Fact-checked by the MyFinancial101 editorial team

Quick Answer

Missing the tax deadline triggers two separate IRS penalties: a failure-to-file penalty of 5% per month (up to 25%) and a failure-to-pay penalty of 0.5% per month (up to 25%). For returns due after December 31, 2025, the minimum penalty if more than 60 days late is $525. Filing immediately, even without full payment, stops the larger penalty from growing.

A missed tax deadline penalty doesn’t arrive as a single surprise bill. The Internal Revenue Service charges two distinct penalties simultaneously: the failure-to-file penalty, set at 5% of unpaid taxes per month, and the failure-to-pay penalty at 0.5% per month, both accruing from the day after the deadline until you resolve the balance. For the 2025 tax year (with an April 15, 2026 deadline), those rates apply to any unfiled, unpaid return right now.

The good news: the damage is heavily front-loaded. Most of the penalty cost accumulates in the first two to three months, which means acting quickly has a disproportionate impact. This guide covers exactly how penalties stack, what interest adds on top, which payment options the IRS offers when you can’t pay in full, and how to request relief if you have a clean compliance history.

Key Takeaways

- The failure-to-file penalty is 5% per month, capped at 25% of unpaid taxes, ten times the failure-to-pay rate, making filing quickly the single most impactful action you can take (IRS).

- For returns due after December 31, 2025, the minimum failure-to-file penalty for returns more than 60 days late is $525, even if the actual tax owed is smaller (IRS, 2026).

- The IRS assessed $29.6 billion in additional taxes in FY 2025 on returns that were not filed on time, a figure that reflects how broadly this problem affects taxpayers (IRS Statistics, 2025).

- When both penalties apply in the same month, the combined rate is capped at 5% total, the failure-to-file rate drops to 4.5% so the two don’t exceed 5% together (IRS).

- More than 20 million taxpayers filed by the October 15 extended deadline in 2025, confirming that extensions are common and do not trigger the failure-to-file penalty on their own (IRS, 2025).

In This Guide

What Happens Right After You Miss the Deadline

Most people expect an immediate notice from the IRS. That’s not how it works. The agency processes more than 271 million federal tax returns and supplemental documents per year, so a CP-series notice typically arrives four to eight weeks after the filing deadline, not the next morning. The penalties, however, start accruing the day after the deadline regardless of when you hear from them.

Refund Expected vs. Balance Due: Two Very Different Situations

If you’re owed a refund, there’s no failure-to-file or failure-to-pay penalty, the IRS won’t charge you for filing late when no money is due. The real risk in that case is forfeiting the refund entirely: unclaimed refunds are generally subject to a three-year window, after which the money reverts to the U.S. Treasury. If you owe taxes, though, the clock started ticking on April 16th. The distinction matters because millions of people delay filing out of anxiety when they actually have nothing to lose.

The 60-day mark is the most important threshold to know. Filing within 60 days of the deadline keeps you in the standard penalty structure. Cross that line and you hit either the 5-month maximum penalty or the flat $525 minimum, whichever is greater, with no further benefit from the graduated monthly rate. If your tax bill is small (say, $200), the minimum penalty will actually exceed your entire tax liability.

The IRS collected $3.5 billion in FY 2025 specifically from delinquent returns, separate from the $29.6 billion in additional taxes assessed on late filers. That gap shows how much of the cost falls on the taxpayer before enforcement even escalates.

The Two Main Penalties, Explained

Two separate penalty clocks run at the same time, and confusing them is one of the most common mistakes late filers make. The failure-to-file (FTF) penalty and the failure-to-pay (FTP) penalty are independent charges, but they interact in a specific way that limits total monthly damage.

How the Rates Stack (and Where They’re Capped)

