Fact-checked by the MyFinancial101 editorial team

Quick Answer

To save money with smarter discount shopping strategies in 2026, time purchases around real sale cycles, use price-history tools to verify genuine deals, stack loyalty rewards with digital coupons, and shift spending toward off-price and resale channels. Consumers who combine these methods save an average of $395.81 per year on digital coupons alone, with additional savings from loyalty programs and purchase timing on top.

Most people approach discount shopping the wrong way: they clip coupons, wait for sales, and assume they are saving money. The reality in 2026 is more complicated. Discount shopping strategies have evolved far beyond printable coupons, and retailers have become sophisticated enough that a “40% off” sticker is often not what it appears. According to Capital One Shopping’s 2025 coupon research, 169.2 million American consumers redeemed digital coupons last year alone, yet most still leave significant savings on the table by relying on a single method.

Price sensitivity among shoppers is not easing. Persistent inflation, tariff-driven cost pressures, and a retail environment full of manufactured urgency have made 2026 a uniquely difficult year for buyers. At the same time, discount chains are aggressively expanding, resale platforms have matured, and browser-based price tools have gotten smarter. The gap between savvy shoppers and average ones is widening.

This guide is for anyone who wants to stop reacting to retailer promotions and start shopping on their own terms. By the end, you will know how to verify real deals, choose the right loyalty programs, and redirect those savings toward concrete financial goals.

Key Takeaways

- The average consumer saves $395.81 per year using digital coupons, according to Capital One Shopping’s 2025 data, but stacking strategies can push that number significantly higher.

- 70% of shoppers engaged in three or more deal-seeking behaviors during the 2025 holiday season, per Deloitte via aggregated Black Friday statistics, confirming multi-channel discount tactics are now the norm.

- Online coupon users receive an average discount of 17.2% per purchase, according to Capital One Shopping citing a CouponFollow study.

- Store brands typically cost 15-25% less than name brands with comparable quality, according to Consumer Reports.

- Discount retailers are planning to open over 1,200 new stores in 2026, the most aggressive expansion in decades, creating fresh geographic access to off-price goods.

- 63% of consumers plan to shop at discount department stores during the holidays, per ICSC’s 2024 holiday survey, signaling that discount channels have become mainstream, not a last resort.

In This Guide

- Why Coupon Clipping Alone No Longer Cuts It

- How Do I Time My Purchases to Get the Lowest Price?

- Which Browser Tools and Price Trackers Actually Save Money?

- Which Loyalty Programs Are Worth Joining?

- How Do I Use Off-Price, Resale, and Salvage Channels to Save More?

- What Behavioral Changes Stop Me From Overpaying?

- Frequently Asked Questions

Step 1: Why Coupon Clipping Alone No Longer Cuts It

Traditional coupon clipping has a ceiling problem: it only saves you money when retailers decide to issue coupons, on products they want to move. In 2026, that ceiling is lower than most shoppers realize. Paper coupons have largely given way to app-exclusive digital offers, which means your Sunday newspaper circular may not reflect where the actual savings live. More critically, retailers have refined a tactic called “high-low pricing,” where regular prices are artificially elevated so that coupons appear to deliver big savings even when the net price is still above a competitor’s everyday price.

The Real Problem With Coupon-Only Thinking

A coupon is a retailer’s tool first and a consumer’s tool second. It directs spending toward specific products, often brand-name items with higher margins, at times the retailer controls. Compare that with the strategies in this guide, which put timing, channel selection, and verification tools in your hands. The most effective coupon users beat inflation by combining coupons with other tactics, not by relying on them alone.

What Digital-Only Deals Mean for Your Wallet

Retailers like Target, Kroger, and Walgreens now gate their best discounts inside proprietary apps, requiring you to opt into data tracking in exchange for savings. This is worth knowing upfront. The FTC advises shoppers to search for coupon codes and discounts and review total costs including shipping before purchasing, and that advice holds whether the coupon is paper or digital. The shift also means that consolidating your shopping into a smaller number of retailers with strong app ecosystems will outperform scattering purchases across dozens of stores for marginal coupon wins.

Many retailers raise baseline prices before issuing digital coupons. A “30% off” app deal may bring the item back to the price it held three weeks earlier. Price history tools, covered in Step 3, are your primary defense against this.

Step 2: How Do I Time My Purchases to Get the Lowest Price?

Buying at the right moment is more reliable than hunting for coupons, because sale cycles repeat with near-calendar precision. Major retail events like Amazon Prime Day (typically mid-July) and Black Friday are well-known, but the deeper savings often come from less-publicized seasonal patterns that most shoppers miss entirely.

