Fact-checked by the MyFinancial101 editorial team

Quick Answer

Retirees can make $2,500 a month work by auditing every income source, cutting housing costs through downsizing or relocation, and stacking senior discounts with benefits programs. The key spending targets: housing under $900, healthcare under $400, and groceries under $350. Most retirees who follow this framework find $200–$400/month in recoverable spending within 60 days.

Most financial advice treats $2,500 a month as a budget too tight to work with. The data says otherwise. Smart spending on a fixed income is less about sacrifice and more about sequencing the right moves, starting with housing, then healthcare, then the smaller categories that quietly drain accounts. According to The Motley Fool’s reporting on SSA data, the average Social Security benefit for retired workers was $2,013 per month, meaning millions of retirees are already living close to this number, and many are doing it well.

The challenge has sharpened recently. Schroders’ 2025 U.S. Retirement Survey found that 45% of retirees report their expenses in retirement are higher than expected, a figure that reflects three years of compounding inflation across groceries, utilities, and healthcare premiums. The gap between expectation and reality is real. But so is the toolkit for closing it.

This guide is for retirees, near-retirees, and anyone supporting an older family member who needs a practical, step-by-step plan, not vague reassurance. By the end, you will know exactly which levers move the needle on $2,500 a month and which conventional wisdom to ignore.

Key Takeaways

- The average retired worker collects $2,013/month from Social Security, per SSA data reported by The Motley Fool, making supplemental strategies essential for reaching a livable $2,500 total.

- Social Security benefits have lost an estimated 20% of their purchasing power between 2010 and 2024, according to the Senior Citizens League via Kiplinger, which explains why the same dollar amount buys less every year.

- U.S. retiree households spent an average of $61,432 in 2024 (roughly $5,119/month), per BLS Consumer Expenditure Survey data reported by Vision Retirement, nearly double what a $2,500 budget allows, which means deliberate trade-offs are unavoidable.

- Medicare Part B alone costs $185/month in 2025, up from $174.70 in 2024, per the Centers for Medicare & Medicaid Services, a line item that tends to grow faster than COLA adjustments.

- A 65-year-old retiring in 2025 should expect $172,500 in total healthcare costs throughout retirement, according to Fidelity’s 2025 Retiree Health Care Cost Estimate, averaging roughly $480/month over an 18-year retirement horizon.

- Cutting takeout by just 3–4 meals per month saves the average retiree over $1,000 annually, per AARP’s 2026 budgeting guidance, one of the highest-return behavioral changes with zero infrastructure required.

In This Guide

- Step 1: What $2,500 a Month Actually Covers for Retirees Today

- Step 2: How to Audit Your True Monthly Income and Hidden Costs

- Step 3: Which Housing Moves Free Up the Biggest Chunk of Your Budget

- Step 4: Grocery, Dining, and Everyday Spending Hacks That Add Up

- Step 5: How to Keep Healthcare From Eating Your Fixed Income

- Frequently Asked Questions

Step 1: What $2,500 a Month Actually Covers for Retirees Today

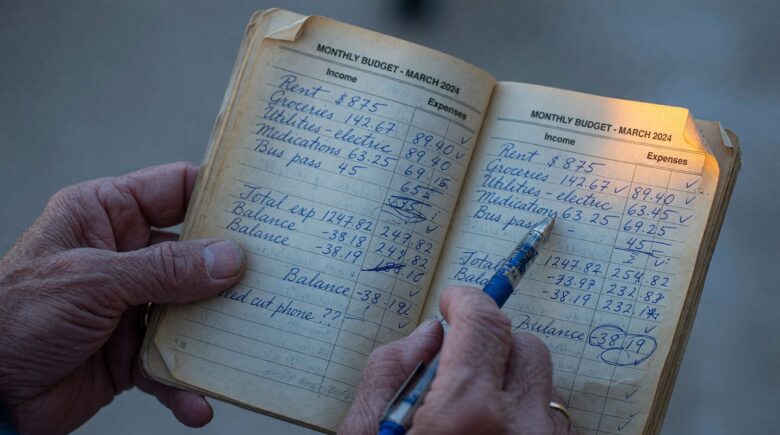

$2,500 a month is tight by national average standards, but it is livable with the right allocation. The most defensible framework puts housing at or below $900, healthcare (including premiums, copays, and prescriptions) at $400, groceries at $300–$350, transportation at $200, and utilities at $150–$200. That leaves roughly $450–$550 for personal care, entertainment, and an emergency fund contribution.

