Fact-checked by the MyFinancial101 editorial team

Key Takeaways

- The IRS established 3.4 million new installment agreements in fiscal year 2024 but accepted only 7,199 Offers in Compromise, a ratio that should calibrate your expectations before you apply for either.

- In FY 2025, taxpayers proposed 38,797 OICs; the IRS accepted just 5,464 of them, worth a combined $98.1 million in settled debt.

- Short-term payment plans (under $100,000, paid within 180 days) carry no user fee for individuals, while OIC application fees and deposits are non-refundable even if the IRS rejects your offer.

- Interest and penalties continue accruing on your full original balance during the entire OIC review period, which typically runs 6 to 12 months.

- OIC acceptance requires you to stay tax-compliant for five consecutive years after the IRS approves your offer; violating that requirement can reinstate the original debt.

- If your OIC is rejected and you had an existing installment agreement, that agreement reinstates automatically with no new setup fee, provided no new tax debt has been added.

In This Guide

- How to Quickly Assess If You Qualify for Either Program

- IRS Payment Plan Options Explained

- Offer in Compromise: When the IRS Will Actually Settle for Less

- Head-to-Head Comparison: Cost, Timeline, and Approval Odds

- Which Option Leaves You Better Off Long-Term

- Applying Step by Step and What Happens If You’re Rejected

- When Neither Option Makes Sense

- Professional Help Thresholds and Avoiding Tax Relief Scams

In fiscal year 2024, the IRS collected more than $16 billion through installment agreements, a 12% jump from the prior year, while simultaneously accepting fewer than 7,200 Offers in Compromise out of millions of taxpayers who owed back taxes. That single data point reshapes the entire conversation about IRS payment plan options: for most people, a structured payment arrangement is not a fallback after failing at an OIC. It is the primary resolution tool, and understanding why matters more than most tax relief content admits.

Tax debt in the United States has been climbing steadily. Individual balance-due accounts exceeded $688 billion in outstanding assessments as of fiscal year 2023, according to the IRS annual Data Book. That figure encompasses penalties, interest, and the underlying tax owed, and for households already stretched by inflation and high consumer debt (Federal Reserve data showed credit card balances hit a record $1.14 trillion in late 2024), the prospect of a lump-sum IRS payment feels impossible. Advertisers know this. The airwaves are full of promises about “settling for pennies on the dollar,” a phrase that describes a real IRS program but one with a 14% acceptance rate in FY 2025. The gap between the marketing and the math is where most taxpayers get hurt.

This guide walks through both programs in full detail: how each is structured, what the real qualification standards look like, what it costs to apply and maintain each arrangement, and, critically, which one actually leaves you in better financial shape over a five- to ten-year horizon. By the time you finish reading, you will be able to size up your own situation against the IRS’s own criteria, build a realistic picture of your monthly obligations under each path, and recognize the warning signs that a tax relief firm is overpromising.

How to Quickly Assess If You Qualify for Either Program

The Filing Requirement That Disqualifies More People Than You’d Expect

Before the IRS will consider any formal resolution, payment plan or OIC, you must be current on all required tax returns. Unfiled returns for any year mean the IRS will not process an installment agreement application, and it will return an OIC submission without review. This is not a technicality that gets waived. It is the first filter, and it catches a meaningful share of people who contact tax professionals believing they are ready to negotiate.

For an OIC specifically, you must also be current on any estimated tax payments due for the current year. Self-employed taxpayers who have been ignoring quarterly payments while negotiating a settlement for prior years will find their OIC rejected for this reason alone. Revenue officers call this “pre-qualifier” compliance, and the agency publishes a free OIC Pre-Qualifier Tool that checks these boxes before you invest time in a full application.

Income, Assets, and the Equity Problem

Payment plans have no strict income or asset ceiling. If you owe the money, the IRS wants a payment arrangement. Offers in Compromise operate differently: the agency evaluates what it can realistically collect from you within the remaining collection statute period (generally ten years from the assessment date). If the net equity in your assets, home equity, investment accounts, retirement accounts above certain exemptions, vehicle equity, plus your projected disposable monthly income exceeds your tax debt, the IRS will reject the OIC because it believes it can collect the full amount through other means.

