Fact-checked by the MyFinancial101 editorial team

The Verdict

A high-yield savings account is usually the better default if your balance is under $2,500 or you want zero fees and no minimums. A money market account wins when you need check-writing or debit access tied directly to your savings, and you can consistently maintain the minimum to avoid rate penalties. Both are safe, insured choices; the decision turns on access needs and balance size, not yield.

The high yield savings vs money market debate looks more complicated than it actually is. Both account types are FDIC-insured, both currently offer APYs in the 3.9–4.15% range at top online institutions, and both are variable-rate products that will drift down as the Federal Reserve continues its gradual easing cycle. The single factor that swings the decision for most people is not yield at all, it is how much access to your cash you need and how reliably you can meet a minimum balance requirement.

That distinction matters more in mid-2026 than it did a few years ago, because the gap between “best-in-class” and “settling for the national average” is enormous. The FDIC’s June 2026 national rate data shows the average savings account paying just 0.38% APY, while top high-yield accounts pay more than ten times that. Choosing wrong means leaving real money on the table.

| Factor | Reasons to Choose High-Yield Savings | Reasons to Choose Money Market Account |

|---|---|---|

| Minimum Balance | Many online HYSAs require $0 minimum to open and earn top APY | MMAs often require $2,500–$10,000 to unlock the highest rate tier |

| Monthly Fees | Online HYSAs typically charge no monthly maintenance fee | Some MMAs charge $10–$25/month if balance drops below threshold |

| Check Writing | Not available on standard HYSAs | Most MMAs include check-writing privileges |

| Debit Card Access | Rarely offered; cash usually moved via ACH transfer | Many MMAs include a debit card for direct spending |

| Rate Transparency | Single flat APY for most balances; easy to compare | Tiered rates make true yield harder to assess without reading fine print |

| FDIC Insurance | Fully covered up to $250,000 per depositor per bank | Identical FDIC or NCUA coverage, no advantage either way |

| Rate on Rate Drops | Both reprice quickly; no structural lag difference | Same variable-rate risk; neither holds a rate guarantee |

Key Takeaways

- Your balance is under $2,500, making it hard to consistently meet MMA minimum requirements without risking fee penalties

- You want to earn the top APY (3.9–4.15%) without reading tiered-rate fine print

- You have no need to write checks or swipe a debit card directly from your savings account

- You are comfortable moving money via ACH transfer, typically 1–2 business days, to your checking account before spending

- You want FDIC insurance with zero monthly fee risk and no balance-maintenance discipline required

- You are saving for an emergency fund or specific goal and do not plan to make frequent withdrawals

- You prefer simplicity: one flat rate, no tiers, no penalty structures to track

Do the Rates Actually Differ Between the Two?

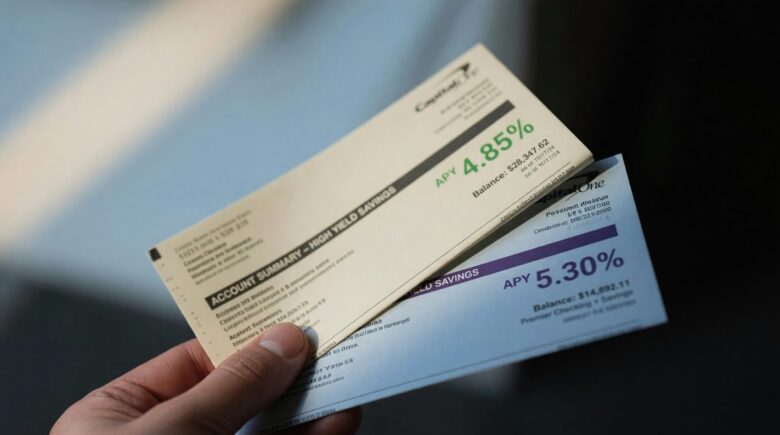

At the top of the market, the honest answer is no. Both HYSAs and MMAs at competitive online banks are advertising APYs between 3.9% and 4.15%, a spread so tight it is not a deciding factor. Where rates diverge sharply is between the best accounts and the national average. The FDIC reports the national average for money market accounts at 0.61% APY and for standard savings at just 0.38% APY. A saver with $10,000 who settles for a national-average savings account earns roughly $38 a year. The same balance in a top HYSA earns closer to $400.