Category-by-Category Timing Map

Electronics hit cyclical lows in January (post-holiday clearance), late summer (back-to-school transitions), and immediately after new model launches. Apparel typically bottoms out in February, late June, and early September, when seasonal inventory turns. Large appliances are cheapest in September and October as new models ship. Furniture and mattresses drop most sharply during Memorial Day and Labor Day weekends. Grocery staples follow a six-to-eight-week coupon cycle that, once tracked, lets you buy at the lowest price and stock up before the cycle resets.

What to Watch Out For

Perceived urgency is a retailer’s primary weapon. Flash sales, “only 3 left” countdowns, and limited-time price drops are calibrated to override deliberate decision-making. Consumer Reports notes that price history tools reveal many Prime Day deals match or exceed prices tracked over prior months, meaning the “event” framing creates urgency that the discount itself does not always justify. The fix is simple: check price history before you buy, every time.

70% of consumers engaged in three or more deal-seeking activities during the 2025 holiday season, according to Deloitte’s aggregated Black Friday data. Multi-channel deal-seeking is now standard behavior, not an edge.

Step 3: Which Browser Tools and Price Trackers Actually Save Money?

Price tracking tools do one thing exceptionally well: they strip the theater out of a “sale.” Before any major purchase, checking price history takes less than 60 seconds and can reveal whether a deal is real or manufactured. The payoff is disproportionate to the effort.

The Tools Worth Installing

CamelCamelCamel tracks Amazon price history going back years and sends email alerts when an item drops to your target price. Keepa offers similar Amazon tracking with more granular data, including third-party seller prices. For broader web comparison, Google Shopping pulls prices across multiple retailers in real time, making it useful for non-Amazon purchases. The browser extension Honey (now part of PayPal) automatically tests coupon codes at checkout and tracks price drops on saved items, though its primary value is coupon-testing rather than deep historical analysis.

As Consumer Reports recommends, you should track prices with tools like Keepa or CamelCamelCamel to verify if a deal is genuine, use retailer apps for early access to Lightning Deals, and compare prices across stores rather than assuming sale prices are the lowest. That last point is the one most people skip.

Setting Personalized Alerts

Generic “deal of the day” notifications are noise. Set price drop alerts only for items already on your planned purchase list, at a specific target price you have decided in advance. This inverts the dynamic: instead of retailers pushing deals to you, you are pulling them only when conditions you set are met. CamelCamelCamel and Keepa both support this directly.

Before any purchase over $50, run the item through CamelCamelCamel first. If the current price is within 5% of the 90-day low, buy. If it is near a 90-day high, wait or check a competing retailer. This single habit can save hundreds per year with minimal time investment.

| Tool | Best For | Covers | Price Alert Feature |

|---|---|---|---|

| CamelCamelCamel | Amazon price history | Amazon only | Yes, email alerts at target price |

| Keepa | Granular Amazon data + 3rd-party sellers | Amazon only | Yes, browser + app notifications |

| Google Shopping | Cross-retailer price comparison | Broad web coverage | Yes, price drop tracking on saved items |

| Honey (PayPal) | Auto-applying coupon codes | 1,000+ retailers | Yes, Droplist feature |

| Rakuten | Cash-back on purchases | 3,500+ retailers | No dedicated price alerts |

Cash-back extensions like Rakuten layer on top of price tracking tools. A 17.2% average discount from online coupons, per Capital One Shopping’s CouponFollow data, stacks with a cash-back rebate to push the effective savings higher. Used together, these tools represent the practical core of any serious discount shopping strategy.

Step 4: Which Loyalty Programs Are Worth Joining?

Free loyalty programs at retailers you already use regularly are almost always worth it. Paid memberships require a harder look at the numbers.

Amazon Prime costs $139 per year as of early 2026. It breaks even quickly for households ordering frequently enough to value free two-day shipping, but the streaming, pharmacy, and grocery benefits vary widely in value. Costco‘s Gold Star membership ($65/year) returns value primarily through lower per-unit prices on staples, which Consumer Reports notes can also be achieved through store brands that cost 15-25% less than name brands. Free-tier programs from Target (Circle), Kroger (Plus Card), and CVS (ExtraCare) require no spending commitment and deliver genuine discounts for existing shopping patterns.

The trap to avoid: buying more than you need to hit a points threshold or unlock a reward tier. If the program is changing your purchase behavior rather than rewarding existing spending, it is working against your budget, not for it. If you are managing credit card debt alongside your savings goals, pairing loyalty strategies with a plan to prioritize and negotiate your credit card balances will do more for your financial position than any rewards point accumulation.

63% of consumers plan to shop at discount department stores during the holiday season, per ICSC’s 2024 survey. Discount retail is no longer a niche channel; it has become a primary destination for mainstream shoppers.

Step 5: How Do I Use Off-Price, Resale, and Salvage Channels to Save More?

Off-price and resale are the fastest-growing savings channels in 2026, and the product quality gap between them and traditional retail has closed dramatically. If you are still treating TJ Maxx, ThredUp, or Facebook Marketplace as fallback options, you are leaving consistent savings on the table.

