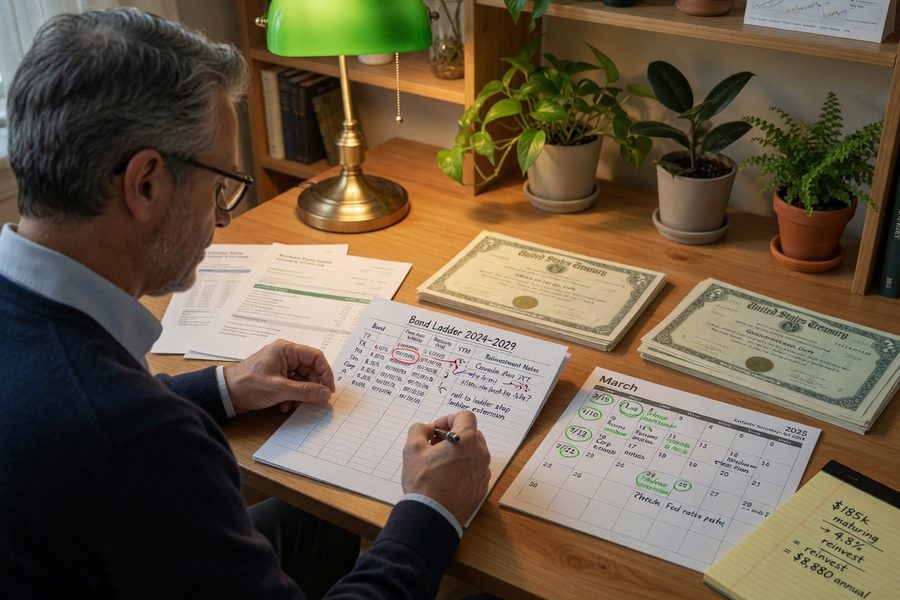

Most investors treat bond investing as a timing problem: buy when rates peak, sell before they fall, repeat. The bond laddering strategy throws that assumption out entirely. Instead of predicting where rates go next, you build a portfolio of bonds that mature at regular intervals, so you’re always collecting income and always have principal coming back to you on a known schedule. No forecasting required.

According to Vanguard’s bond strategy guidance, a ladder contains bonds of relatively equal amounts with staggered maturities specifically to minimize both interest rate and reinvestment risk. This article walks through how that structure works, how to build one that fits your actual goals, and where it genuinely falls short.

Key Takeaways

- A bond ladder staggers maturities across multiple years, so you never have your entire portfolio locked at a single rate or expiring at once.

- Holding individual bonds to maturity means you get par value back regardless of what interest rates do in between, a protection bond funds do not offer.

- True diversification across issuers typically requires a portfolio of $100,000 or more; below that threshold, credit concentration risk is a real concern.

- Each maturing rung gives you an explicit reinvestment decision: extend the ladder, shift duration, or redirect cash to spending needs without selling anything early.

What Bond Laddering Actually Delivers for Steady Income

The core promise is predictability. You buy bonds that mature in year one, year two, year three, and so on, each returning its face value at maturity. The result is a stream of principal payments arriving at regular intervals, layered on top of semiannual coupon income from every rung in the ladder. You know what’s coming and roughly when.

That structure sidesteps the problem that sinks most fixed-income plans: the need to sell before maturity. A bond held to its maturity date returns par value, period. Interim price swings from rising or falling rates are irrelevant if you never sell. This is the mechanical edge laddering has over holding a single long-duration bond or a bond fund, where net asset value moves with the market every day.

Compare that to a lump-sum approach where you park everything in a 10-year Treasury. If rates jump two years in, you’re stuck watching your bond’s market price decline while reinvestment options look far better than what you’re holding. The ladder owner in that same environment just reinvests the maturing rung at the new, higher rate and keeps moving. The income pattern becomes self-correcting over time rather than locked in.

The Interest Rate Risk Problem Laddering Solves

Concentrating maturities is the hidden risk most bond investors underestimate. If everything matures in the same year and rates have dropped, you face a reinvestment cliff: a large sum to redeploy at lower yields with no flexibility. Staggering maturities means only a fraction of your portfolio comes due at any one time, spreading that reinvestment exposure across multiple rate environments.

Duration is the technical term for how sensitive a bond’s price is to rate changes. Longer-duration bonds swing more in price when rates move. A ladder naturally blends short, medium, and longer maturities, which averages out duration across the portfolio without requiring you to calculate it explicitly. As Fidelity’s bond ladder strategy page puts it: “Laddering bonds may be appealing because it may help you to manage interest-rate risk, and to make ongoing reinvestment decisions over time, giving you the flexibility in how you invest in different credit and interest rate environments”, that’s Richard Carter, Fidelity’s vice president of fixed income products and services.