Here is the arithmetic that actually matters. Take a $10,000 balance. At the national average savings rate of 0.38% APY, annual interest is $38.00. At a top HYSA or MMA rate of 4.00% APY, annual interest is $400.00. The difference is $362 per year, or about $30.17 per month. Over five years with no additional deposits and compounding monthly, the top-rate account produces roughly $2,163 in interest versus $191 at the national average. The brand of account matters far less than picking one that offers a competitive rate, and then actually opening it.

One real caveat worth naming: both products carry variable rates. The Federal Reserve has been in a gradual easing cycle since late 2024, and top rates have already drifted down from the 5.00–5.25% peaks seen in 2023. Expect further compression. Neither HYSAs nor MMAs are immune to rate cuts, and no institution locks in a promotional APY indefinitely. If you are parking money here expecting a fixed return, recalibrate that expectation.

Are Both Accounts Actually Safe?

Both are equally safe, with one important distinction to watch. The CFPB confirms that money market deposit accounts at banks are insured by the FDIC, and those at credit unions are covered by the NCUA, up to $250,000 per depositor per institution. High-yield savings accounts at FDIC-insured banks carry the same protection at the same limit. If your combined deposits at a single institution stay under $250,000, both accounts are equally bulletproof.

For couples or families, the joint account structure matters. A joint account at an FDIC-insured bank is covered up to $500,000–$250,000 per co-owner. That means a household with $400,000 in savings can hold it fully insured in a single joint account rather than splitting it across two institutions. This is a practical edge that rarely gets discussed in the standard high yield savings vs money market comparison, but it is worth understanding before you spread cash around unnecessarily.

The one entity that should not be confused with either product is the money market fund. Money market funds are investment products sold through brokerage accounts by firms like Vanguard, Fidelity, and Schwab. They are not FDIC-insured. They aim to maintain a $1.00 net asset value but are not legally required to do so. For cash you genuinely cannot afford to lose, an emergency fund, a near-term down payment, stick with FDIC or NCUA-insured bank accounts, not funds.

The distinction between a high-yield savings account and a money market account comes down to access features, not yield or safety. If your primary goal is earning the highest rate, both products are functionally interchangeable at the top of the market. Check-writing capability is where the MMA earns its place, and for savers who do not need it, that feature carries a cost in the form of higher minimums and more complex fee structures. As Bankrate’s earnings comparison between the two products shows, the real financial gap is not between account types but between competitive and below-average rates across both categories.

Access, Fees, and Minimums: Where the Real Difference Lives

This is the section most comparison articles bury, but it is where the practical decision actually gets made. MMAs typically offer check-writing and debit card access; HYSAs typically do not. If you want to pay a contractor directly from your savings, or need a debit card tied to a high-interest account, an MMA is structurally better suited. If you are comfortable with a 1–2 business day ACH transfer to your regular checking before spending, a HYSA works just fine.

The fee and minimum structure is where HYSAs pull ahead for most people. Online banks like Ally, Marcus by Goldman Sachs, and SoFi offer HYSAs with $0 minimum deposits and no monthly fees at all. MMAs at institutions like Discover, CIT Bank, or traditional banks like Chase often require balances of $2,500 to $10,000 to earn the advertised top rate. Drop below the threshold, and the rate can fall to near national-average territory, or a monthly fee kicks in, which directly offsets your interest earnings. On a $2,500 balance, a $12 monthly fee would consume $144 per year, completely wiping out roughly one-third of your interest income at a 4.00% APY.

The Washington State Department of Financial Institutions notes that money market accounts usually require higher minimum balances than standard savings accounts, a pattern that holds true at most institutions today. If your savings balance fluctuates, that minimum requirement is not just a hurdle at account opening; it is an ongoing risk every month. A HYSA removes that pressure entirely.

