Fact-checked by the MyFinancial101 editorial team

Key Takeaways

- Short-term capital gains (assets held one year or less) are taxed as ordinary income, with rates up to 37% in 2025, while long-term gains top out at just 20% for most investors.

- Single filers with taxable income at or below $48,350 in 2025 pay 0% on long-term capital gains, a genuinely useful bracket to target through careful income planning.

- The 15% long-term rate applies to most middle-income investors; the 20% rate only kicks in above $533,400 for single filers in 2025.

- Higher earners face an additional 3.8% Net Investment Income Tax (NIIT) on top of regular capital gains rates once modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly).

- Collectibles, coins, art, stamps, are taxed at a maximum of 28% even when held long-term, a rate many investors overlook when building diversified portfolios.

- Reporting capital gains on the wrong IRS form, or missing cost basis adjustments, is one of the most common triggers for IRS notices that result in inflated tax bills.

In This Guide

- What Is Capital Gains Tax and Why It Matters

- Short-Term vs. Long-Term: The One-Year Rule Explained

- 2025 Short-Term Capital Gains Tax Rates

- 2025 Long-Term Capital Gains Tax Rates and Brackets

- How to Calculate Your Capital Gains Tax Bill

- Special Asset Classes: Crypto, Collectibles, and Real Estate

- Smart Ways to Reduce Your Capital Gains Tax

- State Capital Gains Taxes: What Federal Rules Don’t Cover

- How Capital Gains Affect Income-Tested Benefits

- Reporting Capital Gains on Your Tax Return

In 2025, the difference between selling a stock after 364 days versus 366 days can cost a typical middle-income investor thousands of dollars in extra taxes. That single day changes whether your profit is taxed at your ordinary income rate, potentially as high as 37%, or at the preferential long-term capital gains tax rates that top out at 20% for most people. Few decisions in personal investing carry that kind of consequence from a single calendar day.

Capital gains taxes affect far more Americans than the investor class alone. A 2025 IRS guidance update confirmed that long-term rates remain capped at 15% for the vast majority of filers, yet surveys consistently show that fewer than half of retail investors can correctly identify which rate applies to their portfolio. Meanwhile, the average household’s exposure to taxable investment accounts has grown steadily as employer pensions vanish and self-directed retirement shortfalls push more people into taxable brokerage accounts.

This guide breaks down exactly how short-term and long-term capital gains are taxed in 2025, including the precise income thresholds by filing status, the special rates for assets like cryptocurrency and collectibles, how state taxes layer on top of federal rules, and what to do before year-end to legally reduce your bill. After reading, you will be able to calculate your estimated capital gains liability, identify whether you qualify for the 0% bracket, and decide which assets to sell, and when.

What Is Capital Gains Tax and Why It Matters

Many investors focus exclusively on investment returns while treating the tax consequence as an afterthought, a mistake that can quietly erase 15% to 37% of a profitable sale. A capital gain is the profit you realize when you sell a capital asset for more than you paid for it. Capital assets include stocks, bonds, mutual funds, exchange-traded funds, real estate, cryptocurrency, collectibles, and business interests. The gain is the difference between your cost basis (what you paid, including commissions) and your sale proceeds (what you received, net of selling costs).

Realized vs. Paper Gains

A critical distinction: capital gains taxes only apply to realized gains, profits from assets you have actually sold. A position sitting in your brokerage account that has tripled in value is a paper gain. The IRS cannot tax it until you sell. This matters practically: you can hold a winning position indefinitely without triggering a tax event, and you can time your sales strategically to fall in a lower-income year or within the 0% bracket threshold.

Paper gains also affect financial planning decisions beyond pure taxes. If you are managing household income to qualify for certain credits or subsidies, an unexpected large sale can push you over key thresholds. That interaction is covered in more detail in the section on income-tested benefits below.

