Fact-checked by the MyFinancial101 editorial team

Quick Answer

The paycheck to paycheck cycle traps 72.8% of Americans earning under $50,000, but breaking it on a modest income is possible. The most effective starting point is a bare-minimum budget that exposes spending leaks, followed by automating even $10–$20 per week into a dedicated savings account before expenses hit.

The paycheck to paycheck cycle is not a personal failure; it is a structural problem that disproportionately affects lower earners. According to LendEDU’s 2025 survey data, 72.8% of people earning under $50,000 report living paycheck to paycheck, compared to 44% among those earning $50,000–$99,000. That gap matters because it shows the cycle is income-sensitive, not just a matter of discipline.

The mechanics of breaking out are consistent even at modest income levels. What differs is the margin you have to work with and the sequencing of moves that actually hold.

Key Takeaways

- 72.8% of Americans earning under $50,000 live paycheck to paycheck, compared to 44% of those earning $50,000–$99,000, according to LendEDU’s 2025 survey.

- Roughly one-third of U.S. private-sector workers without employer retirement plans say they rarely or never have money left at month’s end, per a June 2025 Pew Charitable Trusts brief.

- Auditing fixed costs typically reveals 5–10% of income that can be redirected without meaningful lifestyle change, before any income increase is needed.

- The Earned Income Tax Credit can return $2,000–$7,800 per year to eligible working families, according to the IRS EITC resource center.

- Automating $15–$20 per week into a no-fee savings account builds a $780–$1,040 emergency buffer in one year, enough to cover most single-incident expenses without borrowing.

- A wage increase from $17 to $19 per hour adds roughly $320 per month at full-time hours, more than most lean budgets can recover through cuts alone.

Why Modest Incomes Make the Paycheck-to-Paycheck Trap Especially Sticky

Fixed costs consume a far higher share of income for lower earners, leaving almost no room for error. When rent, a car payment, and childcare together claim 60–70% of a household’s take-home pay, even a single irregular expense, a car repair, a medical co-pay, can wipe out whatever thin cushion exists.

This is a margin problem, not a budgeting problem in the traditional sense. A household earning $2,800 per month after taxes faces the same rent market as one earning $5,000. The difference is that the lower-earning household has perhaps $200–$400 left after essentials; the higher earner has $1,500. One group has room to absorb mistakes; the other does not.

The data reinforces this. A June 2025 Pew Charitable Trusts brief found that roughly one-third of U.S. private-sector workers without employer-sponsored retirement plans say they rarely or never have money left over at month’s end. Among Hispanic workers in that same group, the share climbs to 42%. These are workers already excluded from one of the primary wealth-building tools available to middle-income earners; the cycle compounds quickly.

There is an honest concession worth stating upfront: on truly modest incomes, expense discipline alone rarely solves the problem. Sustainable progress almost always requires some combination of smarter spending, income growth, and benefit optimization working together.

Key Takeaway: Fixed costs leave households earning under $50,000 with almost no financial buffer. LendEDU’s 2025 data shows 72.8% of that income group lives paycheck to paycheck, compared to 44% among those earning $50,000–$99,000, a gap that reflects structural margin differences, not just spending habits.

How to Map Your True Monthly Numbers Without Overwhelm

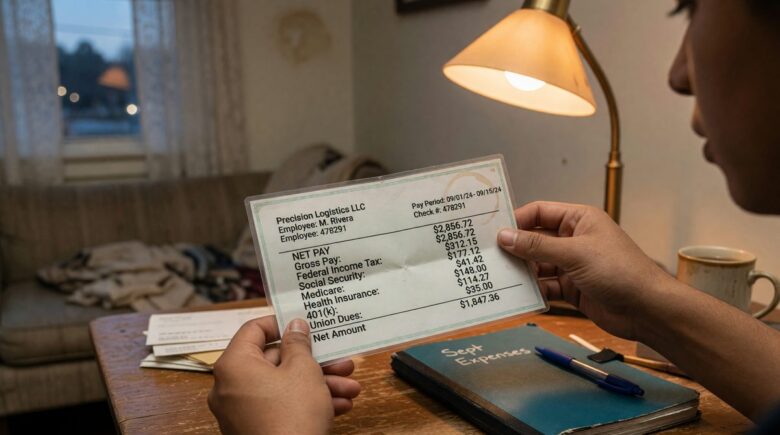

Start with one number: your actual take-home pay after taxes, not gross income. Then list every fixed obligation, rent or mortgage, car payment, insurance, minimum debt payments, and subtract them. What remains is your real working margin, and for many households it is smaller than expected.

