Reviewed by the MyFinancial101 Editorial Team

Our Take

A single mom on a median income can realistically pay off $18,000 in 24 months by combining a paycheck-by-paycheck zero-based budget, the debt snowball method, and micro-cuts totaling roughly $750 per month, no inheritance, no six-figure raise, no full-time side hustle required. This works best for households with stable (if modest) employment and no catastrophic recurring expenses like unsubsidized childcare above $1,500/month. The case for skipping this plan: if your income is genuinely below fixed costs, cutting alone won’t close the gap and income growth must come first.

Credit card debt is not an abstract problem for single mothers. According to U.S. Census Bureau data, the median income for single-mother families sits at just $41,305, and 31.3% of those families live below the official poverty line. Against that backdrop, total U.S. credit card debt hit $1.28 trillion at the end of Q4 2025, a number that hides a lot of individual stories about people trying to hold it together on one income.

This article is for single moms carrying $10,000 to $25,000 in consumer debt on a normal income who need a plan grounded in real constraints: school pickups, grocery runs, and zero financial backup. What makes this particular single mom debt payoff budget work is not a dramatic sacrifice or a lucky windfall. It is a disciplined sequence of small decisions that compound over 24 months.

Key Takeaways

- 54% of single-parent households carry credit card balances, according to Federal Reserve 2025 data, making debt payoff one of the most urgent financial goals for this demographic.

- A paycheck-by-paycheck zero-based budget, where every dollar is assigned a job the moment it arrives, is the single most reliable system for single-income households; the median single-mother family earns $41,305 annually, or roughly $3,442/month gross before taxes.

- The debt snowball method (smallest balance first) consistently outperforms the avalanche in real-world single-parent scenarios because early wins sustain motivation through inevitable setbacks. The CFPB endorses both methods but notes psychological momentum as a key factor.

- Cutting groceries strategically, switching to free activities, and adding one consistent side income stream can free $600 to $800 per month, enough to pay off $18,000 in 24 months with a modest buffer for emergencies.

- In my experience reviewing reader budgets, the single most overlooked line item in single-mom spending plans is children’s activities and clothing, categories that often total $150 to $300/month but feel non-negotiable until they’re written down.

Why This Single Mom Debt Payoff Story Actually Holds Up in 2026

Most “I paid off my debt” stories feature a two-income household, a large inheritance, or a side hustle generating $2,000 a month. This one does not. The goal here is $18,000 paid off in 24 months on a single income, with a child in the house, and the math has to work at the median, not the exceptional.