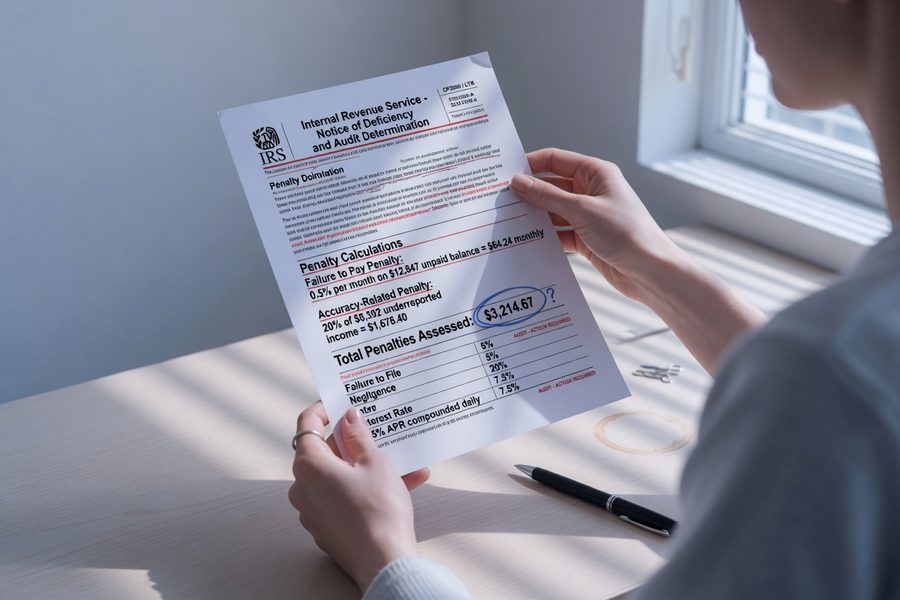

According to the IRS failure-to-file penalty guidance, the FTF rate is 5% of unpaid taxes per month or partial month, up to a maximum of 25%. The failure-to-pay penalty runs at 0.5% per month, also capped at 25%. When both apply in the same month, the combined rate is capped at 5%, so the FTF rate effectively drops to 4.5% to accommodate the FTP rate alongside it. This matters because many penalty calculators online get this wrong and overstate the total.

Here’s what that looks like month by month on a $3,000 balance due:

| Month Late | FTF Penalty (4.5%/mo) | FTP Penalty (0.5%/mo) | Combined Monthly Charge | Running Penalty Total |

|---|---|---|---|---|

| Month 1 | $135.00 | $15.00 | $150.00 | $150.00 |

| Month 2 | $135.00 | $15.00 | $150.00 | $300.00 |

| Month 3 | $135.00 | $15.00 | $150.00 | $450.00 |

| Month 4 | $135.00 | $15.00 | $150.00 | $600.00 |

| Month 5 | $135.00 | $15.00 | $150.00 | $750.00 |

| After Month 5 (FTF maxed) | $0.00 | $15.00 | $15.00 | Continues +$15/mo |

Note: This illustration uses the capped combined rate. Actual monthly charges are computed on the remaining unpaid balance, which decreases as payments are made. Interest accrues separately and is not shown here.

Fraud Penalties Are a Different Category

If the IRS determines a late filing was fraudulent rather than negligent, the failure-to-file penalty jumps to 15% per month, with a maximum of 75% of unpaid tax. This is rare for individual filers, ordinary late filing, even if years overdue, doesn’t meet the fraud threshold. The standard 5% rate applies to the vast majority of people who simply missed the deadline.

How Interest Compounds, and Why It Often Beats the Penalties Long-Term

Penalties get the attention, but interest is quietly the more expensive problem for anyone who waits months or years to resolve a balance. The IRS calculates interest daily on unpaid taxes, and unlike penalties, it has no statutory cap.

The Real Cost at 30 Days vs. 90 Days

The IRS sets its interest rate at the federal short-term rate plus 3 percentage points, adjusted quarterly. For 2026, that has been running at approximately 7% annually (roughly 0.019% per day). On a $3,000 balance, 30 days of interest adds about $17. That sounds modest, but by 90 days, you’ve also added roughly $51 in interest on top of $450 in penalties, for a combined additional cost of approximately $501 above your original liability. Wait a full year without resolving anything and the FTF penalty alone hits its 25% maximum ($750), the FTP penalty reaches 6% ($180), and interest adds roughly $210, a total surcharge approaching $1,140 on that same $3,000 bill. That’s nearly 38% on top of what you originally owed.

The critical takeaway: file now even if you can’t pay. As the IRS explicitly states, taxpayers who missed the April deadline should file as soon as possible to limit interest and penalties, even if they cannot pay the full amount immediately. Filing stops the 5% monthly FTF clock. Not filing keeps it running.