High home equity kills more OIC applications than any other single factor. A taxpayer who owes $45,000 in back taxes but holds $60,000 in home equity will almost certainly receive a rejection, even if their monthly cash flow is genuinely tight. Revenue officers do not discount asset equity because collecting it would be inconvenient; they weigh whether those assets could be liquidated or borrowed against. Homeowners in markets where Zillow-tracked values have risen sharply often discover their equity disqualifies them without realizing it. If you are in this situation, understanding how to prioritize competing debts before applying is essential groundwork.

Active bankruptcy proceedings disqualify you from both an installment agreement and an OIC. The IRS will not process either application while an automatic bankruptcy stay is in effect. You must resolve the bankruptcy first or obtain court permission before pursuing IRS relief.

IRS Payment Plan Options Explained

Short-Term Plans: The Fastest Path Out

A short-term payment plan gives individual taxpayers up to 180 days to pay a balance under $100,000 in full. There is no setup fee for individuals who apply online. You will still owe the current IRS interest rate (the federal short-term rate plus 3 percentage points, compounding daily, 8% as of mid-2025) plus the failure-to-pay penalty of 0.5% per month, but those charges stop accruing once the balance hits zero. For someone who can genuinely clear their debt in four to six months, this is the lowest-cost formal resolution available.

The online application takes under 15 minutes through the IRS’s Online Payment Agreement system. Approval is immediate. No tax professional is required for a straightforward short-term plan, though anyone with complicated circumstances, multiple tax years, business debt, or a prior default, should consult a CPA or enrolled agent before applying.

Long-Term Installment Agreements: The Standard Route

For taxpayers who cannot pay within 180 days, a long-term installment agreement spreads payments over up to 72 months. Balances under $50,000 qualify for what the IRS calls a streamlined installment agreement, which requires no financial disclosure and no negotiation. Under that program, the minimum monthly payment works out to roughly 1/72 of the total balance owed. On a $36,000 balance, that is $500 per month before additional interest accrual is factored in.

Balances between $50,001 and $250,000 can qualify for a similar plan running up to 84 months, though these are reviewed differently and may require some financial documentation. Above $250,000, you enter a fully negotiated agreement that requires Form 433-A (Collection Information Statement) and a thorough review of your income and expenses. Setup fees run $31 for online direct debit enrollment, $107 for other online agreements, and $225 for agreements set up by phone or mail.

The IRS collected more than $16 billion through installment agreements in fiscal year 2024, a 12% increase over FY 2023. That volume reflects 3.4 million new agreements established in a single year.

The Hidden Cost: Interest and Penalties Keep Running

This is the most important caveat about payment plans that comparison articles routinely understate. An installment agreement does not freeze your balance. While you are paying, the IRS continues charging its current interest rate on the outstanding amount plus the 0.5% monthly failure-to-pay penalty (which drops to 0.25% once an agreement is formally in place). On a $40,000 balance over 72 months at roughly 8% annual interest, a taxpayer can end up paying $10,000 to $13,000 more than the original debt, depending on the rate environment and payment speed.

Defaulting on an installment agreement triggers reinstatement fees, a new review, and potential lien filing or enforcement action. A single missed payment does not automatically cancel the agreement, but two missed payments in a 12-month period typically will. Keeping direct debit active through a bank account at an institution like Chase, Bank of America, or a local credit union is the most reliable way to avoid an accidental default caused by a forgotten due date.

Offer in Compromise: When the IRS Will Actually Settle for Less

The Three Grounds for Acceptance

An OIC is accepted on one of three grounds: Doubt as to Collectibility (the agency cannot reasonably expect to collect the full amount), Doubt as to Liability (there is a genuine dispute about whether the tax was correctly assessed), or Effective Tax Administration (collecting the full amount would create an exceptional and demonstrably unfair hardship). In practice, Doubt as to Collectibility drives the overwhelming majority of accepted offers. Doubt as to Liability is rare and requires concrete factual grounds to contest the assessment itself. Effective Tax Administration is rarer still, generally reserved for situations involving serious illness, disability, or other extraordinary circumstances.

Per the IRS, “an offer in compromise allows you to settle your tax debt for less than the full amount you owe if you can’t pay your full tax liability or doing so creates a financial hardship.” That language is precise. This is not a discount program. It is a collectibility calculation dressed in more sympathetic terms.