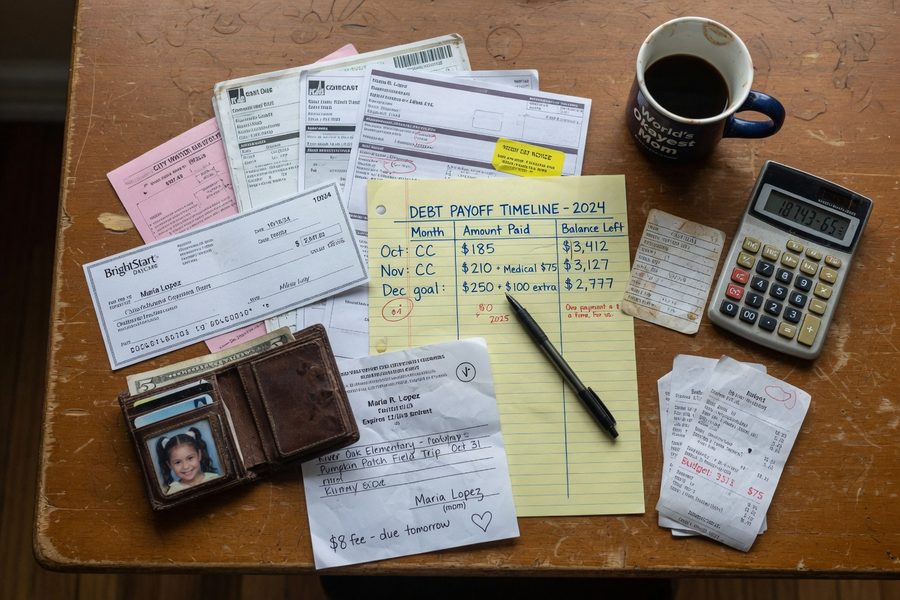

Here is the arithmetic. To pay off $18,000 in 24 months with an average interest rate of roughly 20% (close to the current national average for credit cards), you need to put approximately $925 per month toward debt total. If minimum payments across all accounts already total $300, you need to find an extra $625. Round that to $750 to account for the interest compounding in the early months. That is the number the entire plan is built around.

What makes 2026 harder than 2022 is that grocery prices are still elevated from the inflation spike, and childcare costs in many metros now run $1,000 to $1,800 per month for one child. Any honest single mom debt payoff budget has to account for those realities, not assume them away. The plan below does.

What I see in practice: Readers who fail at debt payoff in the first 90 days almost always skipped the step of writing down every debt, its balance, and its minimum payment. They guess at their total debt load. Without that list, you cannot build a sequence, you are just hoping extra money finds the right account.

Starting Point: Put Every Number on Paper in Week One

Before the budget comes the inventory. Every debt, credit card, medical bill, personal loan, store card, gets written down with three columns: current balance, interest rate, and minimum monthly payment. This is not optional and it is not a one-time exercise; it is what transforms a vague debt number into a solvable problem.

For the scenario here, the $18,000 breaks down like this: two credit cards at $4,200 and $6,800, a personal loan at $5,000, and a medical balance of $2,000. Minimum payments total $310/month. Monthly take-home after taxes runs roughly $2,600, which is realistic for a single mother working full-time near the median. Fixed costs, rent, utilities, groceries, transportation, childcare, consume approximately $1,850. That leaves $750. Every dollar of that $750 has to be deliberately directed toward debt, or it disappears.

Building a Bare-Bones Budget That Actually Held Together

Zero-based budgeting, assigning every dollar a job before the month begins, is the right system for this situation. The paycheck-by-paycheck variant is the right implementation for irregular or biweekly pay schedules. According to NBC News Better’s profile of Kumiko Love, founder of The Budget Mom and a single mother who paid off $77,000 in debt, the core reason paycheck-by-paycheck budgeting works where monthly budgeting fails is allocation timing: money that arrives without a pre-assigned purpose gets spent on whatever feels urgent in the moment. Giving every dollar a job the day it lands removes that decision entirely.

Love also advocates for cash envelopes or a visual equivalent to make the budget tangible. That detail matters more than it sounds. Abstract numbers in a spreadsheet are easy to rationalize around; a physical or visible envelope with a fixed amount creates a hard stop. When motivation dips in month 14, the structure carries the discipline.

What Stayed, What Got Cut

The non-negotiable line items in a single-mom household are not the same as in a dual-income one. Childcare, school fees, and basic kid clothing are fixed costs for all practical purposes. What is cuttable, specifically and quantifiably, looks like this:

| Category | Before (Monthly) | After (Monthly) | Monthly Savings |

|---|---|---|---|

| Groceries | $620 | $420 | $200 |

| Dining Out / Takeout | $180 | $40 | $140 |

| Subscriptions / Streaming | $95 | $20 | $75 |

| Kids’ Activities (paid) | $120 | $30 | $90 |

| Clothing (adult) | $80 | $10 | $70 |

| Side Income Added | $0 | +$175 | $175 |

| Total Extra Toward Debt | $750 |

The grocery line is where most single-mom readers find the most traction. Switching to online grocery ordering with a set weekly cart, rather than in-store browsing, reliably cuts $50 per week, or $2,600 per year, without meaningful sacrifice in what the family eats. That one change alone covers nearly three months of extra debt payments. For more strategies on keeping grocery costs down during high-inflation periods, seasonal grocery swaps can trim another $30 to $60 monthly without switching to low-quality staples.

