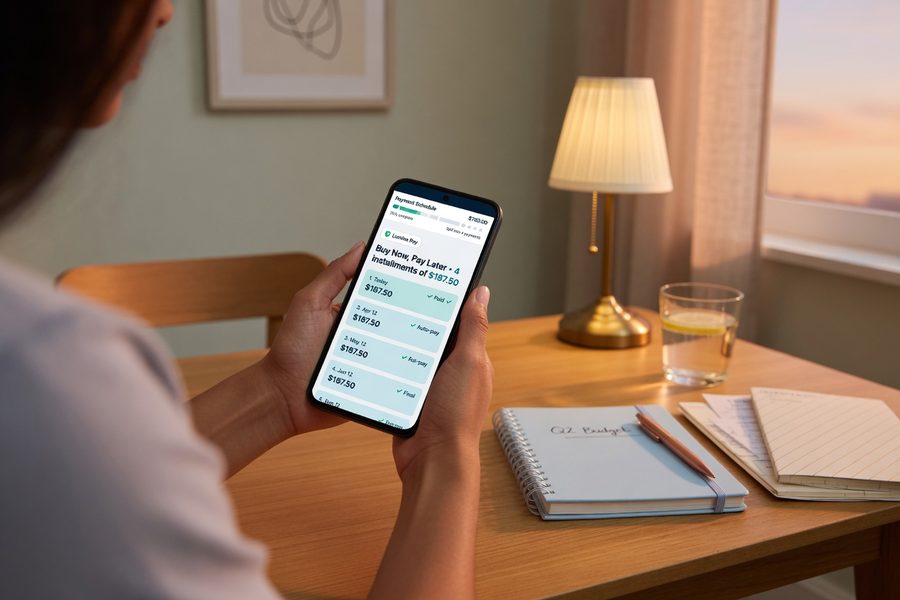

Pay-in-4 plans account for exactly half of total BNPL issuance. The Federal Reserve’s 2026 analysis confirms that $78.3 billion of the $156.7 billion originated in 2025 came from pay-in-4 products, with the remainder in longer-term installment loans that frequently carry interest. The split matters because many consumers assume “BNPL” always means 0% APR. It does not. Providers like Affirm offer both interest-free pay-in-4 options and longer installment loans with APRs that can reach 36%, depending on your FICO Score and the purchase amount.

The psychological pull is real and well-documented. Breaking a $540 appliance into four payments of $135 does not feel like debt, even though it is. The CFPB has documented that BNPL users tend to carry higher overall unsecured debt balances and are more likely to be running multiple simultaneous loans. That pattern suggests many borrowers are using BNPL to extend purchasing power they do not actually have, not as a neutral cash-flow tool. The average BNPL loan size was just $135 in 2023 according to CFPB’s 2025 market report, which means most of these plans are not for major appliances. They are for everyday purchases people could simply save for.

When Saving Up Is the Clear Winner

Saving first wins on nearly every discretionary, non-urgent purchase. Full stop. The math is straightforward: a high-yield savings account paying around 4.5% APY on $400 saved over 60 days earns roughly $3 in interest, while a BNPL plan with even one late fee can cost $7 to $30 depending on the provider. That is a $10 to $33 swing in the wrong direction for a purchase you could have waited on.

Beyond the fee math, the behavioral evidence is damning. A Financial Health Network survey found that nearly one-third of BNPL users spent more than they otherwise would have, and 34% said they would not have made the purchase at all if BNPL had not been available. That is not budgeting. It is impulse spending dressed in installment clothing. If you recognize yourself in that statistic, saving up first is the move that actually reflects your priorities, not a vague aspiration toward discipline.

If you are also working to build financial resilience in other areas, the savings discipline you build here compounds. Whether it is learning to start investing with zero experience or protecting yourself from the kind of debt spiral described in our reporting on credit card debt crushing low-income households, the habit of saving before spending is foundational. Debt is easy to accumulate and slow to escape.

When Does BNPL Actually Make Financial Sense?

BNPL earns its place in exactly one scenario: a genuine necessity, stable income, a true 0% APR term, and a payment schedule you can meet without touching your emergency fund. That is a narrow window, and most consumer situations do not fit inside it cleanly.

Consider a concrete example. You need a $540 washing machine. Your paycheck hits every two weeks. A pay-in-4 plan from a provider like Affirm or Klarna splits that into four payments of $135, due every two weeks. If your budget can absorb $135 per paycheck without strain and the plan carries no interest or fees, you have effectively gotten a six-week float at zero cost. That is a legitimate use. Compare that to saving $135 per paycheck for the same six weeks: you would have $270 saved after the first cycle, not the machine. If the washer is broken and you have children at home, the BNPL plan wins on urgency alone.

The California Department of Financial Protection and Innovation (DFPI) frames it directly: BNPL plans carry the same obligations and risks as other forms of credit, and consumers must evaluate affordability carefully to avoid overextending themselves. “Interest-free” is a term structure, not a financial free lunch. The FDIC makes the same point in its consumer guidance, noting that any deferred-payment product still creates a legal repayment obligation regardless of how the checkout screen presents it.