Reasonable Collection Potential: The Number That Actually Decides Your Case

Your offer’s minimum acceptable amount is determined by the IRS’s calculation of your Reasonable Collection Potential (RCP). RCP equals the net realizable equity in your assets (typically 80% of asset fair market value minus any secured debt) plus your monthly disposable income multiplied by either 12 (if you offer a lump sum within 5 months) or 24 (if you propose periodic payments over 24 months). If your calculated RCP is $35,000 and you owe $80,000, an offer of $35,000 could in theory be accepted. If your calculated RCP equals or exceeds your full balance, the OIC will be rejected.

Many people who run through the IRS Pre-Qualifier Tool misread the output. The tool estimates whether you might qualify; it does not guarantee approval. Revenue officers sometimes calculate RCP more aggressively than the online tool, particularly when they identify asset equity the taxpayer did not fully disclose. Credit bureau data, Experian or TransUnion property records, and county assessor databases are all fair game during a review. Taxpayers who have taken on new debt to fund living expenses while owing the IRS should be especially careful here, because that debt may reduce their net asset calculation only modestly while their gross assets remain disqualifying.

OIC application fees ($205) and any required deposit (20% of a lump-sum offer, or the first month’s payment on a periodic offer) are non-refundable if the IRS rejects your submission. On a $50,000 proposed settlement, that non-refundable deposit alone equals $10,000, gone if rejected.

What the FY 2025 Acceptance Data Actually Shows

In FY 2025, taxpayers proposed 38,797 offers in compromise; the IRS accepted 5,464 of them, amounting to $98.1 million in settled debt. That is an acceptance rate of approximately 14.1%. The broader context matters: many of those 38,797 proposals came from taxpayers who used paid tax relief firms and were poorly matched to the program from the start. Tax professionals who screen carefully before submitting tend to see higher acceptance rates in their own practices, but the population-wide number is what it is, and it should be treated as a floor-level reality check, not a worst-case scenario.

What I see in practice: Most clients who come to me convinced they qualify for an OIC have home equity or retirement assets that disqualify them on paper. The RCP calculation almost always produces a higher number than they expect. I’d estimate that fewer than one in three of the taxpayers who walk in asking about an OIC are genuinely good candidates after we run the numbers.

Head-to-Head Comparison: Cost, Timeline, and Approval Odds

Side-by-Side on the Factors That Matter Most

| Factor | Long-Term Installment Agreement | Offer in Compromise |

|---|---|---|

| Setup Fee | $31–$225 (waived for low-income) | $205 application fee (non-refundable) |

| Deposit Required | None | 20% of offer or first monthly payment (non-refundable) |

| Approval Rate | Near-universal if returns are current | ~14% in FY 2025 |

| Processing Time | Immediate online; days to weeks by mail | 6–12 months typical; can exceed 18 months |

| Interest Accrual | Continues on unpaid balance throughout | Continues on original balance during review |

| Post-Acceptance Compliance | Keep payments current; no extended term | Must stay fully compliant for 5 years |

| Effect on Tax Lien | Lien released after full payment | Lien released within 30 days of final accepted payment |

A Worked Example: $40,000 in Back Taxes

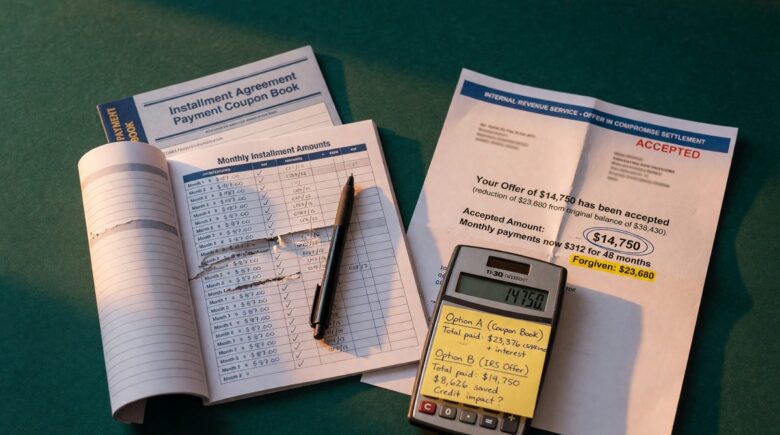

Consider a taxpayer who owes $40,000 in federal back taxes and can document that their RCP is $18,000. Under an OIC, they would submit an offer of $18,000 (plus a $3,600 non-refundable deposit if paying in a lump sum), for a total out-of-pocket cost of roughly $18,205 including the application fee, saving approximately $21,795 off the original balance before accounting for any additional interest that accrued during the 9-month review period (estimated at 8% annually: $40,000 x 8% x 9/12 = approximately $2,400 in new interest). Net savings are real but closer to $19,000 than $22,000 once that interest is factored in.