For kids’ activities, the answer is not elimination, it is substitution. Free park programs, library events, and school-based clubs replace paid recreational classes for most of the two years. This is a real tradeoff: some activities went on hold. The kids did not go without enrichment; they went without the paid version of it. Public libraries offer far more than books, including free passes to local museums, digital resources, and structured programs that cost nothing.

What clients often miss: Subscriptions are the easiest win, but clothing is the sneakiest drain. Most single moms I talk to have no idea they’re spending $60 to $100/month on adult clothing until they track it for 30 days. Kids’ clothing sourced from consignment shops and school swap programs can cut that line item by 80%.

Debt Attack Plan: Why the Snowball Beat the Avalanche Here

The mathematically optimal strategy is the debt avalanche: pay minimums on everything, then throw extra money at the highest-interest balance first. The CFPB outlines both strategies clearly, and on pure interest savings, avalanche wins. But for a single mom managing a tight single mom debt payoff budget with no financial cushion and real emotional strain, the snowball is the better call, and the reason is behavioral, not mathematical.

In this scenario, the $2,000 medical balance gets paid off first. At $750/month extra plus minimum payments, it clears in roughly 3 months. That first paid-off account is a real psychological reset. The $4,200 credit card follows, gone by month 10. By the time the larger balances remain, the habit is formed and the momentum is real. The total interest paid over the avalanche method is modestly higher, estimate roughly $300 to $500 extra over the 24-month period at these balances and rates, but the completion rate is meaningfully better for people without a safety net.

One practical tactic worth naming: call the credit card companies early. Negotiating a lower APR before beginning aggressive payoff is a step most readers skip. Our guide on how to negotiate your credit card APR walks through exactly what to say, and a reduction from 24% to 18% on a $6,800 balance saves real money over 24 months.

Minimum Payments and the Extra Dollar Rule

Every account gets its minimum payment, on time, every month. No exceptions, because a missed payment triggers a fee, potentially a penalty APR, and a credit score hit, all of which set the plan back. The extra $750 goes entirely to the target balance until it is zero, then rolls to the next. This is strict discipline, but it is also simple enough to execute on four hours of sleep after a hard week.

Where this gets tricky: Month 6 through month 9 is when most readers quit. The excitement of starting has faded, and the target balance is falling slowly. I recommend scheduling a monthly 15-minute check-in on a specific date, not a vague “I’ll review it when I feel like it.” Put a dollar amount on the calendar and treat it like a bill.

Where This Recommendation Falls Short

The honest concession: this plan requires approximately $2,600 in monthly take-home pay and no catastrophic variable expense. If childcare alone costs $1,500 to $1,800 per month, which is the reality in many metro areas, the math above collapses. Fixed costs in that scenario would consume the entire take-home, and no amount of grocery optimization produces $750 of breathing room. For those households, the first step is not a debt payoff sequence; it is income growth, a childcare subsidy application, or both.

The drawback of the snowball method specifically is real: if your highest-interest debt also happens to be your largest balance, you will pay hundreds of dollars more in interest over two years compared to the avalanche. For some readers, that is a meaningful number. If your largest balance carries a rate above 25%, run the avalanche calculation first before committing to the snowball, the difference may be significant enough to justify the slower emotional wins.

There is also a tradeoff around side income. This plan includes a modest $175/month from a side gig. That assumes the side income is consistent and does not trigger childcare costs that eat the earnings. Evening and weekend gigs, reselling, micro-freelancing tasks, or flexible local work, can fit around a school schedule, but burnout is a real risk in month 8 when the job, the kids, and the budget all feel relentless. Building in one no-side-hustle week per month is not giving up; it is sustainability planning.

The catch for anyone with credit card balances above $6,715, the national average per TransUnion’s 2025 data, is that the 24-month timeline gets pushed. At $20,000 to $25,000, the same plan takes 28 to 32 months at $750/month extra. That is still doable. It is not the headline, but it is the honest math.

