Fact-checked by the MyFinancial101 editorial team

Quick Answer

Freelancers can use business credit cards to simplify tax season by keeping all deductible expenses on one dedicated statement, reducing preparation time and audit risk. Most issuers approve sole proprietors using only an SSN and personal credit history. Card rewards are generally nontaxable, and 100% of business-use interest is deductible on Schedule C.

Business credit cards for freelancers solve a problem that shows up every April: a chaotic mix of personal and business charges on a single bank statement that takes hours to untangle. With self-employment taxes running at a flat 15.3% on net earnings, 12.4% for Social Security and 2.9% for Medicare, according to IRS guidance on self-employment tax, every legitimate deduction matters. A dedicated business card creates the clean paper trail that makes those deductions defensible.

The good news is that getting approved is easier than most freelancers assume, and the tax benefits extend well beyond simple record-keeping. This guide covers eligibility realities, the card features that actually matter for Schedule C filers, how to handle rewards at tax time, and the mistakes that quietly erase the benefits you worked to build.

Key Takeaways

- 56% of employer firms used credit cards on a regular basis in 2023, according to Federal Reserve data, business cards are a mainstream financing and record-keeping tool, not just a perk.

- The self-employment tax rate is 15.3% of net earnings (12.4% Social Security + 2.9% Medicare), per the IRS, making deduction accuracy critical for sole proprietors.

- The IRS lists credit card statements as valid supporting documents for business expenses, requiring identification of payee, amount, date, and description, per IRS recordkeeping guidance.

- 55% of businesses reported using business credit cards for financing in the past 12 months, according to National Bureau of Economic Research working paper (2025).

- Annual fees and card interest are deductible in proportion to business use, and most issuers approve sole proprietors using only an SSN, no LLC or EIN required.

In This Guide

- Why Freelancers Struggle with Taxes, and How a Dedicated Card Changes the Game

- Can Freelancers Actually Get Business Credit Cards?

- Choosing the Right Card Features for Tax Season Ease

- Using the Card All Year to Make April Painless

- What Happens to Rewards and Points at Tax Time

- Common Mistakes That Undo the Tax Benefits

Why Freelancers Struggle with Taxes, and How a Dedicated Card Changes the Game

The core problem is not complicated: one bank account, one credit card, and twelve months of mixed personal and business charges. By late March, sorting a year’s worth of transactions into deductible and non-deductible categories becomes the single biggest time drain for most self-employed filers, and errors in that process invite IRS scrutiny. A dedicated business card eliminates most of that work before it starts.

The Hidden Audit Risk of Mixed Accounts

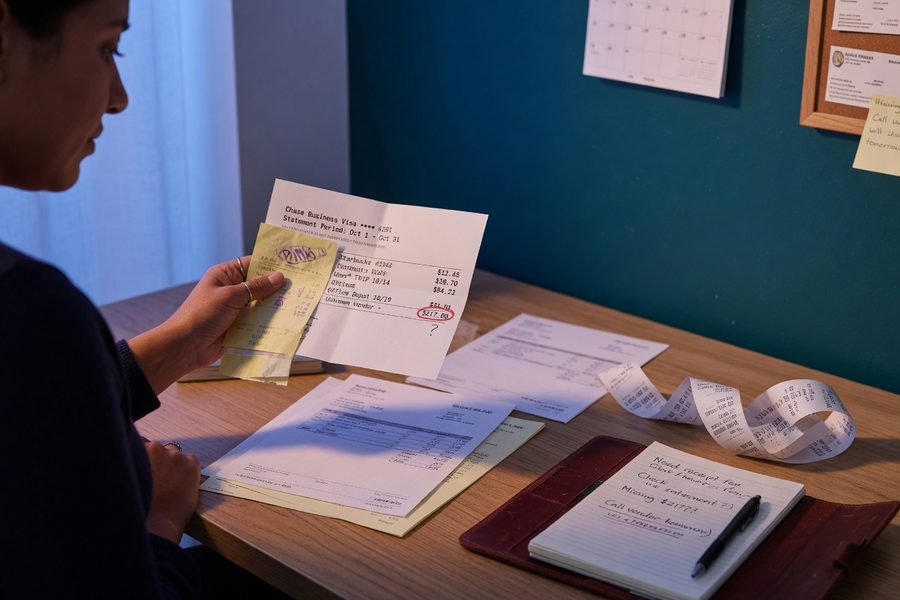

Here’s what underwriters know that most freelancers don’t: the IRS doesn’t just audit suspicious numbers; it audits taxpayers who can’t substantiate their numbers. According to IRS recordkeeping guidance, good records help track deductible expenses and prepare accurate returns, with purchases and other transactions generating supporting documents such as credit card statements. A business card statement is one of those supporting documents. One card, one statement, one clear record.