Under a 72-month installment agreement, the same taxpayer would pay roughly $556 per month on principal, plus interest compounding on the declining balance. Total repayment over 6 years at 8% annual interest on an amortizing schedule works out to approximately $50,300, about $10,300 more than the original balance. The OIC, if accepted, costs roughly $32,000 less over the same period. But, and this is the honest caveat, the OIC is only available if that taxpayer genuinely qualifies. If they don’t, they’ve spent $3,805 in non-refundable fees and deposits for nothing.

In FY 2025, the IRS accepted 5,464 Offers in Compromise worth $98.1 million, out of 38,797 total proposals submitted. That implies a rejection rate of nearly 86%.

Which Option Leaves You Better Off Long-Term

The long-term picture favors an OIC for taxpayers who genuinely qualify, but the comparison is narrower than it first appears. Both programs release the federal tax lien once the debt is resolved, though an accepted OIC typically results in lien release within 30 days of the final payment, while an installment agreement holds the lien in place for the full repayment term (up to 72 months or longer). That lien appears in public records and affects your FICO Score, your ability to refinance through lenders like Rocket Mortgage or Wells Fargo, and any real estate transaction during that period.

On cash flow over five to ten years, an accepted OIC clearly preserves more monthly liquidity once it is resolved. A taxpayer settling a $40,000 debt for $18,000 and completing payment in five months then has no further IRS obligation, freeing up funds that would otherwise go toward 72 monthly installments. The trade-off is the five-year post-acceptance compliance requirement: any lapse in filing or paying taxes during that period can void the settlement and reinstate the original amount owed, with only the payments already made credited back. Payment plans carry no such extended compliance obligation beyond keeping the current agreement current.

Applying Step by Step and What Happens If You’re Rejected

Forms, Fees, and Documentation

For a long-term installment agreement on a balance under $50,000, the application is entirely online through the IRS Online Payment Agreement portal, no forms, no financial disclosure, no waiting. Balances above $50,000 require Form 9465 (Installment Agreement Request) and, above $250,000, Form 433-A. The latter requires documentation of your income, expenses, assets, and liabilities, and the IRS treats it as a financial audit of sorts. Expect to gather pay stubs, bank statements, vehicle titles, mortgage statements, and retirement account balances, including any accounts held at brokers like Fidelity or Vanguard.

An OIC requires Form 656 (Offer in Compromise) and Form 433-A (OIC), a more detailed version of the standard collection information statement. The $205 application fee and required deposit must accompany the submission. Low-income applicants below 250% of the federal poverty level are exempt from both the fee and the deposit, an exemption worth knowing about if your income is modest. For context on current federal poverty guidelines, our coverage of how rising poverty guidelines affect eligibility can help you determine whether you fall within that threshold.