Everyday Portfolios Are Not Exempt

Capital gains taxes are not just a concern for wealthy investors. Anyone who sells shares in a taxable brokerage account, rebalances a portfolio, liquidates an inherited position, or sells a rental property faces a potential capital gains bill. Even selling shares to cover an unexpected expense triggers reporting requirements. If you are new to investing, the guide on how to start investing with zero experience covers the account types that can shelter gains entirely, a good first line of defense before tax planning ever becomes necessary.

Inherited assets receive a “stepped-up” cost basis to their fair market value on the date of death. That means a stock your parent bought for $5 per share and left to you at $80 per share carries a basis of $80, eliminating decades of embedded gain from your tax bill when you sell.

Short-Term vs. Long-Term: The One-Year Rule Explained

The tax code draws a hard line at one year. Assets held for one year or less generate short-term capital gains; assets held for more than one year generate long-term capital gains. That “more than” language is exact: if you buy shares on June 15, 2024, the first eligible sale date for long-term treatment is June 16, 2025, not June 15.

How the Holding Period Is Counted

The IRS counts holding periods by starting the day after the purchase date and ending on, and including, the sale date. So if you bought on January 10, 2024, and sold on January 10, 2025, the sale date counts as exactly one year and one day: long-term. If you sold on January 9, 2025, that is 364 days: short-term. Brokerage account statements typically display a “date acquired” and indicate whether a lot is short-term or long-term, but it is worth verifying before placing a sale order, especially when shares were acquired on multiple dates.

Inherited assets are automatically treated as long-term, regardless of how long you or the original owner held them. Gifted assets carry over the donor’s holding period and cost basis, which can work in your favor or against you depending on the circumstances.

Common Mistakes That Reset the Clock

Three mistakes commonly short-circuit long-term treatment. First, selling covered calls and having shares “called away” can reset the holding period clock on those specific shares. Second, when you reinvest dividends automatically, each reinvestment creates a new tax lot with its own purchase date and basis, meaning some lots may be short-term even inside a position you have held for years. Third, the wash-sale rule disallows a loss if you repurchase substantially identical securities within 30 days before or after the sale, and a disallowed loss can also affect basis and holding period calculations for the replacement shares.

Automated dividend reinvestment plans (DRIPs) create dozens of small tax lots over time, each with different purchase dates and basis amounts. When you eventually sell the position, some lots may be short-term even if the original purchase was years ago. Review lot-level detail before selling any position with a long history of reinvested dividends.

2025 Short-Term Capital Gains Tax Rates

Short-term capital gains receive no preferential treatment. They are added directly to your other ordinary income and taxed at whatever marginal bracket that combined income reaches. For 2025, that means rates range from 10% to 37% under the Tax Foundation’s 2025 bracket tables. The practical implication: a high-income earner who sells a stock held for 11 months will owe more than three times the tax owed by a lower-income investor who waited a few more weeks.

2025 Ordinary Income Brackets (Short-Term Rates)

| Tax Rate | Single Filer Taxable Income | Married Filing Jointly |

|---|---|---|

| 10% | Up to $11,925 | Up to $23,850 |

| 12% | $11,926 – $48,475 | $23,851 – $96,950 |

| 22% | $48,476 – $103,350 | $96,951 – $206,700 |

| 24% | $103,351 – $197,300 | $206,701 – $394,600 |

| 32% | $197,301 – $250,525 | $394,601 – $501,050 |

| 35% | $250,526 – $626,350 | $501,051 – $751,600 |

| 37% | Over $626,350 | Over $751,600 |

A Real-World Short-Term Tax Example

Suppose you are a single filer with $80,000 of W-2 income and you sell stock for a $15,000 short-term gain in 2025. Your total ordinary income becomes $95,000. The first $48,475 of taxable income (after the standard deduction) is taxed in the 10% and 12% brackets; income above that enters the 22% bracket. The $15,000 gain pushes you from approximately $62,000 taxable income to $77,000 taxable income, with the bulk of that gain taxed at 22%. Your extra federal tax from the gain: roughly $3,300. Had you waited to qualify for long-term treatment at 15%, the same $15,000 gain would cost about $2,250 in federal tax, a $1,050 difference for holding a few more weeks.