Where the Money Comes From

Most retirees on this budget blend two or three income sources. Social Security is usually the anchor: the average retired worker received $2,013/month as of late 2025. The gap between that number and $2,500 typically gets filled by a small pension, part-time work, investment withdrawals, or a combination of benefits programs. The National Council on Aging specifically advises fixed-income seniors to inventory every income stream before building a budget, because missing even one source distorts the entire plan.

The Inflation Problem in Plain Numbers

The BLS Consumer Expenditure Survey shows the average retiree household spent $61,432 in 2024, a 2.2% increase from the prior year. That is roughly $5,119 per month, more than double a $2,500 budget. The gap is not a reason to panic; it is a reason to prioritize. Retirees who successfully manage $2,500/month are not spending on the full average basket. They have made deliberate cuts, and those cuts are specific, not random.

Social Security benefits have lost an estimated 20% of purchasing power between 2010 and 2024, according to the Senior Citizens League. That erosion is why a COLA raise rarely feels like a raise, prices outpace the adjustment most years.

Step 2: How to Audit Your True Monthly Income and Hidden Costs

Before cutting anything, you need an accurate number, and most retirees are working with an inaccurate one. The single most common error: underestimating irregular expenses by treating the monthly budget as if every month looks the same. Property taxes, car registration, annual insurance renewals, and medical deductibles all hit in lumps.

How to Do This

Start with a 90-day bank and credit card statement review rather than building a budget from memory. Pull every transaction, categorize it, and look for the “invisible” lines: Medigap or Medicare Advantage premiums auto-drafted monthly, streaming subscriptions you forgot about, and pharmacy copays that vary quarter to quarter. The U.S. Department of Labor’s retirement planning guide provides worksheets specifically designed to help retirees compare projected monthly income against actual expenses over a multi-decade horizon, a useful frame even for those already retired.

For tracking tools, YNAB (You Need a Budget) and Tiller Money both support fixed-income budgeting and allow category-level tracking down to individual subscriptions. Both offer free trials. If app-based tools feel like friction, a printed spreadsheet updated weekly works just as well, consistency matters more than the platform.

What to Watch Out For

Annual expenses that get mentally rounded down are the biggest leak. A $1,200 annual property tax bill is really a $100/month obligation, but it rarely shows up in retirees’ mental monthly tallies. Same for car registration, home maintenance reserves, and dental work not covered by Medicare. The AARP guidance on inflation-adjusted retirement expenses recommends building a 12-month rolling calendar of every predictable non-monthly expense, then dividing by 12 and treating that total as a fixed monthly line item.

If you receive a tax refund, resist treating it as a windfall. Redeposit it directly into a sinking fund for known annual expenses. This single habit eliminates most mid-year budget crises for retirees on fixed incomes, and keeps those one-time payments from quietly funding lifestyle creep.

Retirees who need help identifying benefits they may be missing can check the updated 2026 federal poverty guidelines, which determine eligibility for dozens of assistance programs that many fixed-income seniors qualify for but never claim.

Step 3: Which Housing Moves Free Up the Biggest Chunk of Your Budget

Housing is the single largest expense category for most retirees, and therefore the highest-leverage place to make a change. Cutting housing costs by $300/month adds $3,600 a year back to the budget. No other category comes close to that magnitude.

Downsizing and Geographic Arbitrage

Retirees moving from high-cost Northeast or West Coast metros to no-income-tax states like Nevada, Tennessee, or Florida routinely cut their effective housing and tax burden by 30–50%. Tennessee, for example, has no state income tax and median rent in cities like Knoxville running well below the national average. Nevada’s property taxes are among the lowest in the country. These are not fringe moves, they are increasingly common among retirees on fixed incomes who prioritize purchasing power over proximity to their previous location.

For those who own, the rent-versus-sell calculation deserves real attention. Selling a paid-off home worth $300,000 and renting at $800/month generates immediate liquidity while eliminating property tax, maintenance, and homeowner’s insurance. A reverse mortgage or HELOC keeps you in the home but introduces interest costs and long-term risk to equity, often a worse deal for retirees who plan to relocate within five years anyway. Downsizing first is the cleaner move for most people; tapping equity instruments works better when staying put is the firm plan.

Senior-Specific Housing Options

55+ communities often carry lower HOA fees than general-market condos and bundle amenities that would otherwise be paid separately. Shared housing arrangements, sometimes called “elder co-housing”, are growing in cities like Portland, Denver, and Raleigh, and can cut housing costs by 40% or more while reducing isolation. Neither option suits everyone, but both are worth pricing before assuming the current housing situation is fixed.

