Fact-checked by the MyFinancial101 editorial team

The Verdict

The standard deduction wins for most filers. Take it without hesitation if your itemizable expenses fall below $32,200 (married filing jointly, 2026) or $16,100 (single). Itemizing makes sense only if you own a home in a high-tax state, carry significant mortgage interest, and your total Schedule A deductions clear that threshold, a profile that fits roughly 14% of all filers.

The debate over standard deduction vs itemizing gets framed as a puzzle every American must solve, but for most households the math resolves in under five minutes. The single factor that swings the decision is whether your actual, documentable deductions, mortgage interest, state and local taxes, charitable gifts, qualifying medical expenses, add up to more than your filing-status standard deduction amount. For 2026, that bar is higher than it has ever been: IRS Publication 505 sets the standard deduction at $32,200 for married filing jointly, up from $31,500 in 2025, following both a legislative boost from the One Big Beautiful Bill Act (OBBBA) and a standard inflation adjustment from the Internal Revenue Service.

The reason this decision matters right now is that the OBBBA permanently locked in the higher standard deduction amounts and overhauled the SALT cap in ways that affect whether itemizing even enters the conversation for middle-income homeowners. Getting this wrong in either direction costs real money: either you overpay by missing legitimate deductions, or you waste hours of record-keeping for zero tax benefit. Tax software from providers like TurboTax and H&R Block will run the comparison automatically, but you still need to understand which side of the line you are on before you sit down to file.

| Factor | Reasons to Take the Standard Deduction | Reasons to Itemize |

|---|---|---|

| Simplicity | No receipts, no Schedule A, no documentation | Requires year-round record-keeping and Form 1098, state tax statements, and donation receipts |

| Dollar threshold | Guaranteed $16,100 (single) or $32,200 (MFJ) deduction in 2026, no questions asked | Your Schedule A total must exceed your standard deduction or you gain nothing |

| Homeownership | Renters almost never exceed the standard deduction threshold | Mortgage interest on up to $750,000 of acquisition debt is deductible; substantial in early loan years |

| SALT deductions | Filers in no-income-tax states (TX, FL, NV, TN) have little SALT to deduct | SALT cap rose to $40,400 for 2026 under the OBBBA, meaningful for high-tax-state homeowners |

| Senior filers | The $6,000 senior bonus deduction (age 72+, through 2028) is available to standard-deduction filers too | Seniors with large medical expenses above 7.5% of AGI may still benefit from Schedule A |

| High earners | Filers with MAGI above $640,600 (single, 2026) face a new cap limiting itemized deduction value to the 35% bracket rate | Homeowners earning $200K–$500K in high-tax states are the clearest beneficiaries of the new SALT cap |

| Charitable giving | Cash donations below the new 0.5%-of-AGI floor produce no additional Schedule A benefit in 2026 | Large donors, gifts of appreciated securities, donor-advised funds, can still push itemized totals past the threshold |

| Filing status trap | Married filing separately filers lose the standard deduction entirely if the other spouse itemizes | N/A, itemizing is the only path for the MFS filer whose spouse already itemizes |

Key Takeaways

- Your total itemizable expenses, mortgage interest, SALT, charitable donations, qualifying medical, must exceed $32,200 (MFJ) or $16,100 (single) in 2026 before itemizing saves you a single dollar.

- You own a home with a mortgage on acquisition debt of $750,000 or less, and you are paying meaningful interest, not a near-paid-off loan where interest has shrunk to a few thousand dollars.

- You live in a state with income or property taxes high enough to contribute meaningfully to the SALT cap, and your combined SALT is above $10,000 (the old baseline that mattered before the OBBBA expansion).

- Your modified adjusted gross income falls below $500,000 (the point where the expanded SALT cap starts to phase out), so you can access the full $40,400 SALT ceiling.

- You have documentation for every deduction you plan to claim, Form 1098 for mortgage interest, state tax records, and written acknowledgment for any charitable contribution of $250 or more.

- You have checked your state’s conformity rules, since some states let you itemize on the state return even when you took the federal standard deduction, a step that can add savings independent of your federal choice.

- You are not in the Alternative Minimum Tax (AMT) danger zone, where SALT deductions become a preference item and AMT can claw back part of the benefit you expected from itemizing.