The top short-term capital gains rate in 2025 is 37%, the same as the top ordinary income bracket. For a single filer earning over $626,350, a $100,000 short-term gain costs $37,000 in federal tax alone, versus $20,000 at the long-term rate. That $17,000 gap is the price of impatience.

2025 Long-Term Capital Gains Tax Rates and Brackets

Long-term capital gains have their own separate rate schedule, independent of the ordinary income brackets. Three rates apply to most investors: 0%, 15%, and 20%, determined by taxable income, not gross income, not AGI, but taxable income after deductions. According to the IRS Topic 409 guidance for 2025, the tax rate on most net capital gain is no higher than 15% for most individuals, a statement that holds up for the large middle swath of American earners.

2025 Long-Term Capital Gains Brackets by Filing Status

| Long-Term Rate | Single Filer Taxable Income | Married Filing Jointly | Head of Household |

|---|---|---|---|

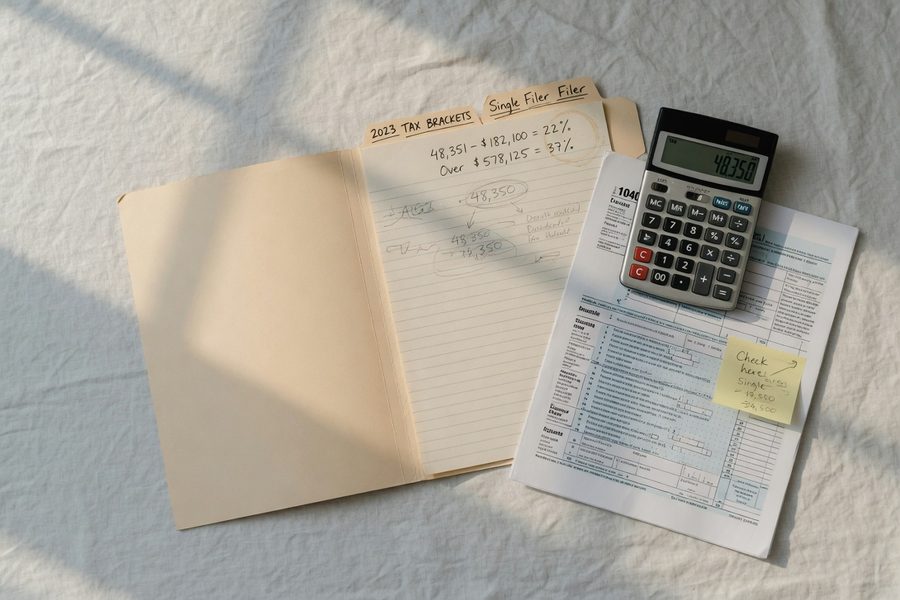

| 0% | Up to $48,350 | Up to $96,700 | Up to $64,750 |

| 15% | $48,351 – $533,400 | $96,701 – $600,050 | $64,751 – $566,700 |

| 20% | Over $533,400 | Over $600,050 | Over $566,700 |

Who Actually Pays 0%?

The 0% bracket is real and reachable for more households than most people assume. A single filer with $48,350 or less in taxable income pays zero federal capital gains tax on long-term gains. To reach that threshold, you subtract the 2025 standard deduction ($15,000 for single filers) from gross income, meaning a single person with $63,350 in wages and no other deductions sits exactly at the 0% threshold. Retirees drawing down modest portfolios, part-time workers with significant unrealized gains, and early retirees using the Roth conversion ladder strategy frequently qualify.

Married filing jointly filers have a threshold of $96,700 in taxable income, a level that, after the $30,000 joint standard deduction, corresponds to approximately $126,700 in gross income. Strategic timing of asset sales in low-income years, or in the year of a job transition, can push long-term gains entirely into this 0% band.