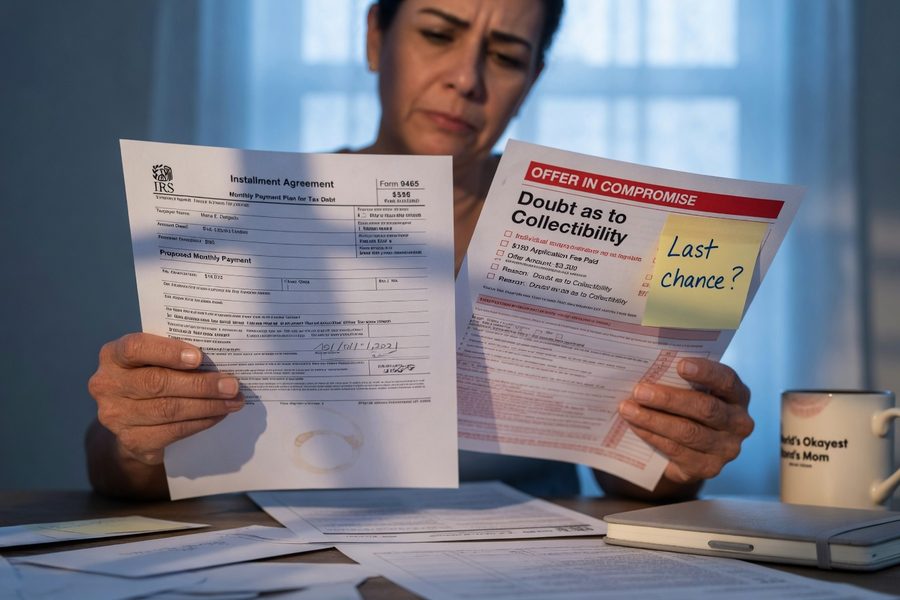

What Happens If the IRS Rejects Your OIC

Rejection is not final. Taxpayers have 30 days from the rejection letter date to file an appeal with the IRS Office of Appeals using Form 13711 (Request for Appeal of Offer in Compromise). Appeals add another several months to the process, and the outcome depends heavily on whether the rejection was based on a calculation dispute versus a fundamental collectibility issue. If the appeal fails, you have not lost the option to apply again; there is no statutory limit on resubmissions, though each new submission requires a new fee and deposit.

One detail most competing articles miss: if you had an active installment agreement before submitting your OIC, that agreement is suspended during the OIC review (you are not required to make installment payments while the OIC is pending). If the IRS rejects the offer, your installment agreement reinstates automatically with no new setup fee, provided no new tax debt has been added to your account. This is a meaningful safety net that reduces the downside risk of attempting an OIC when you are unsure of your odds.

If your OIC is rejected and your original installment agreement reinstates, immediately verify the reinstated balance with the IRS. Interest that accrued during the OIC review period will have been added to your balance, and the monthly payment may need to be recalculated to ensure you pay off within the original term.

Currently Not Collectible: The Overlooked Fallback

Currently Not Collectible (CNC) status is a formal IRS classification that pauses all collection activity when a taxpayer demonstrates they cannot pay basic living expenses and the tax debt simultaneously. It is not a forgiveness program. The debt remains, and interest keeps accruing, but CNC provides relief from levies, garnishments, and IRS contact while your financial situation is documented as dire. CNC status must be renewed periodically and can end if your income increases. For taxpayers who don’t qualify for an OIC and can’t manage even a minimum monthly payment, CNC is worth requesting through Form 433-F while longer-term options are explored.

When Neither Option Makes Sense

Two specific situations exist where both a payment plan and an OIC are suboptimal choices. First, if a significant portion of your balance is attributable to penalties rather than underlying tax, a penalty abatement request under First Time Abatement or Reasonable Cause can eliminate a material chunk of the debt without any fee, financial disclosure, or multi-year compliance obligation. A taxpayer with a clean prior compliance history who suddenly owes a large penalty for a single missed deposit or late payment is nearly always better served requesting penalty abatement before entering any formal agreement. First Time Abatement is automatic for eligible taxpayers and can be requested by phone.

Second, if your debt is approaching the end of its ten-year collection statute of limitations (the Collection Statute Expiration Date, or CSED), entering a payment plan or OIC can sometimes extend or toll that statute, a consequence that locks in IRS collection rights for longer than if you had simply waited. This is uncommon, but taxpayers whose debt is within two to three years of the CSED should have a CPA or enrolled agent review the statute dates before submitting any formal application. If you are dealing with multiple forms of debt simultaneously, our guide on how consumer debt affects lower-income households addresses the broader financial prioritization question.

Professional Help and Avoiding Tax Relief Scams

When You Actually Need Professional Help

A straightforward installment agreement on a balance under $50,000 with current filings and no enforcement action is well within the reach of a competent self-filer. The IRS’s online tools handle it end to end. Beyond that threshold, balances over $50,000, unfiled returns, active liens or levies, self-employment income with complicated asset calculations, or any OIC submission, professional help is worth the cost. An enrolled agent or CPA with tax resolution experience will calculate your RCP more accurately than most online tools, identify penalty abatement opportunities you would miss, and prevent procedural errors that trigger rejection.