The IRS collected $117.5 billion in FY 2025 from unpaid assessments on returns filed with additional tax due, a figure that includes penalties and interest on top of the underlying tax liability. (IRS Collections Data, 2025)

Should You File Now or Request an Extension?

If the April deadline has already passed, an extension is no longer available for the current tax year, that ship has sailed. Extensions (Form 4868) must be filed on or before the original due date. If you’re reading this after April 15, 2026, the only path forward is to file the late return as soon as possible.

What an Extension Actually Covers

A common misconception: an extension gives you more time to file, not more time to pay. If you owed taxes on April 15th and filed an extension, any unpaid balance still began accruing the failure-to-pay penalty immediately. Extensions protect you from the larger FTF penalty only, and only if you filed the extension on time. More than 20 million taxpayers used the October 15 extended deadline in 2025, but each of them still owed any unpaid balance from April onward.

For taxpayers who expect to need extra time in future years, the lesson is straightforward: file the extension and pay an estimate of what you owe by April. That combination eliminates both penalties for the extension period. If you’re uncertain how to estimate that payment, our guide on preparing for tax season covers estimated payment calculations in detail.

If you can’t pay anything right now, file a $0-payment return anyway. Filing without payment stops the failure-to-file penalty immediately and leaves only the smaller failure-to-pay penalty (0.5% per month) running. That single action cuts your monthly penalty rate by 90%.

Payment Options When You Can’t Pay the Full Amount

Not being able to pay in full is not a reason to delay filing. The IRS offers structured payment options for almost every situation, and most can be set up online within 30 minutes.

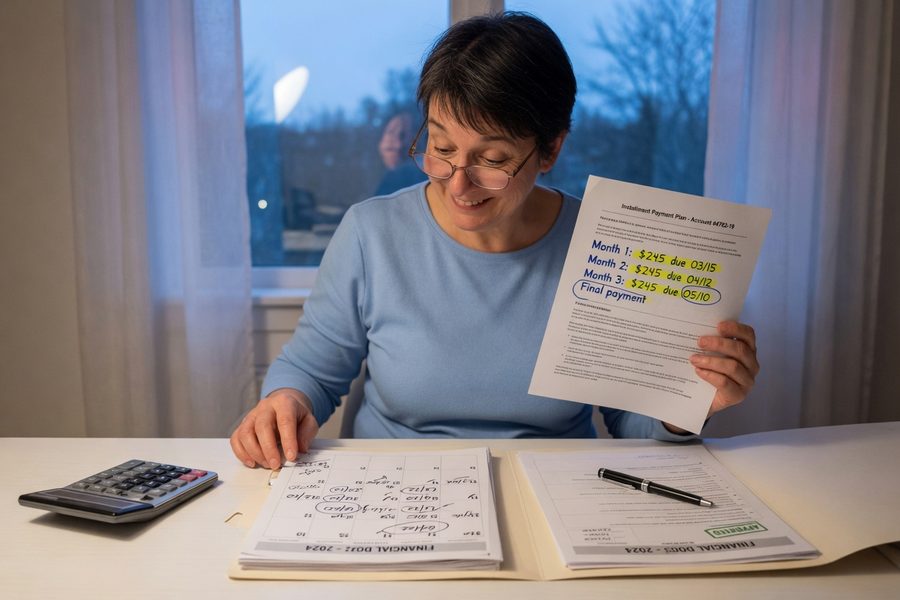

Short-Term Plans, Installment Agreements, and Offers in Compromise

A short-term payment plan (up to 180 days) is available to individuals who owe less than $100,000 in combined tax, penalties, and interest. There’s no setup fee for online enrollment. A long-term installment agreement works for larger balances or those who need more time; setup fees range from $31 to $225 depending on how you apply and your income level, though low-income taxpayers may qualify for a waiver. Both options allow partial payments while the balance accrues the standard 0.5% FTP penalty and daily interest, meaning you’re not stopping the meter entirely, but you are preventing enforcement escalation like liens or levies.

An Offer in Compromise (OIC) is a separate program that lets qualifying taxpayers settle for less than the full amount owed. The IRS acceptance rate for OICs is historically low (around 30-40%), and the application requires detailed financial disclosure. It’s a legitimate option for taxpayers in genuine financial hardship, not a shortcut for anyone who simply prefers to pay less. If you’re carrying other high-interest debts alongside your tax bill, it may help to review strategies for prioritizing and negotiating debt obligations before deciding which to address first. Similarly, if tight cash flow is the core issue, looking at jobs currently paying $19 or more per hour or exploring micro-freelancing income options can help generate the cash to resolve a balance faster.