2025 vs. 2024: What Changed with Inflation Adjustments

| Bracket / Threshold | 2024 Single Filer | 2025 Single Filer | Change |

|---|---|---|---|

| 0% ceiling | $47,025 | $48,350 | +$1,325 |

| 15% ceiling | $518,900 | $533,400 | +$14,500 |

| 20% threshold | $518,901+ | $533,401+ | +$14,500 |

The inflation adjustments for 2025 are modest but meaningful: the 0% ceiling for single filers increased by $1,325 compared to 2024. For investors actively managing income to stay within the 0% band, that extra room is worth knowing.

How to Calculate Your Capital Gains Tax Bill

The calculation follows a specific sequence, and skipping steps is how people end up either overpaying or triggering IRS notices. Work through it in order.

Step 1: Determine Cost Basis and Net Gain

Start with your cost basis: the original purchase price plus any commissions, reinvested dividends, or return-of-capital adjustments. Subtract the basis from your net sale proceeds (sale price minus selling commissions). The result is your gross gain or loss. If you have multiple lots of the same security purchased at different prices and dates, each lot is treated separately. Your brokerage’s Form 1099-B should list cost basis for covered securities, but always verify, basis errors on 1099-Bs do happen.

Step 2: Net Gains Against Losses

Before applying any rate, you must net gains and losses within each category. Short-term gains offset short-term losses first; long-term gains offset long-term losses first. If one category produces a net loss after that process, it can offset net gains in the other category. A net capital loss of up to $3,000 can offset ordinary income in the current year, with any remaining loss carried forward to future years, indefinitely.

What I see in practice: Clients are often surprised to learn that a net short-term loss offsets long-term gains dollar for dollar. Running a careful year-end review of all tax lots, not just obvious losers, regularly uncovers $2,000 to $8,000 in net loss carryforwards that dramatically cut the following year’s bill.

Step 3: Add the 3.8% Net Investment Income Tax

The Net Investment Income Tax (NIIT), established under the Affordable Care Act, adds 3.8% to net investment income for higher earners. It applies to the lesser of (a) net investment income or (b) the amount by which modified adjusted gross income (MAGI) exceeds $200,000 for single filers or $250,000 for married filing jointly. These thresholds are not indexed for inflation and have not changed since 2013, meaning more households are subject to the NIIT each year as incomes rise.

For a single filer with $220,000 MAGI and $30,000 in long-term capital gains, the NIIT applies to the lesser of $30,000 (net investment income) or $20,000 (the amount MAGI exceeds $200,000). So the NIIT applies to $20,000, generating an extra $760 in tax. The effective long-term capital gains rate for that filer becomes 15% + 3.8% = 18.8% on a portion of the gain. High earners at the very top can face an effective federal rate of 23.8% on long-term gains (20% + 3.8%).

The 3.8% NIIT threshold of $200,000 for single filers has never been adjusted for inflation since its introduction in 2013. In real purchasing-power terms, that threshold has eroded by roughly 30%, meaning a steadily growing share of households now face this surtax without any change in tax law.

Special Asset Classes: Crypto, Collectibles, and Real Estate

The standard 0%/15%/20% long-term rate schedule does not cover every asset. Three categories carry different rules, and ignoring them is costly.

Cryptocurrency

The IRS classifies cryptocurrency as property, not currency. Every sale, swap, or exchange of one cryptocurrency for another is a taxable event, and the holding period rules apply identically to stocks. Buy Bitcoin on March 1, 2024, sell it on March 1, 2025, and the gain is long-term. Trade that Bitcoin for Ethereum on February 28, 2025, and you have a short-term taxable event on the Bitcoin, plus a new cost basis in the Ethereum at the fair market value on the trade date. The complexity compounds quickly across high-frequency trading wallets. For a full breakdown of the risks involved with crypto as an asset class, see the MyFinancial101 guide on cryptocurrency investments: risks and benefits.