Enrolled agents are federally licensed specifically to represent taxpayers before the IRS; CPAs and tax attorneys also carry representation rights. Fees vary widely, but a reputable professional handling an OIC submission typically charges $2,500 to $6,000 depending on complexity. That cost is real, but it is deductible as a miscellaneous expense and often recoverable in the form of a better settlement or avoided penalty. If cost is a barrier, the Taxpayer Advocate Service provides free representation in cases involving hardship, and Low Income Taxpayer Clinics (LITCs) serve taxpayers at or below 250% of the federal poverty level at no or nominal cost. You can also find free filing help through the resources covered in our article on free IRS tax help available in 2025.

Red Flags in the Tax Relief Industry

The tax settlement industry is one of the most complaint-heavy segments of consumer financial services. The FTC has taken action against numerous firms for deceptive advertising, charging upfront fees of $3,000 to $10,000 while delivering nothing, and misrepresenting acceptance odds. The CFPB has flagged similar patterns in adjacent debt relief markets, and the same warning signs apply here. Specific red flags include any firm that guarantees OIC approval before reviewing your financials, any firm that asks for payment before completing your case, and any firm that tells you to stop communicating with the IRS without explaining what that means legally.

| Red Flag | What It Actually Means |

|---|---|

| “Guaranteed OIC approval” | No firm can guarantee IRS acceptance; this is a deceptive claim |

| Large upfront fee before review | Legitimate firms assess your finances before quoting a fee |

| “Settle for pennies on the dollar” | Describes the OIC program generically; 86% rejection rate is omitted |

| “Stop all IRS contact immediately” | Without formal representation, ignoring IRS notices worsens enforcement |

| Unlicensed representatives | Only enrolled agents, CPAs, and attorneys may legally represent you before the IRS |

If you are weighing professional help, the top credit counseling services guide on this site covers how to vet financial professionals broadly, and many of the same vetting principles apply to tax resolution firms. For taxpayers navigating stretched household budgets while resolving tax debt, reviewing options like LIHEAP utility assistance can free up monthly cash that makes an installment payment more sustainable.

The IRS offers a free Pre-Qualifier Tool at irs.treasury.gov that estimates whether you may qualify for an Offer in Compromise before you pay a single dollar in fees. Running this tool takes about 10 minutes and can save you $205 in non-refundable application fees if you clearly don’t meet the criteria.

The Compliance Foundation That Underlies Everything

Whatever resolution path you choose, no agreement, payment plan or OIC, survives a compliance failure during its term. Filing every required return on time, paying any new taxes owed as they come due, and making required installment or OIC payments without interruption are the baseline requirements. For OIC recipients, this obligation runs five full years after acceptance. One missed estimated tax payment for the current year can default a multi-year installment agreement. This is not a small caveat; it is the central operating requirement of both programs, and it is the part most taxpayers underestimate when they are relieved to have gotten an agreement in place.

The IRS’s Taxpayer Advocate Service, an independent office within the IRS, can intervene on your behalf if you are experiencing significant hardship and normal IRS channels have been unresponsive. The National Taxpayer Advocate submits an annual report to Congress documenting systemic problems, and individual case advocacy is free.

| Scenario | Best Option | Why |

|---|---|---|

| Owe under $50K, can pay in 72 months | Streamlined Installment Agreement | No disclosure, near-certain approval, no deposit |

| Low income, minimal assets, high debt | OIC (Doubt as to Collectibility) | RCP likely below balance; genuine settlement candidate |

| High home equity, cash-flow tight | Installment Agreement or CNC | Asset equity likely exceeds balance; OIC will be rejected |

| Penalties are bulk of balance | Penalty Abatement Request First | Can eliminate large portion at no cost before any agreement |

| Debt near CSED expiration | Consult professional before any application | Both programs can toll the statute; wrong move extends IRS rights |

| Cannot pay anything, true hardship | Currently Not Collectible | Pauses enforcement while situation stabilizes |

Before submitting any IRS resolution application, pull your IRS account transcript at IRS.gov. Your transcript shows every assessment date, every penalty charge, every payment made, and the Collection Statute Expiration Date for each tax period. Knowing these dates before you file anything prevents costly missteps.