How to Request Penalty Relief

First-time abatement (FTA) is the fastest and most commonly granted form of IRS penalty relief, and most people who qualify never ask for it. The eligibility rule is simple: no penalties on your tax account for the prior three years, and you must be current on all filing requirements.

How to Request FTA and What Qualifies as Reasonable Cause

FTA applies to the failure-to-file and failure-to-pay penalties. You can request it by calling the IRS directly at 1-800-829-1040, by writing a letter to the address on your notice, or, for certain account types, through the IRS online account portal. Phone requests are often resolved in a single call if the account history is clean. When calling, clearly state: “I am requesting first-time abatement under IRS Policy Statement 20-1 for the [tax year] failure-to-file/failure-to-pay penalty. I had no penalties for the three prior tax years.”

If FTA doesn’t apply, say, you had a penalty in 2024, reasonable cause is the alternative. The IRS accepts documented circumstances like serious illness, natural disaster, or the unavoidable absence of records. Vague explanations (“I forgot,” “I was busy”) don’t meet the standard. Specific documentation does: a hospital discharge summary, a FEMA declaration number, or a written statement from a professional who confirms they provided you with incorrect advice. The IRS requires that the cause was beyond your control and that you acted reasonably once the obstacle was removed. For a broader picture of how tax help and credits work for lower-income filers, see our overview of free IRS tax help and commonly missed credits.

One honest limitation of penalty relief: it eliminates penalties, not interest. Even a fully approved FTA request leaves the daily interest charges in place. That’s not a reason to skip the request, eliminating 25% in penalties is still significant, but it’s a detail many taxpayers don’t realize until after approval.

Frequently Asked Questions

What is the missed tax deadline penalty if I owe nothing?

No penalty applies if you’re owed a refund and file late. Both the failure-to-file and failure-to-pay penalties are calculated on taxes owed, a zero-balance return generates neither. The only risk is forfeiting your refund if you wait more than three years past the original due date.

Can the IRS file a tax return on my behalf if I never file?

Yes. The IRS can prepare a Substitute for Return (SFR) using information from W-2s, 1099s, and other third-party data. SFRs use the most unfavorable filing status (typically single) and claim no deductions beyond the standard deduction. The resulting tax bill is almost always higher than what you would have owed on a self-prepared return, which is one more reason to file your own return promptly.

Does filing late hurt your credit score?

Filing a late return does not directly affect your credit score. Tax penalties and interest are not reported to credit bureaus. However, if the IRS files a federal tax lien against your property after escalated collection action, that lien can become a matter of public record and affect your ability to secure financing. The lien risk only arises after extended non-payment, not from a single late filing.

Is there a penalty if I filed an extension but still missed October 15?

Yes. If you filed a valid Form 4868 extension by April 15, 2026, your deadline moved to October 15, 2026. Missing that extended deadline triggers the standard failure-to-file penalty from October 16 onward, the extension only shifted the clock, it didn’t eliminate the penalty for filing after the new date. Any taxes owed from April 15 onward still accrued the failure-to-pay penalty throughout.

What if I owe state taxes in addition to federal?

State tax deadlines and penalty structures vary significantly. Most states follow the federal April 15 deadline, but penalty rates differ, some states charge as little as 1% per month while others match or exceed the federal 5% rate. In general, prioritize filing both returns promptly over trying to pick one. State revenue agencies can independently pursue liens, wage garnishment, and refund offsets, so a federal payment plan doesn’t pause state collection activity. Check your state’s department of revenue website for exact rates and relief programs, as federal first-time abatement has no state equivalent in most jurisdictions.

Sources

- Internal Revenue Service, Failure to File Penalty

- Internal Revenue Service, Failure to Pay Penalty

- Internal Revenue Service, Taxpayers Who Missed the April Tax Filing Deadline Should File as Soon as Possible

- Internal Revenue Service, Filing Past Due Tax Returns

- Internal Revenue Service, Collections Activities, Penalties, and Appeals (FY 2025)

- Internal Revenue Service, IRS Reminds Taxpayers Who Filed for Extensions of the Oct. 15 Deadline