This exercise frequently surfaces what financial counselors call “spending leaks”: subscriptions that auto-renew, convenience purchases that feel small individually but total $80–$150 per month, and irregular bills like annual fees that were never budgeted for. Awareness of these leaks, before any action is taken, often reveals 5–10% of income that can be redirected without any meaningful lifestyle change.

Tools That Work for Busy Schedules

A paper notebook, a free spreadsheet, or a no-fee app like Mint or YNAB’s free tier all accomplish the same goal. The tool matters far less than the habit of reviewing it. A weekly 15-minute check-in, Sunday evening or payday morning, is enough to stay current. Shift workers and parents with irregular schedules often find that a one-page budget template, reviewed once per paycheck rather than monthly, fits real life better than calendar-based systems.

The Consumer Financial Protection Bureau’s free budgeting and spending-tracker tools are genuinely useful here, especially for people who have never tracked spending before. They are plain, printable, and do not require a bank account login.

Key Takeaway: Mapping fixed costs against actual take-home pay typically reveals 5–10% in redirectable spending. The CFPB’s free budgeting tools offer a no-login starting point for anyone who has never formally tracked where their money goes.

Shrinking Expenses and Maximizing Benefits You Already Qualify For

On a tight budget, the highest-return moves target fixed costs first, not daily spending. Renegotiating a car insurance premium, switching to a no-fee checking account, or calling a utility provider to ask about budget billing plans can each save $20–$80 per month with a single phone call or account switch. These savings are permanent; cutting one coffee is not.

Groceries are the second lever. Strategies like shopping from a weekly store circular, buying staple proteins and grains in larger quantities, and using store-brand items for most categories routinely trim 15–25% from a grocery bill without changing what a household eats. Our guide on how coupon stackers are beating inflation covers specific stacking tactics that work even on small orders.

Government Benefits as a Parallel Strategy, Not a Last Resort

Many households living paycheck to paycheck qualify for assistance programs they have never applied for. The Earned Income Tax Credit (EITC) can return $2,000–$7,800 per year to eligible workers; a family of three earning $45,000 may qualify for more than $5,000 in refundable credit. If your household qualifies for SNAP, LIHEAP utility assistance, or WIC, using those benefits frees up cash that would otherwise have gone to groceries and utilities. Our article on how LIHEAP can help with rising utility costs explains the application process and income thresholds in detail.

These programs are part of the income side of the equation. Treating them as a last resort while cutting groceries to near zero is a false economy that increases stress and rarely produces lasting results.

| Expense Category | Typical Monthly Cost | Realistic Savings Potential |

|---|---|---|

| Car Insurance | $180–$260 | $25–$75/month (rate shop + bundling) |

| Groceries (family of 3) | $600–$750 | $90–$185/month (store brands + circulars) |

| Subscriptions | $80–$140 | $40–$90/month (audit + cancel) |

| Utilities | $180–$280 | $30–$60/month (budget billing + LIHEAP) |

| Bank Fees | $12–$35 | $12–$35/month (switch to no-fee account) |

Key Takeaway: Targeting fixed costs before daily spending produces the largest permanent savings. The EITC alone can return $2,000–$7,800 annually to eligible working families; details on qualifying thresholds are available from the IRS EITC resource center.

Building Your First Buffer: The $500 That Changes Everything

A $500–$1,000 starter emergency fund does something mathematically simple but psychologically profound: it converts the next unexpected expense from a debt event into a cash event. Without that buffer, a $400 car repair goes onto a credit card at 24% APR. With it, the repair is covered and the fund is rebuilt over the following weeks.

The CFPB’s emergency fund guide specifically recommends setting achievable savings goals even when living paycheck to paycheck or with irregular income, noting that small, consistent deposits build both the account balance and the habit itself. This sequencing matters. The habit, not the dollar amount, is what sustains progress.

The Arithmetic of Small Transfers

Here is a worked example. At $15 per week, automated on payday, a household accumulates $780 over 52 weeks. That covers most single-incident emergencies, a flat tire, a copay, a utility reconnection fee, without borrowing. At $20 per week, the fund reaches $1,040 in a year. Neither amount requires an income increase; both require only that the transfer happens before discretionary spending does.

The account matters too. A no-fee, high-yield savings account at an online bank like Ally or Marcus keeps the money accessible but not immediately visible in a checking account, which reduces the temptation to spend it. Avoid any account with a minimum balance requirement; a fee that triggers when the balance drops below $500 defeats the purpose entirely.