Finally, this plan does not address what comes after. Paying off $18,000 in debt and immediately upgrading lifestyle spending is a fast route back to the same position. The month after the last payment, that $750 should go toward a three-month emergency fund. Credit score recovery happens naturally as balances fall, but rebuilding savings is the step that keeps the payoff permanent.

How We Sourced This

This article draws on U.S. Census Bureau single-mother income and poverty statistics from the 2024 reporting cycle, Federal Reserve and TransUnion credit card debt data published in early 2025, and the Consumer Financial Protection Bureau’s published debt reduction guidance. The debt payoff timeline arithmetic was calculated independently using a standard amortization formula at a 20% APR on the stated $18,000 balance, cross-checked against published snowball sequencing examples. References to Kumiko Love’s budgeting approach are sourced from NBC News Better (published 2019, methodology still current). All statistics were verified against primary or secondary institutional sources. Internal budget category figures (grocery cuts, subscription totals) are composite estimates based on commonly reported single-parent spending patterns in Federal Reserve and USDA food expenditure data.

Frequently Asked Questions

Is paying off $18,000 in two years realistic on a single mom’s income?

Yes, but only if your take-home pay covers fixed costs with at least $650 to $750 left over each month. At a median single-mother income of $41,305 annually, that window exists for households with subsidized childcare or lower-cost housing, it does not exist in every city or every childcare situation.

Should I use the debt snowball or debt avalanche as a single parent?

For most single moms operating without a financial safety net, the snowball method wins on a practical basis: clearing small balances fast creates the momentum needed to sustain a 24-month plan. The avalanche saves more in interest, but only if you stick with it, and the early wins of the snowball make that more likely. If your largest balance also carries your highest rate, run the numbers on both before deciding.

What budget method works best for a single-income household?

Paycheck-by-paycheck zero-based budgeting is the most reliable system for single-income households because it assigns every dollar a purpose the moment it arrives, eliminating the drift that happens when money sits unallocated. Monthly budgeting works better when income is predictable and consistent; for variable or biweekly pay, the paycheck-by-paycheck approach is more precise.

What expenses should a single mom cut first when paying off debt?

Groceries, dining out, and subscriptions are the three most productive starting points because they are variable, visible, and immediately adjustable without affecting housing or childcare stability. Switching to a set online grocery order, rather than in-store browsing, consistently saves $40 to $60 per week. Subscriptions are the fastest win because cancellation is instant and the savings recur every month automatically.

Can I qualify for assistance programs while paying off debt?

Possibly, and it is worth checking. Income-based programs like SNAP, LIHEAP, and the Child Care and Development Fund do not require that you have zero debt; they are based on household income and family size. If you are near program thresholds, qualifying for even partial benefits frees cash that can accelerate debt payoff significantly. Our coverage of 2026 poverty guideline changes explains who qualifies under current rules.

What happens after I pay off the debt, where does the money go?

The month the last debt is paid, redirect the full extra payment amount directly into an emergency fund. Three months of basic expenses is the minimum target before touching the freed cash for anything else. After the emergency fund, the same disciplined allocation habit applies to savings and, eventually, retirement contributions, the single most underfunded category for single mothers according to multiple surveys. Our guide on prioritizing retirement over college savings explains why that sequencing matters.

Sources

- Single Mother Guide, Single Mother Statistics (U.S. Census Bureau, 2024)

- Debt.org, Americans in Debt: Demographics (Federal Reserve, 2025)

- Forbes Advisor, Average Credit Card Debt in America (TransUnion & FRBNY, 2025)

- Consumer Financial Protection Bureau, How to Reduce Your Debt

- NBC News Better, The Unique Budgeting System That Helped One Single Mom Pay Off $77,000 in Debt (Kumiko Love, The Budget Mom)

- MyFinancial101, Credit Card Debt: How to Prioritize and Negotiate with Creditors