Relocating purely for cost savings without accounting for healthcare access is a common mistake. Some lower-cost states have fewer in-network Medicare providers, which can push out-of-pocket medical costs high enough to offset the housing savings. Check Medicare plan networks in any target state before committing.

| Housing Strategy | Estimated Monthly Cost | Key Trade-Off |

|---|---|---|

| Stay in current home (with mortgage) | $1,100–$1,400 | Familiarity; highest fixed cost on $2,500 budget |

| Stay in current home (paid off) | $300–$600 (taxes, insurance, maintenance) | Lowest cash outlay; maintenance risk increases with age |

| Downsize locally | $700–$950 rent or reduced mortgage | Frees equity; may require moving twice if relocating later |

| Relocate to lower-cost state (rent) | $650–$850 | Maximum savings; disrupts social network and healthcare |

| 55+ community | $800–$1,100 including HOA | Bundled amenities; geographic options more limited |

| Shared housing / co-housing | $450–$700 | Lowest cost; requires compatible housemate and clear agreements |

Step 4: Grocery, Dining, and Everyday Spending Hacks That Add Up

Groceries are controllable in a way that rent and Medicare premiums are not. That makes them worth optimizing, but not obsessing over to the exclusion of bigger-ticket categories.

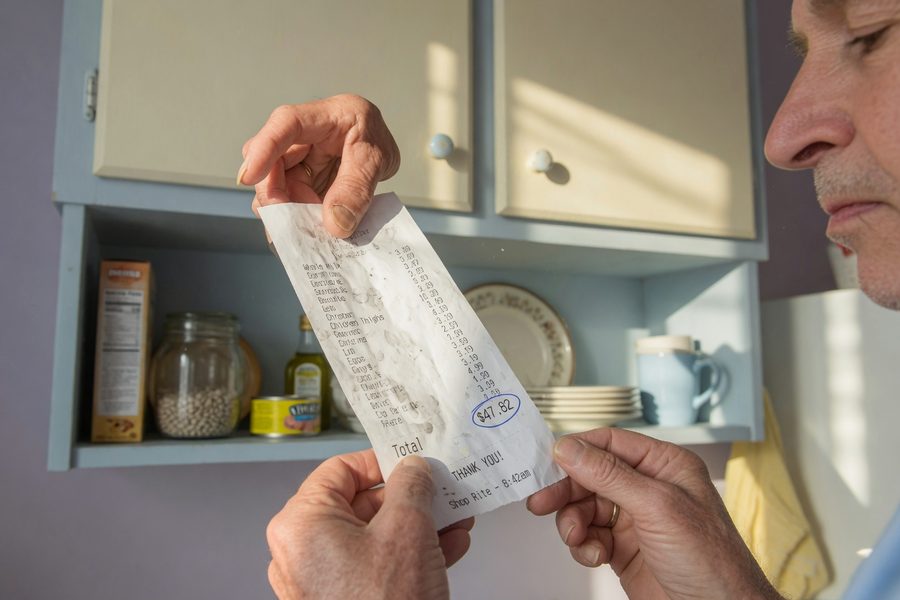

Keeping a household grocery budget at or under $300–$350/month is achievable for one or two people through a combination of meal planning, store-brand substitution, and strategic use of senior discount days. Most major grocery chains, Kroger, Albertsons, and Food Lion among them, offer 5–10% discounts on specific days for shoppers aged 60 or older. Stacking those discounts with store loyalty apps and manufacturer coupons is where the cumulative savings become meaningful. As detailed in our guide on how coupon stackers are beating inflation, the discipline of layering discounts across a single shopping trip can reduce a grocery bill by 15–25%.

Dining out is where the budget most often breaks quietly. AARP’s 2026 guidance is direct: cutting takeout by 3–4 meals per month saves over $1,000 annually. That number is not surprising when the average restaurant meal runs $15–$25 per person versus $3–$5 for a home-cooked equivalent. Occasional dining out is fine and sustainable on $2,500. Regular takeout is not.

Many public libraries now offer free access to streaming services, museum passes, and digital magazines, resources that can replace $50–$100 in monthly subscriptions. Our breakdown of what your library gives you for free covers exactly what to ask for at the circulation desk.