If you are still building your emergency fund from scratch, a zero-minimum HYSA is almost always the cleaner starting point. Once you have cleared $5,000–$10,000 in savings and want the convenience of integrated check-writing, revisiting an MMA makes sense. For more context on how cash savings fits alongside other financial priorities, the breakdown in why retirement savings should take priority over college funding is a useful read alongside this decision.

Who Should and Who Should Not

Good candidates for a high-yield savings account

A HYSA fits most people who are building or holding an emergency fund and want maximum yield without complexity.

- Someone with a balance under $5,000 who cannot reliably maintain a minimum without risk of fee penalties

- A renter or single-income household building a 3–6 month emergency fund from a lower base balance

- Anyone who accesses their savings infrequently and is comfortable with ACH transfers rather than direct check-writing

- A person already managing multiple financial accounts who wants their savings to be dead-simple, one rate, no tiers, no fine print

Who should skip the HYSA and choose an MMA

An MMA earns its extra complexity when direct access to savings funds is genuinely part of how you manage money.

- A small business owner or freelancer who occasionally writes checks from a reserve account and needs that function built in (rather than routing through a separate checking account each time)

- A household with $25,000 or more in liquid savings who wants debit access for large periodic expenses like property taxes or insurance premiums

- A retiree living partially off savings who values the convenience of an integrated debit card without maintaining a separate checking account

- Any saver who consistently maintains $10,000 or more in the account and can hold the minimum to access top-tier MMA rates without risk of dropping below it

Frequently Asked Questions

Is a high-yield savings account or money market account better for an emergency fund?

A HYSA is the better default for an emergency fund if you are still building toward your target balance. The $0 minimums and flat fee structure at online banks mean your interest is never eaten by monthly charges, and you do not need check-writing access for most emergency withdrawals, an ACH transfer to your checking account the same or next day covers nearly every scenario. Once your fund is fully funded and stable, an MMA with debit access is a reasonable upgrade if the minimum is easy to maintain.

Are money market accounts and money market funds the same thing?

They are completely different products. A money market account is a bank or credit union deposit account, FDIC or NCUA insured up to $250,000. A money market fund is a mutual fund product sold through brokerage accounts by firms like Fidelity or Vanguard; it carries no federal deposit insurance and, while it targets a stable $1.00 net asset value, that is not guaranteed. For cash you cannot afford to lose, only bank deposit accounts qualify.

What happens to my rate if the Fed cuts interest rates again?

Both HYSAs and MMAs carry variable rates, meaning the institution can lower your APY at any time without notice. As of mid-2026, top rates have already retreated from the 5.00%+ peaks of 2023 in line with Fed easing. The repricing on both products tends to happen quickly, often within 30 days of a Fed move. There is no meaningful structural difference in how fast HYSAs versus MMAs reprice; both follow the federal funds rate closely.

Can I lose money in a high-yield savings account?

Not through market losses. Both HYSAs and MMAs at FDIC-insured banks protect your principal up to $250,000 per depositor per institution. The only way to “lose” money in a HYSA is through fees that exceed your interest earnings, which is why the NCUA advises savers to review account terms carefully, especially for accounts with tiered rates or minimum balance requirements.

Does it make sense to hold both a HYSA and a money market account?

Rarely, and usually not worth the administrative overhead. Holding two high-interest accounts at separate institutions splits your FDIC coverage benefit without meaningfully increasing yield. The better approach for most people is picking one product that fits their access needs and balance size, earning the best available rate, and routing additional cash toward debt reduction or investment accounts. If you are carrying high-interest debt alongside your savings decision, the framework in how to prioritize and negotiate credit card debt is worth reading first.

Sources

- FDIC, National Rates and Rate Caps (June 2026)

- Consumer Financial Protection Bureau, What Is a Money Market Account?

- MyCreditUnion.gov (NCUA), Savings Accounts Overview

- Washington State Department of Financial Institutions, Saving Money: Tips and Resources

- Federal Reserve Bank of St. Louis (FRED), Savings Deposit National Rate (June 2026)

- Bankrate, HYSA vs. Money Market Account Earnings Comparison