Collectibles and Qualified Small Business Stock

Collectibles, including coins, art, antiques, stamps, fine wines, and gems, carry a maximum long-term rate of 28% regardless of how long you hold them. That rate applies even if your income would otherwise put you in the 15% bracket. Qualified small business stock (Section 1202 stock) can sometimes be excluded entirely from gain recognition, but any taxable portion is also capped at 28%. Gains from the sale of certain real property where prior depreciation was claimed are taxed at 25%, a separate wrinkle covered in the next section. These higher rates on specific asset classes are easy to overlook, particularly for investors who assume the 0%/15%/20% schedule applies universally.

Real Estate: The Depreciation Recapture Trap

Rental property owners face a specific wrinkle: the portion of gain attributable to prior depreciation deductions, called unrecaptured Section 1250 gain, is taxed at a maximum rate of 25%, not the standard long-term rate. If you owned a rental property for 15 years and claimed $60,000 in depreciation deductions, up to $60,000 of your gain is taxed at 25% when you sell. This catches many landlords off guard, particularly those who aggressively depreciated improvements. The primary residence exclusion ($250,000 single / $500,000 joint) applies only to the non-depreciation portion of the gain.

Smart Ways to Reduce Your Capital Gains Tax

Tax minimization strategies exist, but each one has trade-offs, limits, or conditions that generic advice tends to gloss over. Here are the approaches that actually work, with the caveats named upfront.

Tax-Loss Harvesting

Tax-loss harvesting means deliberately selling positions at a loss to offset realized gains. It works best in volatile years when some holdings are down while others are up. The limitation: the wash-sale rule prevents you from buying back substantially identical securities within 30 days before or after the sale. You can buy a different but similar ETF to maintain market exposure while the 30-day window clears. Note that tax-loss harvesting only defers taxes, it reduces basis on replacement shares, so you pay more when you eventually sell those. The benefit is the time value of deferral, not permanent elimination.

Account Type Optimization

Holding highly appreciated or frequently traded assets inside tax-advantaged accounts (traditional IRA, Roth IRA, 401(k)) eliminates capital gains tax entirely on those holdings. Roth accounts are particularly powerful: growth and qualified withdrawals are tax-free. The trade-off is that tax-deferred accounts eventually generate ordinary income on withdrawal (traditional IRA/401(k)), which for some investors means swapping a 15% capital gains rate for a 22% or 24% income rate. Matching asset type to account type, a strategy called asset location, is one of the higher-impact moves available to investors who hold both taxable and tax-advantaged accounts. For background on long-term account strategy, the piece on saving for retirement over college addresses how to prioritize account types when resources are limited.

Strategic Timing of Sales

If your income will be lower next year due to retirement, a career transition, or a sabbatical, deferring a large gain to that lower-income year can shift you into a smaller bracket or even the 0% long-term band. Conversely, if you expect income to rise significantly, accelerating a gain into the current year at a lower rate can make sense. Neither move is universally correct, the decision depends on your projected multi-year income, marginal rate trajectory, and state tax situation.

Charitable investors can donate appreciated long-term stock directly to a charity instead of selling it. You receive a deduction for the full fair market value of the shares, and neither you nor the charity pays capital gains tax on the embedded appreciation. This is more tax-efficient than selling the stock and donating cash, provided you itemize deductions.

State Capital Gains Taxes: What Federal Rules Don’t Cover

Federal capital gains tax rates often get all the attention, but state taxes can add a significant second layer, and the variation between states is stark.

States That Tax Capital Gains as Ordinary Income

Most states that have an income tax treat capital gains as ordinary income, applying no separate preferential rate. California stands out at the extreme: the state’s top marginal income tax rate is 13.3%, applied to capital gains without distinction between short-term and long-term. A California resident in the top federal and state bracket faces a combined effective rate over 33% on long-term gains. New York adds up to 10.9% in state tax, plus New York City residents pay an additional local income tax of up to 3.876%. Oregon, Minnesota, and New Jersey also impose top rates above 9% on capital gains income.