The mental load matters too. Sorting mixed expenses every April is not just time-consuming; it’s error-prone. Small charges, a $12 Canva subscription, a $47 software license, get missed entirely when they’re buried among grocery runs and restaurant visits. Over a year of 1099 income across multiple platforms, those small misses add up to real money.

The IRS specifically lists credit card receipts and statements among the supporting documents required to substantiate business expenses, including identification of payee, amount, proof of payment, date, and description of the purchase. A dedicated business card statement satisfies nearly all of those requirements in a single document.

If you’re building a freelance income stream and want context on where the self-employment economy is heading, the surge in platform-based independent work is worth understanding, this overview of micro-freelancing trends provides useful background on how the gig economy is reshaping solo income.

Can Freelancers Actually Get Business Credit Cards?

Yes, and far more easily than the name implies. Most major issuers approve sole proprietors using only a Social Security Number and personal credit history. You do not need an LLC, a registered business name, or an Employer Identification Number to qualify.

What Issuers Actually Evaluate

Issuers treat freelance income as legitimate business income. When you apply, you’ll typically report your annual business revenue (even if it’s $20,000 from a few 1099 clients), your personal credit score, and your estimated monthly spending. The personal guarantee is standard, meaning you are personally responsible for the debt, but this is true for virtually every small business card, not just those marketed to freelancers. It’s an honest trade-off: you get a business card with separate reporting and business-specific features, and the issuer gets a creditworthy individual on the hook.

Issuers such as American Express, Chase, Capital One, and Brex all have products designed for self-employed applicants with variable income. Some fintech-oriented cards, including Brex and Ramp, have moved toward models that underwrite based on cash flow rather than personal credit alone, which can be advantageous for freelancers with strong revenue but a thin personal credit file.

According to a 2025 National Bureau of Economic Research working paper, 55% of businesses reported using business credit cards for financing in the past 12 months. Business cards are a standard tool across all firm sizes, not a product reserved for corporations.

Building a Business Credit Profile from Scratch

Consistent use of a business credit card, even a modest one, begins building a record with commercial credit bureaus like Dun & Bradstreet and Experian Business. This matters for freelancers who may eventually need a line of credit to bridge a slow month or cover a large equipment purchase right before a quarterly estimated tax payment is due. A two-year history of on-time payments on a business card is the kind of profile that opens those options when cash flow is tight.

Choosing the Right Card Features for Tax Season Ease

Not all business cards are equally useful at tax time. The features that matter most for Schedule C filers are automatic expense categorization, downloadable year-end summaries, and integration with accounting tools, not just the rewards rate.

Categorization and Reporting Tools

Cards from American Express and Chase Ink provide downloadable transaction reports in CSV or QuickBooks-compatible formats. This matters because Schedule C uses specific line items, advertising, office expense, travel, utilities, and a card that pre-categorizes purchases into those buckets cuts preparation time dramatically. Some platforms, including QuickBooks Self-Employed and Keeper Tax, can pull card transactions directly via open banking connections and flag potential write-offs automatically. A card with strong export features and API integrations is effectively doing a portion of your bookkeeping for you.