One honest caveat: this approach assumes at least some discretionary margin exists each week. For households where fixed costs genuinely consume every dollar of take-home pay, building even a $15 weekly transfer may require an income-side change first, whether that is a wage increase, a second income source, or qualifying for a benefit program that frees up cash currently going to groceries or utilities.

Once the starter buffer is in place, the next move is addressing high-interest debt. Our breakdown of how to prioritize and negotiate credit card debt covers sequencing strategies that work alongside, not instead of, building savings.

The CFPB recommends building an emergency fund by setting achievable savings goals even when living paycheck to paycheck or with irregular income, an approach designed specifically for households where margin is thin and consistency is harder to maintain than the goal itself. Full guidance is available in their Essential Guide to Building an Emergency Fund.

Key Takeaway: Automating just $15–$20 per week into a separate no-fee savings account builds a $780–$1,040 emergency buffer in one year, enough to cover most single-incident expenses without going into debt. The CFPB recommends this approach specifically for irregular-income and paycheck-to-paycheck households.

Can You Boost Income Without Burning Out?

Yes, but the options that last are ones that fit around existing obligations rather than adding unsustainable hours. Low-barrier income sources, freelance tasks on platforms like Fiverr or TaskRabbit, selling unused items, picking up shift-swap hours, or taking on seasonal work, can realistically add $200–$500 per month without requiring new credentials or equipment.

For those open to skill-adjacent work, our roundup of $19+ hourly jobs hiring now in 2026 identifies specific sectors with genuine openings at livable wages. A single income-side improvement, even a shift from $17 to $19 per hour, adds roughly $320 per month at 40 hours per week, more than most households can realistically cut from an already lean budget.

Tax refunds and credits are another income-side lever that many households leave on the table. The EITC, the Child Tax Credit, and free filing through the IRS Free File program are each worth auditing every year. Our guide on free IRS tax help and one credit families overlook walks through exactly which credits are most commonly missed by lower-income filers.

Key Takeaway: A wage increase from $17 to $19 per hour adds roughly $320 per month after taxes, more than most tight budgets can achieve through cuts alone. Sectors actively hiring at $19+ per hour in 2026 offer a realistic income path for workers without advanced credentials.

Frequently Asked Questions

How long does it realistically take to break the paycheck to paycheck cycle on a modest income?

Most households making meaningful, consistent changes see a measurable shift within 6–12 months. Building a $500 starter emergency fund is typically the first milestone, achievable in 4–6 months at $20–$25 per week in automated transfers. Full financial stability, meaning consistent savings and manageable debt, usually takes 12–18 months when starting with under $3,000 in monthly take-home pay.

Is it possible to save money when there is literally nothing left at the end of the month?

Start by auditing recurring charges before assuming there is truly nothing left. Subscriptions, unused memberships, and auto-renewing services frequently account for $60–$120 per month that is not mentally tracked as a regular expense. Even redirecting $10 per week to a separate savings account before spending begins rewires the habit and produces results over time.

What government programs can help someone living paycheck to paycheck?

The most commonly underused programs for lower-income households are the Earned Income Tax Credit, SNAP food assistance, LIHEAP for utility bills, and WIC for families with young children. Income eligibility thresholds were updated in 2026; our article on rising poverty guidelines in 2026 details who now qualifies and how to apply.

Should I pay off debt or build an emergency fund first?

Build the starter fund first, then attack debt. A $500–$1,000 buffer prevents the most common reason people fall back into debt: an unexpected expense that has nowhere else to go except a credit card. Once that buffer exists, direct all extra cash toward the highest-interest debt using the avalanche method, while maintaining minimum payments on everything else.

Sources

- Consumer Financial Protection Bureau, An Essential Guide to Building an Emergency Fund

- Consumer Financial Protection Bureau, Outreach Materials: Budgeting and Spending Tracker Tools

- Pew Charitable Trusts, Workers Without Access to Retirement Benefits Struggle to Build Wealth (2025)

- IRS, Earned Income Tax Credit: Questions and Answers

- IRS, Free File: Do Your Federal Taxes for Free

- IRS, Child Tax Credit

- Benefits.gov, Low Income Home Energy Assistance Program (LIHEAP)

- USDA Food and Nutrition Service, Supplemental Nutrition Assistance Program (SNAP)

- USDA Food and Nutrition Service, WIC Program

- Federal Reserve, Report on the Economic Well-Being of U.S. Households (SHED)

- U.S. Bureau of Labor Statistics, Earnings and Wages Data

- Urban Institute, Low-Income Working Families Initiative

- National Foundation for Credit Counseling, Budgeting and Savings Resources

- FDIC, Money Smart Financial Education Program