States With No Capital Gains Tax

| State | Capital Gains Treatment | Top Marginal Rate on Gains |

|---|---|---|

| Florida | No state income tax | 0% |

| Texas | No state income tax | 0% |

| Nevada | No state income tax | 0% |

| Washington | 7% tax on long-term gains over $262,000 (2024 threshold) | 7% |

| New Hampshire | No tax on capital gains or wages | 0% |

| California | Ordinary income rates apply | 13.3% |

Washington state deserves a specific note: after years of legal challenges, its 7% excise tax on long-term capital gains above approximately $262,000 survived state Supreme Court review and is now in effect. The tax does not apply to real estate sales or retirement account distributions, but it applies to gains from stocks and bonds, a significant development for high earners in a state that previously had no income tax.

How Capital Gains Affect Income-Tested Benefits

This is an angle most tax guides skip, but it matters for a large segment of investors. Capital gains income, including long-term gains, counts toward modified adjusted gross income (MAGI) for purposes of several income-tested federal programs.

For Affordable Care Act premium tax credits, MAGI is the benchmark. Selling a large long-term position in a year when you are on a marketplace health plan can push your projected income above 400% of the federal poverty level, eliminating your subsidy entirely and creating a repayment obligation at tax time. The impact can reach several thousand dollars per year depending on plan cost and family size. Similarly, capital gains can affect eligibility thresholds for Medicare premium surcharges (IRMAA), which add $70 to $420 per month per person to Medicare Part B premiums for two years after the triggering income year. For more context on how income fluctuations affect federal program eligibility, see how rising poverty guidelines affect benefit eligibility.

A retiree who normally qualifies for a $600/month ACA premium subsidy could lose the entire credit by realizing a $40,000 long-term capital gain in a single year, depending on household size and income. Planning the timing of portfolio sales around anticipated health insurance status is one of the most underutilized strategies in retirement income planning.

Reporting Capital Gains on Your Tax Return

Accurate reporting is not optional, the IRS receives copies of all broker-issued 1099-B forms and cross-matches them against your return. Mismatches generate automated notices, and responding to them is time-consuming even when you are correct.

The Key Forms

Schedule D is the main form for reporting capital gains and losses. It summarizes totals from Form 8949, where each individual sale is listed with its proceeds, cost basis, and holding period classification. Brokers often provide a consolidated 1099-B that groups transactions, but you are still required to transfer each transaction, or a grouped summary with the correct code, to Form 8949. Transactions where basis is not reported to the IRS (non-covered securities, pre-2011 acquisitions, or transactions from some cryptocurrency platforms) must be entered separately with a different adjustment code.

Common Errors and IRS Matching Issues

Two errors show up repeatedly. First, taxpayers who receive a 1099-B showing gross proceeds but no cost basis sometimes report zero basis, generating a massively inflated gain. The basis is not on the 1099-B, but it does exist, in your purchase confirmation, mutual fund statements, or DRIP records. Second, wash-sale disallowed losses are often shown on the 1099-B but require an adjustment on Form 8949 to add back the disallowed amount to the replacement lot’s basis. Skipping that step understates your future basis. Getting tax preparation right for situations like these is one reason to consider professional help; the MyFinancial101 article on free IRS tax help and credits families overlook outlines no-cost filing resources if your situation is straightforward.

Estimated tax payments may be required if your capital gains liability will exceed $1,000 for the year and you do not have sufficient withholding to cover it. Underpayment penalties apply even if you pay the full amount by April 15. Investors who realize large mid-year gains should calculate whether a Q3 or Q4 estimated payment is needed to avoid penalties.