One honest caveat worth naming: even a well-managed, genuinely 0% APR pay-in-4 plan does not appear on your Experian, Equifax, or TransUnion credit file in most cases, which means it builds no positive FICO Score history. A Chase credit card paid in full each month, by contrast, does. If your goal includes credit-building alongside the purchase itself, BNPL delivers nothing on that front.

Hidden Costs, Behavioral Traps, and the Late Payment Problem

Nearly half of BNPL users have a cash-flow problem they may not recognize as one. Recent survey data shows that 47% of BNPL users made at least one late payment in the past year. For context, BNPL charge-off rates run around 1.8% to 2%, which is lower than credit cards, meaning most people technically pay back what they borrow. But making a late payment and eventually paying off a loan are different things. Late fees, frozen accounts, and the stress of scrambling to cover a missed installment represent real financial friction even when the debt eventually clears.

Stacking multiple plans amplifies every risk. A borrower running three simultaneous BNPL plans of $100, $80, and $135 per month has committed $315 in fixed monthly obligations that do not appear on a standard credit report pulled by Experian or TransUnion. That is money that cannot go to an emergency fund, a car repair, or a retirement account. NBER analysis has found that BNPL adoption correlates with lower savings account balances and a higher rate of overdraft fees, a direct link between the behavior and measurable financial fragility.

The debt-to-income (DTI) ratio problem is particularly overlooked. Because most pay-in-4 BNPL plans are not reported to the major credit bureaus, they do not factor into the DTI calculation a lender like Chase or a mortgage underwriter uses to assess your creditworthiness. That sounds like an advantage, but it is actually a trap: your real DTI is higher than your file suggests, which means you may be approved for new credit you genuinely cannot afford. The New York City Department of Consumer and Worker Protection specifically warns consumers to read the fine print because plans vary widely in payment periods, fees, and interest structures.

There is also an opportunity cost working against BNPL users who could be saving instead. If you redirect $135 per month for six months into a high-yield savings account rather than paying down a BNPL plan, you accumulate $810 plus interest while keeping a financial buffer intact. That buffer is what separates a manageable budget from one that breaks under the first unexpected expense. For practical strategies on managing debt before it compounds, our breakdown of how to prioritize and negotiate with creditors applies directly to anyone who has let BNPL obligations stack up.

Who Should and Who Should Not

Good candidates

BNPL is a reasonable short-term tool for buyers who meet specific financial thresholds.

- Someone replacing a broken essential appliance who has stable biweekly income and zero existing BNPL plans open

- A buyer with a fully funded emergency fund (at least 3 months of expenses) who treats the installment plan as a cash-flow convenience, not a credit extension

- A consumer with a strong FICO Score and payment history who has read the exact fee schedule and confirmed the plan is 0% APR through the final payment date

- Someone making a large, planned purchase who can confirm each installment represents less than 10% of their monthly take-home pay

Who should skip it

These profiles are set up to get hurt by BNPL, regardless of how manageable the first payment feels.

- Anyone already carrying credit card balances above 30% utilization, adding installment obligations raises total debt load without improving terms

- Buyers with variable or irregular income, such as gig workers or seasonal employees, where a payment due date may not align with cash availability

- Anyone without a funded emergency fund; any BNPL commitment competes directly with the ability to absorb unexpected expenses

- Shoppers making a discretionary or impulse purchase, if you can honestly delay it 30 to 90 days without consequence, saving first costs you nothing and protects you from a bad month

- People currently running two or more active BNPL plans; stacking a third creates invisible fixed obligations that most budgets cannot safely absorb

Frequently Asked Questions

Is buy now pay later better than saving up for big purchases?

It depends entirely on whether the purchase is urgent and whether the plan is genuinely 0% APR. For a broken essential item with stable income, BNPL can provide a real short-term bridge. For anything discretionary, saving first removes all fee risk, avoids debt, and builds a habit that pays off with compounding benefits over time.

Does BNPL hurt your savings?

Research suggests it does. NBER analysis has linked BNPL adoption to measurable declines in savings account balances and higher overdraft frequency. Every dollar committed to an installment plan is a dollar not going into an emergency fund or investment account, and that trade-off compounds over time.

What happens if you miss a BNPL payment?

Late fees vary by provider and can range from $7 to $30 per missed payment. Some plans also pause your ability to make new purchases, and longer-term BNPL products from providers like Affirm may report late payments to credit bureaus including Experian, affecting your FICO Score. The U.S. FINRED program advises consumers to understand late payment consequences before signing up, not after a missed due date.

How long should you save before deciding to use BNPL instead?

If you can save the full purchase amount in 90 days or fewer, saving first is almost always the right call. Beyond 90 days, urgency becomes a more legitimate factor, but only if the item is a genuine necessity. If you are looking for ways to close a savings gap faster, hourly jobs currently hiring above $19 can make a real difference faster than most people expect.

Sources

- Federal Reserve, Buy Now, Pay Later: Beyond Pay-in-4 (2026)

- Consumer Financial Protection Bureau, Consumer Use of Buy Now, Pay Later and Other Unsecured Debt

- Consumer Financial Protection Bureau, BNPL Market Report (December 2025)

- California DFPI, Buy Now, Pay Later: What Consumers Need to Know

- New York City DCWP, Buy Now, Pay Later Tips for Consumers

- U.S. FINRED, Buy Now, Pay Later: Understanding the Risks