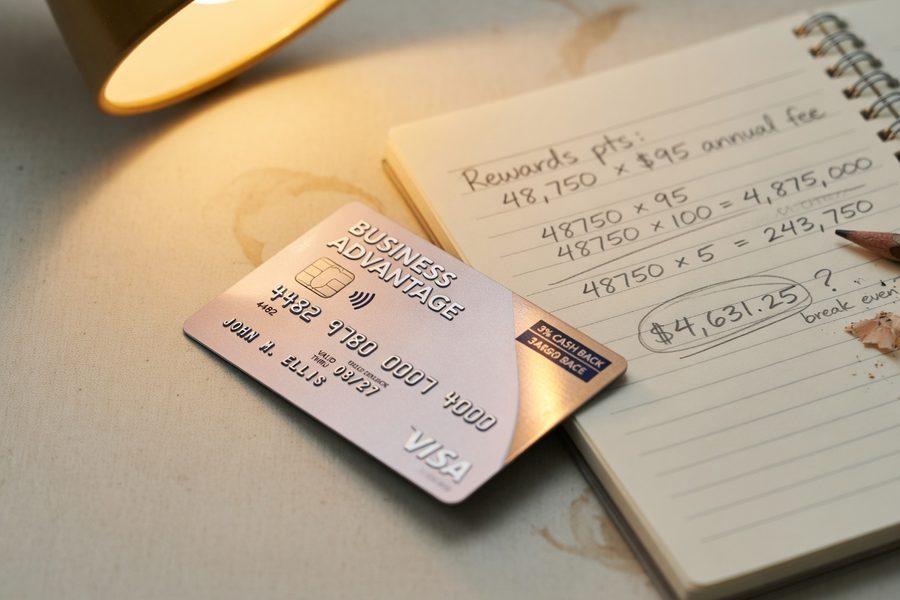

Annual Fees vs. Rewards: Running the Real Math

Here’s the trade-off most articles skip: a card with a $95 annual fee that earns 3x points on software and advertising may deliver more net value than a no-fee card earning 1.5x, but only if your spending in those categories is high enough. For a freelancer spending $500 per month on business software, advertising, and equipment, the 3x card at a conservative 1-cent-per-point redemption generates about $180 in annual rewards. After the $95 fee, the net gain is $85. The no-fee card at 1.5x on the same $6,000 annual spend generates $90. The fee card wins, but only by $5 in that scenario. The annual fee is also deductible in proportion to business use, which narrows the gap further for high-earning freelancers.

| Card Feature | Tax Season Value | Best For |

|---|---|---|

| Year-End Summary Report | Consolidates all charges by category for Schedule C | All freelancers |

| QuickBooks / CSV Export | Eliminates manual data entry into accounting software | Freelancers using bookkeeping tools |

| Automatic Expense Categories | Pre-sorts charges (travel, office, meals) to match Schedule C lines | High-volume spenders |

| Virtual Card Numbers | Tags recurring software subscriptions for easy identification | SaaS-heavy freelancers |

| Receipt Matching / Upload | Attaches digital receipts to transactions for IRS substantiation | Freelancers with frequent travel or meals |

| No Annual Fee | Keeps the card cost-neutral for lower-spending sole proprietors | Early-stage freelancers |

Using the Card All Year to Make April Painless

Real-time tracking is the whole point. Logging expenses every quarter, rather than reconstructing them in April, means your quarterly estimated tax payments to the IRS are based on accurate numbers, not rough guesses.

One underused application: paying quarterly estimated taxes directly by card through IRS-authorized payment processors like Pay1040 or ACI Payments. These processors charge convenience fees between 1.5% and 1.96% of the payment amount. If your card earns 2x points on all purchases at a value of 1 cent per point, you net a small positive return on the tax payment itself, and the convenience fee is deductible as a business expense. For a $3,000 quarterly payment, the math looks like this: a 1.96% fee equals $58.80 in charges; a 2% rewards earn-back equals $60.00 in value. The net gain is $1.20, and the $58.80 fee is deductible. It’s not a windfall, but it turns an inevitable expense into a mildly positive transaction. If your card earns only 1.5% back, you’d net a $1.80 loss before accounting for the deduction, a legitimate reason to match your card’s reward rate to this strategy before relying on it.

Set a monthly 15-minute calendar block to review your business card statement and add a brief note to any unusual or large charges explaining their business purpose. That habit takes under an hour per year and eliminates the most common deduction documentation gap the IRS flags during correspondence audits.

For broader context on navigating tax season as a self-employed filer, this guide on preparing for tax season early covers quarterly payment schedules and common filing mistakes worth avoiding.

What Happens to Rewards and Points at Tax Time

Most rewards earned through ordinary card spending are treated as purchase rebates by the IRS, not taxable income. This means the cash back, points, or miles you accumulate on your business purchases do not get added to your gross income for the year. The IRS has not issued a formal regulation on this point, but the longstanding administrative position is consistent: rewards tied to spending are rebates on that spending, not compensation.

One Exception Worth Knowing

Signup bonuses received without a minimum spending requirement, pure introductory offers for opening an account, have been treated as taxable income in limited IRS guidance, though enforcement has been inconsistent. In practice, virtually every competitive business card ties its welcome bonus to meeting a spending threshold within the first three months, which brings those rewards back under the rebate treatment. Still, if your card issues a 1099-MISC for a signup bonus, that income is reportable.

When you redeem points toward business expenses, software renewals, office supplies, advertising, the redemption effectively reduces your deductible cost basis. Redeeming 10,000 points toward a $100 software subscription means your deductible expense for that subscription is $0, not $100. This is rarely explained clearly, but it’s the correct treatment. Redeeming toward personal purchases (flights, hotel stays for vacation) avoids this issue entirely.

Common Mistakes That Undo the Tax Benefits

The most damaging mistake is mixing personal charges onto the business card, not occasionally, but habitually. One or two personal charges per year can be prorated without difficulty, but a pattern of mixed use invites the IRS to reclassify the entire card as personal, which eliminates the interest and fee deductions and weakens the substantiation value of the statements.