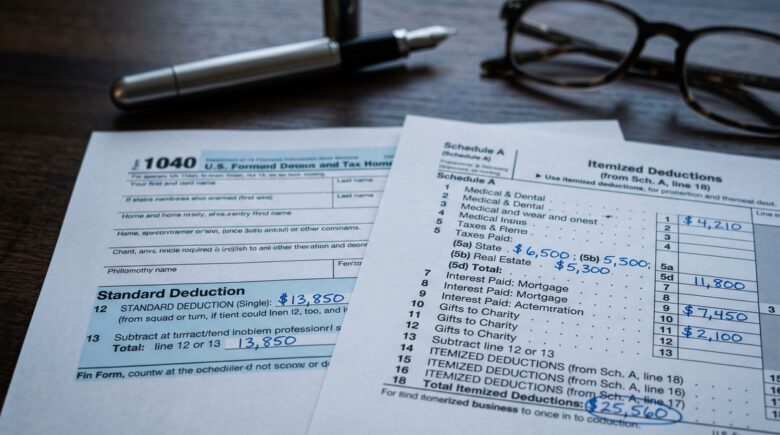

What the Standard Deduction Actually Gives You in 2026

Most people underestimate how generous the standard deduction has become. For 2026, the IRS confirms the standard deduction at $16,100 for single filers, $32,200 for married filing jointly or qualifying surviving spouses, and $24,150 for heads of household. These figures reflect two compounding increases: first, the OBBBA added $750 for single filers and $1,500 for joint filers above prior law in 2025, then the Tax Foundation notes a further inflation adjustment of $350 (single) and $700 (joint) for 2026. The result is that the threshold for itemizing to win has moved substantially higher than it was even three years ago.

The standard deduction is not always a single flat number. Filers age 65 or older, or who are blind, receive an additional amount on top of the base figure, and the OBBBA introduced a $6,000 senior bonus deduction available through 2028 for filers age 72 and older. Critically, that $6,000 bonus is available to both standard-deduction filers and itemizers, which directly undercuts the argument that seniors must itemize to capture their full tax benefits. There is also a hard forced exception: if you are married filing separately and your spouse chooses to itemize, your own standard deduction drops to zero, you must itemize too, even if your Schedule A comes up short.

One practical note on recordkeeping: lenders like Chase, Wells Fargo, and Rocket Mortgage typically mail Form 1098 mortgage interest statements by January 31. If you are considering itemizing, pull that document before you do anything else. It is the single largest deduction for most homeowners, and the number on it often tells you within minutes whether you have any realistic chance of clearing your standard deduction threshold.

The SALT Cap Overhaul: Who It Actually Flips Back to Itemizing

The expanded SALT cap is the biggest structural change in years, but it does not flip the calculation for as many people as the headlines suggest. The cap on state and local tax deductions rose from $10,000 to $40,400 for single filers and joint filers alike in 2026 under the OBBBA. That matters, but only if your total Schedule A clears the standard deduction hurdle first. You do not capture SALT savings just by having high state taxes; you have to itemize in full.

Here is a concrete worked example. A married couple in New Jersey pays $14,000 in property tax and $18,000 in state income tax, for a combined SALT of $32,000. They also pay $15,000 in mortgage interest. Their Schedule A total: $47,000. That clears the $32,200 MFJ standard deduction by $14,800. If their marginal federal rate is 22%, that $14,800 difference reduces their federal tax bill by roughly $3,256. For this household, itemizing clearly wins.

Two dynamics are almost entirely absent from most coverage of the SALT change. First, the cap phases out for MAGI above $500,000, dropping $100 per $1,000 of income over that threshold, so a filer at $700,000 sees the cap shrink from $40,400 toward $20,400. Second, and less discussed, is what the Tax Foundation and other analysts call the SALT marriage penalty: the $40,400 ceiling is shared by a married couple filing jointly, while two unmarried co-owners of the same property each get their own individual $40,400 ceiling. Two single people who together own a home could each deduct up to $40,400 of SALT, for a combined potential deduction of $80,800, double what a married couple filing jointly can claim. This asymmetry is rarely worked through in plain terms, and it is a real consideration for high-SALT-state couples weighing filing strategy.