In the rising rate environment of 2022 through much of 2024, investors holding long-duration bond funds watched NAV fall sharply. Ladder holders with maturities arriving in those years simply reinvested proceeds into new bonds at better yields, effectively upgrading their portfolio’s income without selling at a loss. In a falling rate environment, the longer rungs they already held locked in higher yields far longer than a short-term rollover strategy would have.

Practical Steps to Build a Ladder That Matches Your Goals

Start with three decisions: total amount, ladder length, and rung spacing. A retiree bridging five years to Social Security needs a different structure than someone saving for a known expense in ten years. Rung spacing is commonly annual, but nothing stops you from using every two years if you want fewer reinvestment decisions or a longer overall ladder without too many individual positions.

Choosing Bond Types

Treasuries are the simplest starting point: no credit risk, highly liquid, available in any amount through TreasuryDirect with no broker markup. Investment-grade corporate bonds offer higher yields but introduce default risk and wider bid-ask spreads. Certificates of deposit are another option, especially for shorter rungs; FDIC insurance covers up to $250,000 per institution, making them a practical substitute for short-term Treasuries in taxable accounts. Charles Schwab’s bond ladder resources recommends sticking with higher-rated bonds specifically to preserve the reliability the strategy depends on.

A tax-aware wrinkle worth naming: Treasury interest is exempt from state and local taxes, which makes Treasuries particularly efficient in high-tax states for taxable accounts. Municipal bonds flip that equation, their federal tax exemption is most valuable for investors in the 32% bracket or higher. In an IRA, the tax exemption on munis is wasted, so Treasuries or investment-grade corporates typically make more sense there. Matching bond type to account type is a genuine efficiency most generic guides skip past.

Minimum Viable Size and Platform Selection

Here’s the part most articles bury: building a properly diversified individual-bond ladder usually requires $100,000 to $250,000 or more. Corporate bonds often trade in $1,000 increments on paper, but round-lot pricing is typically $10,000 per issue, and spreading credit risk across enough issuers takes real capital. Below that range, a ladder of Treasuries or CDs is still workable because you’re not taking issuer-specific credit risk. But a corporate ladder with only three or four issuers is not diversified; it’s concentrated.

If your portfolio is smaller, maturity-date ETFs like BulletShares or iBonds offer a genuine middle ground: they hold diversified corporate bonds maturing in a specific year, trade on an exchange, and liquidate at or near par at their target maturity. The fees are modest (typically around 0.10% to 0.18% annually), and you can build a ladder of these ETFs with far less capital than you’d need for individual bonds while still capturing much of the staggered-maturity benefit.

Bond Laddering Versus Bond Funds or Target-Date ETFs

The clearest advantage of an individual bond ladder is the par-value guarantee at maturity. Bond fund shares have no maturity date, so there’s no promised return of principal; you sell at whatever the NAV happens to be. That distinction matters enormously in a rising rate environment when fund prices are depressed. The ladder holder waits; the fund holder sells at a loss or holds an investment with no clear recovery timeline.

Where funds win is simplicity and liquidity. A $20,000 bond fund position is fully liquid any trading day. An individual bond may carry a spread of 0.25% to 1% or more when you sell before maturity, and small lots trade at worse prices than institutional round lots. For investors still accumulating assets or those who might need to access funds on short notice, a broad bond fund or laddered maturity ETFs may actually be the more practical choice despite the structural advantages of a true ladder.

The table below compares the three main approaches across the factors that matter most to income-focused investors.

| Factor | Individual Bond Ladder | Bond Index Fund | Maturity-Date ETFs (e.g., BulletShares) |

|---|---|---|---|

| Principal return at maturity | Par value guaranteed (if held to maturity) | No maturity date; sell at current NAV | Near-par liquidation at target year |

| Minimum practical investment | $100,000–$250,000 (corporate); $10,000–$20,000 (Treasuries/CDs) | $1 (most brokers) | $1,000–$5,000 per ETF rung |

| Annual expense ratio | $0 (no fund fees; broker spread applies on purchase) | 0.03%–0.15% (e.g., BND at 0.03%) | 0.10%–0.18% per ETF |

| Interest rate risk | Low if held to maturity; price fluctuates if sold early | Full NAV exposure to rate moves daily | Low near maturity; moderate early in fund life |

| Credit diversification (at $50,000) | Poor, 3 to 5 issuers maximum | Excellent, hundreds of issuers | Good, typically 100+ issuers per ETF |

| Liquidity (selling before maturity) | Possible; spread of 0.25%–1%+ on corporate bonds | Full liquidity any trading day at NAV | Full liquidity any trading day at market price |

| Tax control (taxable accounts) | High, investor controls timing of gains/losses | Low, fund manager triggers distributions | Moderate, ETF structure limits capital gain distributions |

| Setup complexity | High, research, purchase, and track individual bonds | Very low, single purchase | Low, one ETF per target year |