The Off-Price Expansion You Should Know About

Discount retailers, including Five Below, Dollar Tree, Burlington, and the TJX Companies (TJ Maxx, Marshalls, HomeGoods), are collectively opening over 1,200 new stores in 2026. This expansion is the most aggressive in decades and is driven directly by sustained price sensitivity. More locations mean more inventory turnover, which generally means more fresh product arriving at reduced prices. Identifying recently opened stores in your area is worth the effort: new locations often run introductory promotions and carry dense inventory before the best items are picked over.

Resale Platforms for Durable Goods

Platforms like eBay, Poshmark, ThredUp, and Mercari have moved well past the perception that resale means worn-out goods. A notable shift in 2025 and into 2026: the popularity of GLP-1 weight-loss medications has driven a surge in clothing donations as buyers change sizes, creating unusually strong resale inventory across a wide range of sizes that previously had thin secondary market supply. 56% of consumers reported increasing their purchases of discounted fashion in the past year, with 22% noting a substantial rise in off-price buying specifically. For durable goods like tools, furniture, and appliances, the Facebook Marketplace and OfferUp remain the most liquid local options with no seller fees for buyers.

Food salvage deserves mention here. Apps like Too Good To Go connect buyers with restaurants and retailers selling surplus food at deep discounts, typically 50-70% off, before it goes to waste. It is not a primary grocery strategy, but as a supplement for prepared foods and bakery items, it is genuinely useful and carries no subscription cost.

What to Watch Out For

Resale has one honest limitation: you cannot always buy on your timeline. If you need a specific item in a specific size by a specific date, waiting for resale may not be realistic. The strategy works best for non-urgent, recurring purchases, seasonal clothing, and home goods where you have lead time to search. For time-sensitive needs, off-price retail chains are the more reliable option.

Step 6: What Behavioral Changes Stop Me From Overpaying?

Every discount tool in this guide can be neutralized by one bad habit: buying things you did not plan to buy. Behavioral discipline is the foundation that makes the other five steps work.

The 24-Hour Cart Rule

Before completing any unplanned purchase over $30, add it to your cart and wait 24 hours. This single rule removes a significant share of impulse spending, particularly on e-commerce platforms designed to shorten the decision cycle. In practice, the urgency fades on most items you did not specifically go looking for. Those that still seem worth buying after a day are more likely genuine needs.

Grocery-Specific Tactics That Reduce Bills 20-30%

Meal planning combined with a defined shopping list before entering the store reduces grocery spending by 20-30%, according to USDA research on grocery shopping behavior. The mechanism is straightforward: a list caps what enters the cart and prevents the category drift that inflates totals. “Shop your pantry” routines, where you inventory what you already have before writing a list, reduce duplicate purchases and trim the list further. Pairing your list with the store’s weekly circular before you shop, rather than after you arrive, lets you substitute planned items for discounted equivalents without abandoning the structure. For more on this, the seasonal grocery cost management strategies on this blog go deeper into category-specific substitutions.

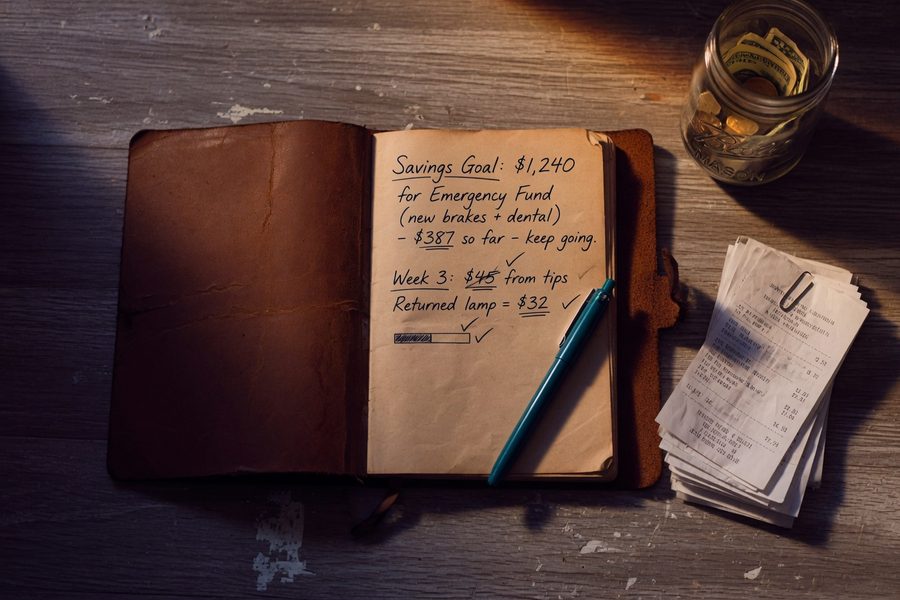

Connecting Savings to a Specific Goal

The research on behavior change is consistent: savings behavior becomes more durable when it is tied to a concrete goal rather than a vague intention to “spend less.” If your $395 in annual coupon savings goes into a general checking account, it dissolves. If it flows automatically into an emergency fund or a dedicated debt payoff account, it compounds. Consider reading about how to start investing with zero experience if your savings goal is building long-term wealth rather than just reducing debt.

