Fact-checked by the MyFinancial101 editorial team

Quick Answer

Effective money management for freelancers with irregular income starts with calculating your lowest reliable monthly income over the past 6-12 months, then using that figure as your spending ceiling. Keep a minimum 6-month emergency buffer (9-12 months for high-seasonality work), set aside 25-35% of every payment for taxes, and pay yourself a fixed monthly “salary” from a dedicated business account to smooth cash flow.

Money management for freelancers with irregular income is genuinely different from budgeting on a salary, and treating it the same way is where most self-employed workers run into trouble. According to research from the National Bureau of Economic Research (2025), self-employed individuals at age 55 earn an estimated average of $134,000 annually compared to $79,000 for similarly positioned employees, but with far greater income fluctuations quarter to quarter. Higher earning potential and higher cash-flow risk come as a pair.

If you have ever ended a strong month with a false sense of security, then stared at a thin client roster six weeks later wondering how to cover rent, this guide is for you. Below, you will find a practical framework covering baseline income calculations, account structure, tax reserves, buffer-building mechanics, and spending rules that hold up when revenue swings by 40% or more.

Key Takeaways

- Self-employed workers at age 55 earn an estimated average of $134,000 per year, compared to $79,000 for comparable employees, but face substantially greater income volatility (National Bureau of Economic Research, 2025).

- Only 55% of U.S. adults had set aside enough for three months of expenses in 2024, a threshold most freelancers need to more than double (Federal Reserve Board, 2024).

- Freelancers should reserve 25-35% of every payment for federal income tax and self-employment tax from day one, before spending a single dollar.

- The IRS recommends that self-employed individuals maintain separate business and personal bank accounts for accurate recordkeeping and tax compliance (IRS Publication 334).

- Using the lowest reliable monthly income from the past 6-12 months as a budget ceiling creates automatic surplus in above-average months without requiring willpower.

In This Guide

Why Irregular Income Feels Like a Constant Emergency

The anxiety is not irrational. It is a predictable response to an unpredictable cash cycle, and the first step to managing it is understanding the structure of the problem rather than blaming your own financial discipline.

Most freelancers mentally benchmark their finances against their best months. A strong October, three invoices paid, a new retainer signed, sets an expectation that November will look similar. When it does not, the gap between expectation and reality triggers a stress response that economists call “reference point loss aversion.” The actual income may still cover expenses comfortably, but the comparison to peak months makes it feel like a shortfall. This is why the psychological work of money management for freelancers with irregular income starts with reframing volatility as the baseline condition, not a deviation from it.

The Decision Fatigue Problem During Slow Months

Multi-month slow periods create a specific kind of decision fatigue that generic financial advice glosses over. When revenue drops for eight consecutive weeks, every purchase becomes a negotiation: is this necessary right now, or should I hold cash? That constant low-grade stress depletes the cognitive energy you need for client work, which can make the slow period worse. The fix is a pre-committed spending framework built during good months, so that the decisions are already made when revenue dips. Concrete rules outperform willpower every time.

Those still building a client roster can meaningfully smooth this stress by adding a steady income stream. Exploring steady-paying hourly roles available in 2026 can serve as a bridge during lean patches without compromising long-term freelance growth.

Only 55% of U.S. adults had saved enough to cover three months of expenses in 2024, according to the Federal Reserve’s 2024 household survey. For freelancers, the recommended threshold is at least twice that, six months, and up to twelve for those with seasonal revenue patterns.