Documentation Gaps on Large Purchases

The IRS requires more than a charge appearing on a statement. According to IRS guidance on business travel deductions, self-employed individuals should keep well-organized records including receipts and other documents to support deductions for business travel and other expenses reported on Schedule C. For purchases over $75, a receipt plus a brief note explaining the business purpose is the standard the IRS expects. A card statement alone is not always sufficient for large or unusual charges.

Personal guarantees also create a risk that most freelancers overlook: because repayment is tied to your personal credit, late payments on a business card can damage your personal credit score, which in turn affects future borrowing costs and, if you’re carrying any balance, the APR you pay on that card. If you’re already managing personal card debt, the guidance on prioritizing and negotiating credit card debt is worth reviewing before adding another account. The business benefits of a dedicated card are real, but they require the discipline to pay the balance, or at minimum to understand the deductibility rules on any interest you carry.

One more overlooked issue: if you prorate a card that’s used 80% for business and 20% for personal, only 80% of the annual fee and interest are deductible. Most freelancers either claim 100% (incorrect) or 0% (leaving money on the table). The proportional approach is the defensible one, and it requires documenting the split, ideally by keeping a simple log of personal vs. business charges each month. If you’re uncertain how to approach deductions you may have missed in prior years, this overview of free IRS tax help and overlooked credits covers low-cost options for catching up.

The IRS treats credit card rewards earned through ordinary business spending as nontaxable purchase rebates in most circumstances, meaning the points or cash back you accumulate on deductible business expenses do not add to your gross self-employment income for the year.

Building the habit of clean records pays dividends beyond April. Freelancers with organized financials are better positioned to access credit lines, respond to IRS inquiries quickly, and make accurate quarterly estimated payments, all of which reduce stress and cost at every point in the business cycle, not just at filing time. For those exploring how to build income streams that support better financial planning, the micro-freelancing surge article examines how solo workers are structuring diversified revenue.

Frequently Asked Questions

Do freelancers need an LLC or EIN to get a business credit card?

No. Most major issuers approve sole proprietors using only a Social Security Number and personal credit history. You can list your own name as the business name on the application. An EIN is optional and only required if you have employees or operate as a formal entity like an LLC or S-corporation.

Are business credit card rewards taxable income for freelancers?

Generally, no. The IRS treats rewards earned through ordinary spending as nontaxable purchase rebates. The main exception is a signup bonus received without any spending requirement, which some IRS guidance has treated as taxable income, though virtually all competitive business cards tie their welcome offers to a minimum spending threshold, bringing them under the rebate treatment.

Can I deduct the annual fee on a business credit card?

Yes, in proportion to business use. If the card is used exclusively for business, the full annual fee is deductible on Schedule C. If you occasionally use it for personal charges, you can only deduct the percentage that reflects business use, for example, 80% of a $95 fee if 20% of charges were personal.

Is business credit card interest deductible on Schedule C?

When a card is used entirely for business, 100% of the interest paid is deductible as a business expense. Mixed-use cards require prorating the deduction based on the percentage of business charges. Keeping personal charges off the business card entirely is the cleanest approach and preserves the full deduction.

What records does the IRS require to support business credit card deductions?

The IRS requires supporting documents that identify the payee, amount, proof of payment, date, and description of the expense, per IRS guidance on recordkeeping. A card statement satisfies most of these requirements, but for large or unusual charges, attaching the original receipt and a brief note explaining the business purpose provides stronger substantiation.

Can I pay my quarterly estimated taxes with a business credit card?

Yes, through IRS-authorized processors like Pay1040 or ACI Payments. These processors charge convenience fees between roughly 1.5% and 1.96% of the payment amount. That fee is deductible as a business expense. Whether the strategy is net-positive depends on your card’s rewards rate, if your card earns less than the convenience fee percentage, you’ll lose a small amount on the transaction before accounting for the deduction.

How do business credit cards help with Schedule C preparation?

Cards with automatic expense categorization and downloadable year-end summaries map directly to Schedule C line items such as advertising, office expense, and travel. Exporting transactions in CSV or QuickBooks-compatible formats eliminates most manual data entry. Tools like Keeper Tax and QuickBooks Self-Employed can pull card data directly and flag potential write-offs, reducing preparation time significantly compared to sorting a mixed personal account.

Sources

- Internal Revenue Service, What Kind of Records Should I Keep?

- Internal Revenue Service, Recordkeeping for Small Businesses and Self-Employed

- Internal Revenue Service, Self-Employment Tax (Social Security and Medicare Taxes)

- Internal Revenue Service, Understanding Business Travel Deductions

- Board of Governors of the Federal Reserve System, Consumer & Community Context (March 2025)

- National Bureau of Economic Research, Working Paper No. 33618 (2025)