Real-World Example: Two Paths on a $55,000 Tax Debt

Consider an illustrative example: a self-employed graphic designer, 41 years old, with $55,000 in federal tax debt spanning three years of underreported income. She has a car worth $12,000 (with $8,000 still owed), no real estate, $6,000 in a savings account, and a net monthly disposable income, after IRS-allowed living expenses, of $400. Her calculated RCP using a lump-sum OIC formula would be: (80% of net asset value) + (12 x monthly disposable income) = [(80% x $20,000 net assets)] + [12 x $400] = $16,000 + $4,800 = $20,800. Since $20,800 is well below her $55,000 balance, she is a legitimate OIC candidate.

Path A: She submits an OIC for $20,800. She pays the $205 application fee and a $4,160 deposit (20% of the lump-sum offer). Nine months later, the IRS accepts the offer. Total paid: $20,800. She must now stay fully compliant for five years, file every return on time, pay every quarterly estimated tax. Over the review period, approximately $3,300 in new interest accrued on the original $55,000 balance, but that is absorbed into the settled amount. Total savings versus full repayment: roughly $34,200 plus interest that would have built on the remaining balance.

Path B: She applies for a 72-month installment agreement under the standard online program. Minimum monthly payment: $55,000 ÷ 72 = approximately $764 per month. On a $400 monthly disposable income, she cannot sustain this payment. She would need to request a lower payment based on hardship, which triggers a full financial disclosure and may result in the IRS pushing for a higher payment than she proposes. Even at $600 per month (a negotiated rate), total payments over 72 months plus interest on the declining balance come to approximately $68,000, $13,000 more than the original debt.

In this scenario, the OIC clearly wins on total cost. The risk is the five-year compliance obligation. If this designer has a history of falling behind on quarterly estimated taxes, which is what generated the debt in the first place, the OIC’s post-acceptance requirement is a genuine threat. A smart adviser in this case would build a quarterly estimated tax system before submitting the offer, not after, so the compliance infrastructure is already in place when the IRS accepts.

Your Action Plan

-

Pull Your IRS Account Transcript

Log into your IRS online account at IRS.gov and download transcripts for every tax year with a balance. Record the assessment date and Collection Statute Expiration Date (CSED) for each. These dates govern which programs you can use and whether entering any formal agreement is in your interest. If you cannot access your online account, call the IRS at 800-829-1040 and request transcripts by mail.

-

File All Missing Returns Immediately

Neither an installment agreement nor an OIC will be processed while you have unfiled returns. If cost is a barrier to getting returns prepared, the IRS Volunteer Income Tax Assistance (VITA) program provides free preparation for taxpayers earning under $67,000, and Low Income Taxpayer Clinics offer representation. Do not delay resolution strategy while returns remain unfiled; the interest meter runs regardless.

-

Run the IRS OIC Pre-Qualifier Tool

Before paying any professional or submitting any application, spend 10 minutes on the IRS’s free Pre-Qualifier Tool at irs.treasury.gov. Enter your income, assets, and expenses honestly. If the tool says you likely do not qualify, take that seriously; it is a first-pass version of the same RCP calculation the IRS uses. If it says you may qualify, that is a signal to consult a professional for a more precise RCP calculation before committing to the $205 application fee and non-refundable deposit.

-

Check for Penalty Abatement Before Committing to Any Program

Call the IRS and ask whether your account qualifies for First Time Abatement. This requires no application form and is granted automatically if you have three prior years of clean filing and payment compliance. If your balance includes a large penalty component, abatement can reduce what you actually owe before any payment plan or OIC calculation is done, potentially enough to push you into a simpler, lower-cost resolution tier.

-

Apply for the Appropriate Plan Based on Your RCP and Cash Flow

If your RCP is below your balance and you have the liquidity for the deposit, engage a credentialed professional to prepare and submit your OIC. If your RCP equals or exceeds your balance, apply for the highest-tier installment agreement you can sustain without default: the streamlined program under $50,000, or a negotiated agreement using Form 433-A above that threshold. Set up direct debit for every installment agreement; the 0.25% (vs. 0.5%) monthly penalty rate for direct-debit agreements compounds to meaningful savings over 72 months.

-

Build a Compliance System Before Your Agreement Takes Effect

The most common reason OICs are voided and installment agreements default is the same tax debt problem recurring: current-year returns are filed late or current-year taxes go unpaid. Set up automatic estimated tax payments through IRS Direct Pay or EFTPS for the current year. Calendar your filing deadline at least 30 days in advance. If your income is variable, freelance, self-employment, gig work, estimate conservatively and pay a buffer. One missed quarterly payment can unravel an agreement you spent months building.