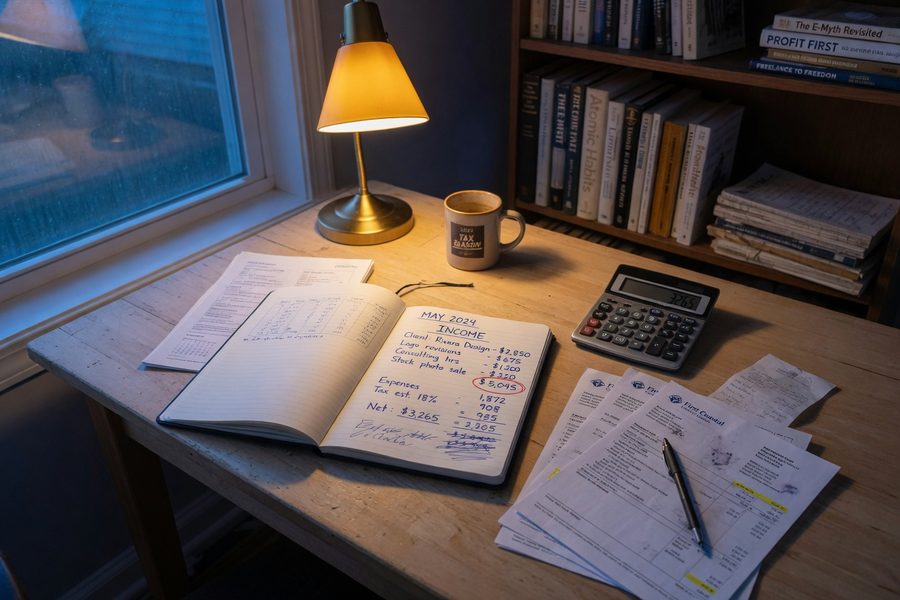

Calculating Your Realistic Baseline Income

Your budget should be built on your lowest reliable month, not your average. This single shift changes everything downstream.

Pull your actual deposits for the past 6-12 months. Remove any one-time windfalls, a large project you landed once, a referral bonus, a retainer that ended, and identify the floor: the worst ordinary month you had. That number is your baseline. Budget as though every month pays that amount. In stronger months, the surplus accumulates automatically without requiring any active decision-making.

A Worked Example

Suppose your last twelve months of freelance deposits look like this: your lowest ordinary month was $3,200 and your monthly average was $5,100. Using $3,200 as your ceiling means that in an average month you generate $1,900 in surplus. Over twelve months at the average rate, that is $22,800 in surplus, money that flows into your buffer, tax reserve, and retirement accounts without any conscious transfer decision. If you had budgeted to the average instead, a month at $3,200 would leave you $1,900 short, forcing debt or dipping into savings. The baseline approach converts volatility from a threat into a structural advantage.

One honest caveat: this method requires enough monthly income to actually cover essential expenses at the floor level. If your lowest months genuinely do not cover rent, utilities, and food, the baseline approach will not close that gap on its own. In that case, the priority shifts to either raising the floor through additional income or cutting fixed expenses before any of the buffer-building strategies below become workable.

Separating Business and Personal Money

Every invoice should land in a business checking account first. Personal money never touches it until you transfer your predetermined monthly “salary.”

The IRS explicitly recommends in Publication 334 that self-employed individuals maintain separate business and personal bank accounts for accurate recordkeeping and tax compliance. Beyond the tax argument, separation creates a psychological firewall: your personal lifestyle is funded by fixed monthly transfers, not by however much happened to arrive that week. This is the mechanism that converts irregular deposits into predictable household income.

The Three-Account Structure

A simple setup that works for most sole proprietors requires three accounts: a business checking account where all client payments are received; a tax reserve savings account, funded immediately upon each deposit; and a personal checking account that receives a single fixed transfer each month. LLC owners may add a fourth account for retained business earnings, but sole proprietors rarely need more complexity than these three. Automate the tax transfer and personal salary transfer so they execute on a schedule, handling compliance and personal cash flow before you can spend the money on anything else.

For anyone managing existing credit card debt alongside freelance income, keeping business and personal accounts strictly separated also prevents the common mistake of using business revenue to pay personal debt impulsively during flush months, which distorts both your tax records and your true baseline calculation.

Set your monthly personal salary transfer to occur on the 1st and 15th, two equal halves of your baseline income, rather than one lump sum. This mirrors a biweekly paycheck rhythm, which makes personal budgeting more intuitive and reduces the temptation to treat the whole month’s transfer as immediately available.