Step 5: How to Keep Healthcare From Eating Your Fixed Income

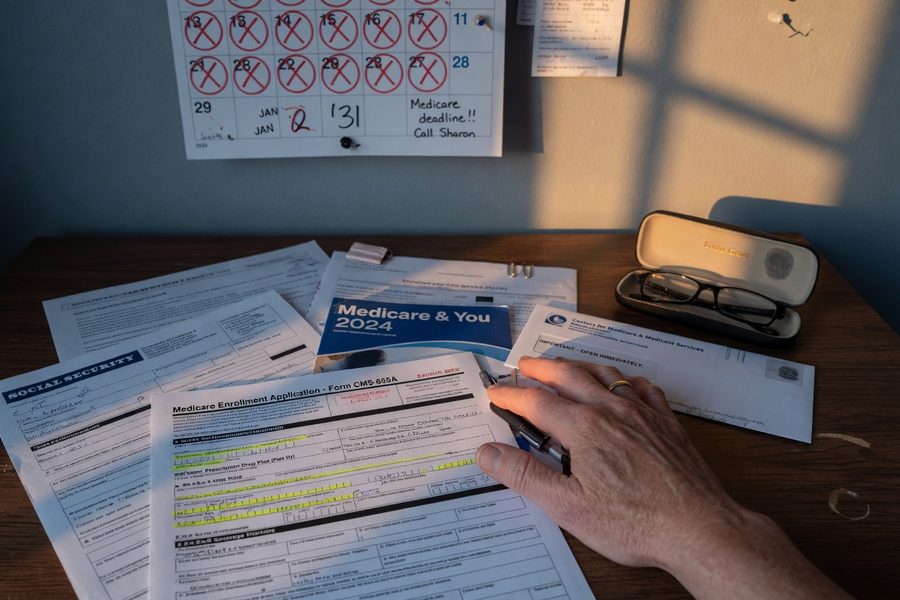

Healthcare is the spending category most likely to derail a $2,500 budget, and the one where smart planning returns the most dollars. The numbers are stark: Fidelity’s 2025 Retiree Health Care Cost Estimate puts total lifetime healthcare spending for a 65-year-old at $172,500, a 4%+ increase over the 2024 estimate. Averaged over an 18-year retirement, that is roughly $480 per month. Add the $185/month Medicare Part B premium for 2025 (up from $174.70 in 2024, per the Centers for Medicare & Medicaid Services), and healthcare quickly consumes 25–30% of a $2,500 budget before a single copay or prescription.

Worked Example: Controlling the Healthcare Line

Consider a retiree with Original Medicare (Parts A and B) plus a Part D drug plan. Monthly fixed costs: $185 (Part B) + $35 (Part D average) = $220/month before any services. Adding a Medigap Plan G supplement at approximately $120–$150/month raises the premium total to $340–$370 but eliminates most out-of-pocket exposure for covered services. Compare that to a Medicare Advantage plan at $0 premium but with copays of $20–$50 per specialist visit and potential network restrictions. For a healthy retiree with 3–4 doctor visits per year, Advantage often wins on cost. For someone managing a chronic condition with frequent specialist care, Medigap’s predictability is worth the premium gap. The decision is condition-specific, not universally obvious.

Prescription Strategies That Cut Costs Immediately

Mail-order pharmacies (available through most Part D plans) cut 90-day supply costs by 20–30% compared to retail 30-day fills. Patient assistance programs run by manufacturers like AstraZeneca, Pfizer, and Novo Nordisk provide name-brand medications at no or reduced cost for income-qualifying patients. GoodRx and Mark Cuban’s Cost Plus Drugs platform sometimes price generic medications below even the Part D copay, meaning it is worth price-checking outside your insurance before filling at the counter.

What to Watch Out For

The Medicare Annual Enrollment Period (October 15 – December 7 each year) is the one window to switch plans without penalty. Missing it means being locked into the current plan for another full year. Set a calendar reminder. Also note that free preventive health screenings are covered at $0 under Medicare, skipping them is a false economy that leads to larger medical bills later.

Retirees who are also managing utility costs alongside healthcare can explore the LIHEAP assistance program, which helps fixed-income households offset heating and cooling bills and is often available to the same income tiers that qualify for Medicare Savings Programs.

The Medicare Extra Help program (also called the Low Income Subsidy) reduces Part D drug costs dramatically for enrollees below roughly 150% of the federal poverty level. In 2026, that threshold sits around $22,000 for a single person. If your income is near that line, apply through the Social Security Administration, approval is retroactive to the application month.

Frequently Asked Questions

Can a single person realistically live on $2,500 a month in retirement in 2026?