Ongoing Management, Reinvestment, and Adjustments

Each time a rung matures, you face a real choice. Reinvest in a new long rung to extend the ladder? Use the cash for planned spending? Shift toward shorter or longer maturities based on your read of needs, not rates? This is the control the strategy provides, and it’s worth treating each maturity as a deliberate decision rather than an automatic rollover. As State Street Global Advisors notes, a bond ladder strategy is designed to generate reliable income regardless of how rates move, providing stability to fund specific goals.

Credit monitoring is lighter than most investors expect. If you built with Treasuries or high-quality investment-grade bonds and none have call features, you mostly just track maturity dates. Callable bonds add complexity, an issuer can redeem early when rates drop, returning your principal before you expected and forcing reinvestment at lower yields. Sticking with noncallable bonds, as Fidelity’s experts recommend, eliminates that variable entirely.

Life changes, retirement, inheritance, a shift in spending needs, may mean adjusting the ladder’s length or allocation rather than maintaining the original structure indefinitely. Pairing a bond ladder with other income sources fits neatly into the retirement “bucket” framework, where the ladder covers short-to-medium term cash needs while growth assets handle longer horizons. If you’re still building toward retirement, reading about prioritizing retirement savings can help clarify where a ladder fits in your overall plan.

Frequently Asked Questions

How much money do I need to start a bond ladder?

With Treasuries or CDs, you can technically start with as little as $10,000 to $20,000 spread across a few maturities. The practical threshold for a diversified corporate bond ladder, where you need exposure to multiple issuers to manage credit risk, is closer to $100,000 to $250,000. Below that range, sticking to Treasuries, CDs, or maturity-date ETFs like BulletShares avoids the credit concentration problem without sacrificing the staggered-maturity structure.

Does a bond ladder protect against inflation?

Standard nominal bonds do not adjust for inflation. If inflation runs above your coupon rate, your real purchasing power erodes over the ladder’s life. One practical response is adding Treasury Inflation-Protected Securities (TIPS) as some rungs in the ladder. TIPS principal adjusts with the Consumer Price Index, so your maturity payment rises with inflation. A hybrid ladder, TIPS for shorter maturities where inflation risk is more immediate, nominal Treasuries for longer rungs, gives both inflation sensitivity and yield without going all-in on either.

Can I build a bond ladder inside an IRA or 401(k)?

Yes, and it can be a good fit for tax-deferred accounts. In an IRA, interest income compounds without annual tax drag, which suits the regular coupon payments a ladder generates. One thing to skip in a retirement account: municipal bonds. Their federal tax exemption is irrelevant inside an IRA, so you’d be accepting lower yields for no benefit. Treasuries and investment-grade corporates are the more efficient choices there. If managing credit card debt is eating into investable cash, tackling that first makes sense, our guide on prioritizing and negotiating credit card debt covers the options.

What happens if I need cash before a bond matures?

You can sell individual bonds on the secondary market before maturity, but you’ll get the current market price, not par value. If rates have risen since you bought, that price will be below par. Treasuries sell at tighter spreads than corporates in most conditions, but there’s still a real cost to exiting early. This is the liquidity trade-off laddering asks you to accept. If your financial situation has unpredictable cash demands, keeping a separate emergency fund in liquid savings before committing capital to a ladder is the more prudent order of operations. For tips on building that cash buffer while also investing, starting investing with zero experience is a useful primer.

Is a bond ladder better than a bond index fund?

It depends on what you’re optimizing for. A bond index fund offers immediate diversification, full liquidity, and low fees with minimal setup. An individual bond ladder gives you a guaranteed return of principal at maturity, direct control over credit quality and duration, and no NAV risk if you hold to term. The ladder wins on certainty; the fund wins on simplicity and accessibility. For most investors who don’t need the explicit maturity-date certainty, a low-cost bond index fund or a set of maturity-date ETFs delivers most of the benefit at far lower complexity.