Building Buffers That Actually Smooth Cash Flow

A six-month emergency fund is the minimum for freelancers. For anyone with seasonal revenue patterns or clients who pay on 60-day net terms, nine to twelve months is a more defensible target.

The standard advice to W-2 employees is three to six months of expenses. Freelancers need more because revenue can swing 40% or more quarter to quarter, and client payment delays can stack on top of a naturally slow season. A single client paying two weeks late during a slow month can create a genuine cash-flow crisis if your buffer is too thin, even if your annual income is healthy.

Income-Smoothing Mechanics

Beyond the emergency fund, an income-smoothing account is a separate high-yield savings account that serves a different purpose: it holds surplus from strong months and is drawn down in weak ones to maintain your fixed personal salary. The mechanics work like a reservoir. In a month where revenue exceeds your baseline by $2,000, that $2,000 goes into the smoothing account rather than lifestyle spending. In a month where revenue is $1,500 below baseline, you draw $1,500 from the smoothing account. Your personal checking account receives the same transfer every month regardless. The goal is stability, not growth, though holding these funds in a high-yield savings account means they earn meaningful interest while waiting.

Building a buffer of nine or more months of expenses takes time, often two to three years for someone early in their freelance career. During that accumulation phase, the system is more fragile than it eventually becomes, and a prolonged slow period before the buffer is fully funded can still cause real financial strain. That is worth stating plainly. The framework described here is sound, but it offers its full protection only once the buffer is in place.

Those who want to retire early or build wealth beyond the buffer should direct surplus funds into retirement vehicles. A SEP IRA allows contributions of up to 25% of net self-employment income (with a 2025 cap of $70,000), while a Solo 401(k) allows both employee and employer contributions, making it more powerful for higher earners. The timing rule that matters: base contributions on your conservative baseline income projection for the year, not on a windfall quarter. Adjusting upward at year-end is straightforward; overcommitting and needing to reverse contributions is not. For a deeper look at building long-term wealth as a freelancer, this guide to starting investing with no prior experience covers the foundational principles that apply regardless of income structure.

Self-employed individuals at age 55 earn an estimated average of $134,000 annually, compared to $79,000 for comparable employees, a $55,000 premium, but with substantially higher income volatility, according to the National Bureau of Economic Research (2025). That premium only translates to real wealth if cash-flow management preserves it through lean periods.

Spending and Budgeting Rules That Survive Income Swings

Budget every personal expense against your baseline income, not your average, not last month’s total. Every dollar above baseline is surplus until it hits one of three designated buckets: buffer, tax reserve, or retirement.

The Zero-Sum Budget Approach

A zero-sum budget assigns every dollar of your baseline income a job before the month begins: fixed costs first (rent, utilities, insurance, minimum debt payments), then variable necessities (groceries, transport), then discretionary categories capped at specific amounts. The math must reach zero, meaning all income is allocated, with surplus directed explicitly to savings categories rather than left unassigned. Left unassigned, it disappears. The discipline of this approach is that surplus months do not automatically authorize lifestyle upgrades; they fund the buffer and retirement accounts instead.

Containing Lifestyle Creep in Strong Months

Lifestyle creep is the most reliable way for high-earning freelancers to end up financially fragile. After a run of strong months, fixed costs rise, a nicer apartment, a car payment, a second streaming subscription, and the new floor becomes unsustainable when revenue normalizes. The rule that prevents this: no increase in recurring fixed expenses unless your buffer is fully funded and the new expense is covered by your baseline, not by recent good months. Discretionary spending during flush months is fine; converting discretionary spending into new fixed obligations is the problem.

Keeping variable grocery and household costs lean is a discipline that pays off year-round, not just during slow periods. Resources like strategies used by coupon stackers to beat inflation apply directly to a freelancer’s variable spending categories.