Frequently Asked Questions

What is the minimum monthly payment on an IRS installment agreement?

For agreements on balances under $50,000, the IRS sets the minimum at 1/72 of your total balance, so a $36,000 debt would have a minimum payment of $500 per month. For balances between $50,001 and $250,000, the same 84-month formula applies (balance divided by 84). For balances above $250,000, there is no formula minimum; the IRS negotiates a payment based on your Collection Information Statement, Form 433-A.

Note that these minimums assume no additional penalties or interest adjustments. Your actual monthly cost will be slightly higher as the IRS adds accrued interest to the balance at each payment cycle. Using direct debit reduces the ongoing failure-to-pay penalty rate from 0.5% to 0.25% per month, which makes a measurable difference over a long agreement term.

Does applying for an Offer in Compromise hurt my credit score?

The OIC application itself does not generate a credit inquiry or directly affect your FICO Score. However, the federal tax lien that the IRS may have already filed, which is what typically shows up in public records and damages credit, remains in place throughout the OIC review and is released within 30 days after you make the final payment on an accepted offer. Credit reporting agencies including Experian, Equifax, and TransUnion may reflect the lien removal within one to two reporting cycles after release. So the credit impact of an OIC is largely determined by whether a lien was filed before you applied, not by the OIC process itself.

Can I switch from an installment agreement to an Offer in Compromise?

Yes. Submitting an OIC does not require you to cancel your existing installment agreement first. Keeping the installment agreement in place while you submit an OIC is often the right move: you are not required to continue making installment payments while the OIC is under review, and the agreement reinstates automatically with no new fee if the IRS rejects your offer. If the OIC is accepted, the installment agreement is terminated and superseded by the offer terms.

How long does the IRS typically take to review an OIC?

Published IRS guidance cites a processing time of roughly 6 to 12 months for most OIC submissions, though complex cases or those that go through the appeals process can take 18 months or longer. During that entire period, collection activity (levies, garnishments) is suspended, but interest and penalties continue accruing on your original balance. The accrued interest is not forgiven as part of the OIC; it is absorbed into the negotiated settlement if the offer covers it.

Is there a minimum debt amount required to apply for an OIC?

No. There is no floor on how much you must owe to submit an OIC. The practical economics of the program make it questionable for small balances. The $205 non-refundable application fee, the required 20% deposit on a lump-sum offer, and the cost of professional help to prepare the submission can easily exceed the savings on a $5,000 to $10,000 debt. A payment plan, or even a short-term plan at no user fee, is almost always the more cost-effective choice for smaller balances.

What happens to penalties and interest if my OIC is accepted?

An accepted OIC settles your entire tax liability, the underlying tax, all penalties, and all interest, for the agreed amount. The IRS does not separately preserve the right to collect penalties or interest once the offer is accepted and paid in full. This is one of the genuine financial advantages of an OIC over a payment plan: the settlement extinguishes the complete liability rather than simply spreading out the full amount over time.

What does “Currently Not Collectible” status do to my tax debt?

Currently Not Collectible status pauses all IRS collection enforcement, levies, liens, garnishments, and collection notices, while you are classified in hardship. The debt itself does not go away, and interest continues to accrue. CNC status is reviewed periodically (typically every year or two) through an updated financial statement. It is best understood as temporary breathing room rather than a resolution, but for taxpayers in genuine crisis, it can provide time to stabilize income or prepare for a formal resolution like an OIC or installment agreement.

Sources

- Internal Revenue Service, Offer in Compromise

- Internal Revenue Service, IRS Payment Plan Options: Fast, Easy, and Secure

- Internal Revenue Service, Tax Topic 204: Offers in Compromise

- Taxpayer Advocate Service, Offer in Compromise

- Internal Revenue Service, An Offer in Compromise Can Help Certain Taxpayers Resolve Tax Debt

- Internal Revenue Service, Collections Activities, Penalties, and Appeals Statistics (FY 2025)

- Internal Revenue Service, SOI Tax Stats: What’s New (FY 2024 Installment Agreement Data)

- Internal Revenue Service, Online Payment Agreement Application

- Taxpayer Advocate Service, Low Income Taxpayer Clinics (LITC)

- Internal Revenue Service, Form 656 Booklet: Offer in Compromise Instructions and Forms