Real-World Example: Timing a Stock Sale to Hit the 0% Bracket

Consider an illustrative example: Maria, a 58-year-old single filer, took early retirement in late 2024. Her 2025 income consists of $35,000 from part-time consulting work. After claiming the standard deduction of $15,000, her taxable income is $20,000, well below the $48,350 threshold for the 0% long-term capital gains bracket.

Maria holds 500 shares of an index ETF she purchased in 2018 for $42 per share (total basis: $21,000). The shares are now worth $110 each (total value: $55,000). If she sells all 500 shares, her long-term gain is $34,000. Adding that gain to her $20,000 taxable income produces $54,000 total. The first $28,350 of the gain ($48,350 minus $20,000) falls within the 0% bracket and generates zero federal capital gains tax. The remaining $5,650 of the gain is taxed at 15%, producing a federal capital gains bill of $847.50 on a $34,000 gain.

Had Maria been in her peak earning years with $120,000 in W-2 wages, that same $34,000 gain would have been entirely in the 15% bracket, costing $5,100. Had she sold those shares after holding them for only nine months (short-term), the gain would have been added to her $120,000 wages and taxed at 22% to 24%, generating an estimated $7,480 to $8,160 in additional federal tax.

The before/after comparison: by retiring a year before realizing this gain, Maria reduced her federal capital gains tax from roughly $5,100 (long-term, peak income) to $847.50 (long-term, low income year), a $4,252 difference on a single sale, simply by aligning the timing of the sale with a low-income year. State tax would apply separately based on her state of residence.

Your Action Plan

-

Identify every taxable account where you hold appreciated assets

Pull statements from all brokerage, investment, and retirement accounts. Separate taxable accounts (where capital gains apply) from tax-advantaged accounts (IRA, Roth, 401(k), where gains are deferred or tax-free). Focus your capital gains planning exclusively on taxable accounts.

-

Check the holding period and classification for each position you are considering selling

Log into your brokerage account and review the lot-level detail for every position you plan to sell this year. Confirm whether each lot is classified as short-term or long-term. If any lots are within 30 to 60 days of crossing the one-year threshold, note those dates and build your sale schedule accordingly.

-

Project your 2025 taxable income before adding any capital gains

Estimate your wages, self-employment income, interest, ordinary dividends, and any other taxable income sources for the full year. Subtract your expected deductions (standard or itemized). The resulting figure is your “base” taxable income, which determines which capital gains bracket your gains will fall into when added on top.

-

Calculate the tax cost under short-term vs. long-term treatment for each planned sale

Using the rate tables in this article, run the numbers for each position at both your ordinary income rate and the applicable long-term rate. If the difference exceeds the cost of waiting, defer the sale. Be specific: use the actual gain amount, your filing status, and your projected taxable income from Step 3.

-

Scan all taxable positions for unrealized losses you can harvest before year-end

Identify any positions currently trading below your cost basis. Calculate whether harvesting those losses would offset gains you have already realized or plan to realize this year. Execute loss harvests before December 31, then wait 31 days before buying back the same or a substantially identical security to avoid the wash-sale rule. You can immediately buy a similar (not identical) fund to maintain your target asset allocation during that window.

-

Assess whether capital gains will affect your eligibility for income-tested programs

If you receive ACA premium tax credits, check whether realizing gains will push your MAGI above the 400% federal poverty level threshold for your household size. If you are on Medicare, check whether your projected MAGI will trigger IRMAA surcharges. If either applies, consult with a CPA or financial planner before executing large sales. The two-year IRMAA lookback period makes the timing especially important.

-

File correctly using Form 8949 and Schedule D, and pay estimated taxes if needed

Report each sale on Form 8949 with accurate proceeds, basis, acquisition date, and sale date. Summarize totals on Schedule D. If your projected federal capital gains liability exceeds $1,000 and your withholding will not cover it, make a Q3 or Q4 estimated tax payment using IRS Form 1040-ES to avoid underpayment penalties. Keep all trade confirmations and 1099-B forms for at least three years after the filing deadline of the return on which they appear.