Run the arithmetic on your grocery habit once. If you spend $600 per month on groceries and reduce that by 25% through planning and list discipline, that is $150 per month, or $1,800 per year. That figure, added to the average $395.81 in digital coupon savings, puts your combined annual savings potential near $2,200 without buying a single item you did not need.

Frequently Asked Questions

Are discount shopping strategies actually worth the time, or does it take more effort than it saves?

The high-effort tactics, like extreme couponing or driving to multiple stores, often are not worth the time. The highest-return habits, like checking price history before purchases, using one or two loyalty apps for stores you already shop, and meal planning before grocery trips, take under 30 minutes per week and produce measurable savings. The average digital coupon user saves $395.81 per year, and that is before layering in timing, resale, and behavioral tactics.

How do I know if a sale price is actually a good deal and not inflated?

Check price history before buying. CamelCamelCamel and Keepa both show Amazon’s historical pricing going back months or years. For non-Amazon retailers, Google Shopping’s price tracking covers a broad range of sites. Consumer Reports confirms that many sale prices during high-profile events match or exceed prices tracked over prior months, so the habit of verifying before buying is not paranoid: it is practical.

Should I pay for Amazon Prime or Costco, or are free loyalty programs enough?

Free programs are sufficient for most shoppers who buy infrequently online or who do not live near a Costco. Amazon Prime pays off for households placing six or more orders per month, where free shipping alone covers the $139 annual cost. Costco’s $65/year membership makes financial sense primarily for families buying bulk staples regularly. If neither describes your situation, the free-tier programs from Target Circle, Kroger, and similar retailers deliver real savings at no cost or commitment.

What is the best way to save money on groceries in 2026?

Meal planning with a written list before shopping reduces grocery bills by 20-30% per USDA data, making it the single highest-impact grocery tactic available. Layer in store-brand substitutions (15-25% cheaper per Consumer Reports), digital loyalty coupons from the store’s own app, and a shop-your-pantry routine to avoid duplicate purchases. The combination regularly outperforms any individual tactic used alone.

How do I use resale apps without getting ripped off or buying poor-quality items?

Stick to platforms with buyer protection policies: eBay’s Money Back Guarantee and Poshmark’s authentication service for luxury goods both cover disputes. For clothing, filter by condition (“like new” or “new with tags”) and check the seller’s rating and return history. For durable goods on Facebook Marketplace, inspect in person before paying and pay in a safe public location. Avoiding wire transfers or payment apps without buyer protection removes most of the financial risk.

Can I combine digital coupons, cash-back apps, and loyalty points on the same purchase?

Yes, and stacking these is how meaningful savings accumulate. A typical stack might look like: load a digital coupon through the store’s app, pay with a cash-back credit card, and activate a Rakuten rebate for the same retailer. Each layer applies independently. The only common restriction is that some stores limit one manufacturer coupon per transaction, but retailer digital coupons and cash-back rebates are usually not subject to that constraint. Check the store’s coupon policy before your first stacked purchase.

Is it worth shopping at discount chains like TJ Maxx instead of buying on sale at a full-price retailer?

For apparel, home goods, and branded basics, off-price chains typically deliver lower net prices than waiting for sales at full-price retailers, with no need to track promotions. TJX Companies, Burlington, and similar chains source overstock and off-season merchandise at wholesale levels that even steep full-price sales rarely match. The tradeoff is limited selection: you cannot always find a specific brand, size, or color. For flexible shoppers with lead time, off-price is almost always the better channel.

How do I stop impulse buying even when I know a deal is good?

Use the 24-hour cart rule: add the item to your cart and revisit it the next day. Studies on purchasing behavior consistently show that most urgency around a “limited” deal fades within hours. If the item is still discounted and still wanted after 24 hours, buy it. If the deal has expired and you still want it, the item likely recurs at similar prices, so a price alert through Keepa or Google Shopping will catch the next opportunity without the rushed decision.

How can I tie my savings from discounts directly to paying off debt?

Set up an automatic transfer from checking to a dedicated debt payoff account each time you would have spent the money on a planned purchase at full price. Alternatively, treat each month’s grocery savings as a fixed additional payment toward your highest-interest balance. If credit card debt is the priority, the strategy of negotiating your credit card APR downward can amplify the impact of every extra dollar you direct toward the balance. The key is routing the savings deliberately rather than letting them absorb into general spending.