Taxes: The Non-Negotiable Reserve

Set aside 25-35% of every payment the moment it clears your business account. For most freelancers, federal income tax plus the IRS self-employment tax (currently 15.3% on net earnings, covering Social Security and Medicare) will land in the 30-32% range for moderate earners; higher-income freelancers should lean toward 35% to avoid underpayment penalties. Pay quarterly estimated taxes by the IRS deadlines, April 15, June 16, September 15, and January 15, and keep the reserved funds in a dedicated savings account so they are never accidentally spent. Underpayment penalties are small relative to the tax bill itself, but the April surprise of a large balance due is both financially and psychologically damaging. For freelancers working through the full complexity of estimated taxes and deductible expenses, this overview of what to prepare before tax season covers the most common areas where self-employed filers leave money on the table.

| Income Level (Annual) | Suggested Tax Reserve Rate | Estimated Annual Set-Aside | Quarterly Payment |

|---|---|---|---|

| Under $50,000 | 25% | $12,500 | $3,125 |

| $50,000 – $100,000 | 30% | $15,000 – $30,000 | $3,750 – $7,500 |

| $100,000 – $150,000 | 32% | $32,000 – $48,000 | $8,000 – $12,000 |

| Over $150,000 | 35% | $52,500+ | $13,125+ |

These figures assume no business deductions have been applied yet. After accounting for deductible home office, equipment, professional development, and health insurance premiums, your actual tax liability will typically be lower, which is why overcautious reserves are better than thin ones. Refund the overage to yourself at filing; never borrow from the tax reserve during a slow month.

Freelancers who receive payments from international clients should account for platform fees (typically 5-20% on platforms like Upwork or Fiverr) and potential currency conversion losses when calculating their effective income. A quoted rate in euros or pounds may convert to meaningfully less than expected; build this into your baseline income calculation rather than treating it as an unexpected deduction.

Frequently Asked Questions

How much should a freelancer have in an emergency fund?

Freelancers should maintain at least six months of essential living expenses in an emergency fund, more than the three-to-six months typically recommended for salaried employees. Freelancers with highly seasonal work or who rely on a small number of large clients should target nine to twelve months, because a single client departure can eliminate a significant share of monthly revenue immediately.

What percentage of freelance income should go to taxes?

Reserve 25-35% of every payment for taxes, covering federal income tax and the self-employment tax of 15.3% on net earnings. The exact rate depends on your total annual income and filing status; higher earners should lean toward 35% to avoid underpayment penalties. Move this amount to a dedicated savings account before spending anything else.

Should I use a separate bank account for my freelance business?

Yes. The IRS recommends separate business and personal accounts for self-employed individuals, and the practical benefits extend well beyond compliance. Separate accounts make it straightforward to track deductible expenses, calculate true profit, and maintain the discipline of paying yourself a fixed monthly salary rather than spending whatever arrived that week.

What is the best budgeting method for irregular income?

The zero-sum budget works well for freelancers because it assigns every dollar of your baseline income to a specific category before the month begins, including explicit allocations for savings and tax reserves. Combined with a baseline income figure drawn from your lowest reliable month (not your average), it creates spending rules that hold up even in low-revenue months without requiring constant recalculation.

How do I handle a month when income is much lower than usual?

Draw from your income-smoothing savings account to maintain your fixed personal salary transfer. This is precisely what that account exists for; using it during a slow month is working as intended. The emergency fund stays untouched unless the slow period extends beyond what the smoothing account can cover.

When should a freelancer start contributing to a retirement account?

Start contributing as soon as your buffer reaches at least three months of expenses, even if contributions are small initially. A SEP IRA or Solo 401(k) contribution timed to your year-end tax situation allows you to reduce taxable self-employment income significantly. Base your contribution on your conservative baseline projection, not on a strong quarter, to avoid overstating your available cash for the year.

Sources

- National Bureau of Economic Research (2025), Earnings of Self-Employed Workers

- Federal Reserve Board (2024), Economic Well-Being of U.S. Households: Savings and Investments

- Internal Revenue Service, Publication 334: Tax Guide for Small Business

- Internal Revenue Service, One-Participant 401(k) Plans (Solo 401k)

- Internal Revenue Service, SEP Plan Overview and Contribution Limits