One more planning note: the expanded SALT cap reverts to $10,000 in 2030 unless Congress extends it. The 2026–2029 window is a limited planning opportunity, not a permanent feature of the tax code. Homeowners in high-tax states who expect to itemize during this period should consider whether accelerating prepayments of state estimated taxes or property taxes into these years, while the higher cap is available, makes financial sense given their projected income. A CPA or enrolled agent who works with the IRS tax code regularly can stress-test this kind of multi-year strategy against your actual debt-to-income ratio (DTI) and income trajectory.

Who Actually Itemizes, and Why the 14% Figure Is the Right Anchor

About 14.2% of taxpayers are projected to itemize in 2026, up from roughly 9–11% in recent post-TCJA years, but still far below the 30% who itemized before the 2017 Tax Cuts and Jobs Act. Even the largest SALT change in a generation moves the needle only modestly. That is the right frame for this decision: itemizing is not a savvy move that most people are missing, it is a genuinely useful tool for a specific minority of filers.

The Joint Committee on Taxation data is worth sitting with: the Peter G. Peterson Foundation, citing Joint Committee on Taxation estimates, found that 84% of the tax benefits from deductions for state and local taxes, charitable contributions, and mortgage interest go to taxpayers with incomes over $200,000. That is not an argument against itemizing if you qualify, it is a reality check that itemizing is structurally most valuable to high-income households with large mortgages and significant state tax bills. Middle-income filers who itemize often do so for modest gains that may not justify the documentation burden.

There is also a 2026-specific wrinkle for very high earners. Filers in the 37% bracket, above $640,600 for single filers, face a new rule that caps the tax value of their itemized deductions at the 35% bracket rate. Every dollar of itemized deductions above the standard deduction saves them 35 cents rather than 37 cents. The difference sounds small but compounds across tens of thousands of dollars in deductions. Combined with the AMT, which treats SALT deductions as a preference item, some high-income filers who expect a windfall from itemizing will find the actual savings are trimmed by two separate mechanisms simultaneously. The Consumer Financial Protection Bureau (CFPB) has noted that tax complexity disproportionately affects consumers who lack access to professional tax guidance, and this is one area where that observation lands squarely.

Credit profile also matters in ways that intersect with this decision indirectly. Homeowners carrying a FICO Score below 680 often hold mortgages with higher annual percentage rates (APR), which means larger interest payments that are more likely to push Schedule A past the standard deduction threshold. Paradoxically, the borrowers who pay the most in mortgage interest because of weaker credit may actually be better positioned to benefit from itemizing, though that is a poor reason to celebrate a high APR. Experian and Equifax both publish guidance on how mortgage interest affects credit utilization calculations, a separate but related financial planning consideration.

For context on where itemizing fits within a broader personal finance picture: if you are also managing high-interest debt, the math on which path saves you more may be secondary to more urgent priorities. Our breakdown of how to prioritize and negotiate credit card debt covers the calculus of where to direct cash first, and tax savings from itemizing rarely outrun the drag from carrying a high-rate balance.

Who Should and Who Should Not

Good candidates

The filer most likely to benefit from itemizing has a clear, specific profile, not just “someone with a lot of deductions.”

- A homeowner in California, New York, New Jersey, or another high-income-tax state earning between $200,000 and $500,000, with mortgage interest above $10,000 and combined SALT near or at the $40,400 cap. This is the exact household the expanded SALT cap was designed to benefit.

- A filer with large, documented medical expenses, costs exceeding 7.5% of AGI, such as someone who had a major surgery or ongoing specialist care not covered by insurance in 2026.

- A married couple filing separately where one spouse already itemizes, making itemizing mandatory for the other regardless of their individual Schedule A totals.

- A high-income donor who gives appreciated securities or contributes to a donor-advised fund, generating Schedule A totals that dwarf the standard deduction threshold without the 0.5%-of-AGI charitable floor being a limiting constraint.

- A filer whose state allows itemizing on the state return independent of the federal choice, worth checking before assuming the federal decision settles everything.

Who should skip it

For these filers, itemizing costs time and produces nothing, or less than expected.