Yes, but geography matters more than income level. A single retiree in Knoxville, Tennessee or Albuquerque, New Mexico can cover housing, healthcare, food, and transportation on $2,500 with room for savings. The same budget in San Francisco, Boston, or New York City requires significant trade-offs that most people are unwilling to make long-term. The National Council on Aging recommends pairing a realistic budget with a full benefits audit, many single retirees qualify for programs that effectively add $100–$400 in purchasing power per month.

What government benefits can retirees on fixed incomes claim in 2026?

The most commonly missed programs are Medicare Savings Programs (which cover Part B premiums for low-income enrollees), Medicare Extra Help for drug costs, SNAP food benefits, and LIHEAP for utility assistance. Eligibility for each is tied to the federal poverty guidelines, which were updated in early 2026. A retiree living on $2,500/month may qualify for one or more of these depending on household size. The easiest starting point is the NCOA’s BenefitsCheckUp tool at benefitscheckup.org, which screens for over 2,500 programs simultaneously.

Is it better to rent or own a home on a fixed income?

Owning a paid-off home is the cheapest option on paper, but it carries hidden costs that compound with age: maintenance, repairs, property taxes, and homeowner’s insurance. Renting removes those variables but exposes you to annual rent increases. The right answer depends on your home’s equity, your health, and your willingness to relocate. A retiree with significant equity in a high-cost area is often better off selling, investing the proceeds, and renting in a lower-cost market, the rental income on invested equity frequently exceeds the savings from staying put.

How can I reduce Medicare costs beyond just picking the cheapest plan?

The biggest levers beyond plan selection are Extra Help (for Part D), Medicare Savings Programs (for Part B premiums), and using mail-order pharmacy for 90-day supplies. Every Medicare plan covers an annual wellness visit at no cost, use it to get referrals, update prescriptions, and identify preventive services that avoid larger future bills. The CMS fact sheet on 2025 Medicare premiums outlines exactly what is covered under each part, which helps identify where out-of-pocket exposure actually lives in your specific plan.

Should I use a reverse mortgage or HELOC to stretch my retirement budget?

A reverse mortgage works best for retirees who plan to age in place permanently and have substantial home equity but limited liquid assets. It carries fees, interest that compounds over time, and eventual repayment obligations that reduce the estate. A HELOC is cheaper to initiate but requires monthly interest payments, which can strain a fixed income if the draw is large. Neither is inherently bad, but both are inferior to downsizing if relocation is even a possibility within five years. Use home equity instruments as a last resort, not a first strategy.

What apps or tools actually help retirees track a fixed-income budget?

YNAB (You Need a Budget) and Tiller Money are the strongest options for retirees who want category-level visibility without complex investment tracking. Both sync to bank accounts and flag irregular spending patterns. For those who prefer no apps, a printed 12-month cash flow calendar, one column per month, each expected expense listed by due date, catches the annual lumps that derail monthly budgets. The method matters less than the consistency; daily or weekly review beats monthly reconciliation for fixed-income households.

How do I stretch a grocery budget to under $350 per month for two people?

Meal planning before shopping, buying proteins in bulk and freezing portions, and substituting store-brand staples for name brands covers most of the gap. Stack those habits with senior discount shopping days (typically Tuesday or Wednesday at major chains) and digital coupons from the store’s loyalty app. For two people eating primarily at home, $300–$350 is achievable; it requires a weekly plan and a firm list, but not extreme restriction. Reducing restaurant meals to once or twice a week, rather than several times, is the behavioral shift with the highest dollar return, as AARP’s 2026 guidance confirms.

Sources

- The Motley Fool, Average Social Security Benefit for Retirees (December 2025)

- Vision Retirement, Biggest Retiree Expenses (BLS Consumer Expenditure Survey, 2025)

- Centers for Medicare & Medicaid Services, 2025 Medicare Part B Premiums and Deductibles

- Fidelity Investments, 2025 Retiree Health Care Cost Estimate

- Kiplinger, How Inflation Is Impacting Retirees (Senior Citizens League Data, 2025)

- Schroders, 2025 U.S. Retirement Survey: Inflation Taking Toll on Retirees

- National Council on Aging, What Does Living on a Fixed Income Mean?

- AARP, Inflation-Adjusted Living Expenses in Retirement

- U.S. Department of Labor, Taking the Mystery Out of Retirement Planning

- MyFinancial101, How LIHEAP Can Help With Rising Utility Costs

- MyFinancial101, Rising Poverty Guidelines in 2026: Who Benefits Now?