Frequently Asked Questions

How long do I need to hold a stock to qualify for the long-term capital gains rate?

You must hold the asset for more than one year, meaning at least one year and one day. If you purchased shares on May 10, 2024, the earliest sale date that qualifies for long-term treatment is May 11, 2025. Selling on the exact anniversary date does not count as long-term under IRS rules.

Do I owe capital gains tax if I reinvest the proceeds instead of taking cash?

Yes. The taxable event occurs at the moment of sale, regardless of what you do with the proceeds afterward. Reinvesting the cash into another investment does not defer or eliminate the gain. The only exceptions are specific tax-deferred structures such as qualified opportunity zone investments, where reinvestment can defer and potentially reduce the gain under certain conditions.

Are capital gains taxed differently in my IRA or 401(k)?

Inside a traditional IRA or 401(k), there are no capital gains taxes on sales within the account. All withdrawals are eventually taxed as ordinary income, regardless of how the underlying assets performed. Roth accounts go further: qualified withdrawals are entirely tax-free, meaning decades of capital appreciation can be withdrawn without any capital gains or ordinary income tax. This is why asset location, placing your highest-growth, highest-turnover assets inside Roth accounts, is such a high-value strategy.

Can I deduct capital losses against my wages or salary?

Up to $3,000 of net capital losses per year can offset ordinary income such as wages, salary, or self-employment income. Any remaining loss beyond $3,000 carries forward to the next tax year indefinitely and retains its character (short-term or long-term) going forward. There is no time limit on capital loss carryforwards; they do not expire.

Is cryptocurrency taxed the same as stocks for capital gains purposes?

The IRS treats cryptocurrency as property, so the same short-term/long-term framework applies. Hold for more than a year and the preferential long-term rates apply; sell sooner and gains are ordinary income. The added complexity with crypto is that every trade, including swapping one coin for another, is a taxable event, and many platforms do not provide accurate cost basis tracking. Keeping your own transaction records is essential. State tax treatment of crypto gains follows the same rules as federal treatment in most states.

What happens if I forget to report a capital gain?

The IRS automatically receives a copy of your Form 1099-B from your broker and matches the proceeds against your tax return. If reported proceeds are missing from your return, you will likely receive a CP2000 notice proposing additional tax, often calculated on the full sale amount with zero basis, inflating the bill substantially. Responding to these notices requires documentation and time. Filing an amended return before an IRS notice arrives is always preferable; the penalties and interest on late or unreported gains can add up quickly.

Do capital gains affect my Social Security benefits?

Capital gains do not directly affect whether you receive Social Security benefits or the amount of your monthly payment. They can, however, affect how much of your Social Security income is taxable. Combined income (adjusted gross income plus nontaxable interest plus half of Social Security benefits) determines how much of your benefit is included in taxable income. A large capital gain in a single year can push combined income above $34,000 (single) or $44,000 (joint), causing up to 85% of Social Security benefits to become taxable for that year.

A single retiree with $28,000 in Social Security benefits and a $50,000 capital gain in one year could see up to $23,800 (85%) of those Social Security benefits become taxable, on top of the capital gains tax itself. Planning large asset sales in coordination with Social Security income can meaningfully reduce this compounding effect.

Sources

- Internal Revenue Service, Topic No. 409: Capital Gains and Losses

- Tax Foundation, 2025 Federal Tax Brackets and Rates

- TurboTax, Guide to Short-Term vs. Long-Term Capital Gains Taxes

- Internal Revenue Service, About Schedule D (Form 1040): Capital Gains and Losses

- Internal Revenue Service, About Form 8949: Sales and Other Dispositions of Capital Assets

- Internal Revenue Service, Instructions for Schedule D (2024)

- Internal Revenue Service, Publication 550: Investment Income and Expenses

- Internal Revenue Service, Questions and Answers on the Net Investment Income Tax

- KFF (Kaiser Family Foundation), Explaining Health Care Reform: Questions About Health Insurance Subsidies