- Renters in any state, without mortgage interest or property taxes, it is nearly impossible to accumulate Schedule A deductions above $16,100 (single) or $32,200 (MFJ) unless medical expenses are extraordinary.

- Homeowners in Texas, Florida, Nevada, or Tennessee, states with no income tax, whose SALT consists entirely of property taxes and rarely approaches the expanded cap in a way that, combined with other deductions, clears the standard deduction bar.

- Filers with MAGI above $900,000, where the SALT phaseout has nearly eroded the expanded cap back to the old $10,000 floor and the 35%-bracket cap on deduction value reduces the per-dollar benefit further.

- Anyone who cannot produce documentation, Form 1098 for mortgage interest, written acknowledgment for charitable gifts, and state tax records, before filing. Undocumented deductions are not deductions; the IRS can disallow them entirely on audit. The Federal Deposit Insurance Corporation (FDIC) recommends keeping financial records for at least seven years, which aligns with the IRS audit window for most returns.

One real limitation worth naming: even when itemizing is mathematically correct, it is not free. Professional tax preparation from a CPA or an enrolled agent who specializes in Schedule A returns costs money. Services like SoFi Tax or Jackson Hewitt charge fees that can erode a modest itemizing advantage. If your Schedule A beats the standard deduction by only $800 or $1,000, professional fees may wipe out the net benefit. That is a tradeoff the straightforward comparison tables rarely acknowledge.

Frequently Asked Questions

Is it worth itemizing for a $1,000 difference over the standard deduction?

Probably not. A $1,000 difference over the standard deduction saves you $220 at a 22% marginal rate, before accounting for the time spent gathering documents, the cost of tax software that handles Schedule A, or any professional fees. For most filers, that math does not clear the bar, and the IRS itself advises taking whichever method produces the lower tax liability, which means the burden is on itemizing to prove its worth by a meaningful margin.

Can I itemize on my state return even if I took the standard deduction federally?

Yes, in several states. A number of states decouple their income tax rules from federal treatment, allowing taxpayers to itemize on the state return regardless of the federal choice. Some states also offer no standard deduction at all, making the federal decision essentially irrelevant to the state calculation. Check your state’s department of revenue directly. Assuming your federal decision automatically carries over is one of the more common and costly filing errors, and state revenue agencies, unlike the IRS, rarely publicize the discrepancy proactively.

Does the new $6,000 senior bonus deduction mean seniors should itemize?

No, the $6,000 senior bonus deduction for filers age 72 and older is available whether you take the standard deduction or itemize, so it does not tip the scales toward Schedule A on its own. Seniors with large medical expenses above 7.5% of AGI may still find itemizing worthwhile, but the senior bonus alone is not a reason to switch methods. For broader context on government benefit programs available to seniors managing tight budgets, see our overview of who benefits from the 2026 poverty guideline changes.

What happens to the SALT deduction in 2030?

The expanded $40,400 SALT cap is scheduled to sunset back to $10,000 in 2030 unless Congress passes new legislation to extend it. That makes 2026 through 2029 a finite planning window, not a permanent feature of the tax code. High-tax-state homeowners who benefit from itemizing now should factor that clock into any multi-year tax planning, particularly if they are considering accelerating prepayable state taxes or property taxes into the years before the cap shrinks. If you are also tracking how federal legislative changes are affecting household finances more broadly, our piece on SNAP benefits amid federal budget standoffs covers related ground.

Sources

- Internal Revenue Service, Publication 505: Tax Withholding and Estimated Tax (2026 Standard Deduction Amounts)

- Internal Revenue Service, Instructions for Schedule A (Form 1040): Itemized Deductions

- Internal Revenue Service, IRS Releases Tax Inflation Adjustments for Tax Year 2026, Including Amendments from the One Big Beautiful Bill

- Internal Revenue Service, New and Enhanced Deductions for Individuals

- Tax Foundation, 2026 Tax Brackets, Standard Deduction Amounts, and OBBBA Adjustments

- Peter G. Peterson Foundation, 8 Key Charts on Tax Breaks (citing Joint Committee on Taxation)

- MyFinancial101–2025 Refund: Free IRS Tax Help and One Credit Families Overlook