Fact-checked by the MyFinancial101 editorial team

Quick Answer

Required minimum distributions in 2026 apply to anyone born in 1951–1959 who turned 73 by year-end and has a traditional IRA, 401(k), or similar pre-tax account. Calculate your RMD by dividing your December 31, 2025 account balance by your IRS Uniform Lifetime Table factor. Miss the deadline and you face a 25% excise tax on the shortfall, reduced from the old 50% penalty under SECURE 2.0.

Required minimum distributions in 2026 force millions of retirees to withdraw a set amount from their pre-tax retirement accounts each year, whether they need the money or not. The SECURE 2.0 Act, signed into law in December 2022, reshuffled nearly every aspect of these rules: the starting age, the penalty structure, and which accounts are even subject to the mandate. According to the IRS’s official RMD guidance, most retirees must now begin withdrawals at age 73, with the age rising to 75 for those born in 1960 or later, a change that adds years of potential tax planning time for younger cohorts but creates confusion about who exactly owes what in any given calendar year.

This matters in 2026 specifically because a large group of Americans born in 1953, the first full birth-year cohort solidly in the new age-73 regime, will hit their required beginning date for the very first time. Meanwhile, those who delayed their very first RMD to April 1, 2026, will face two taxable distributions stacking into the same calendar year, potentially bumping their income into a higher bracket or triggering Medicare surcharges. The stakes are real and the rules are specific enough that a single misunderstanding can cost thousands of dollars.

This guide is written for retirees and near-retirees who need a clear, current picture of how required minimum distributions 2026 work under the post-SECURE 2.0 framework. By the end, you will know exactly when to start, how to calculate your amount, what the deadlines mean for your tax bill, and which legal strategies can reduce the bite.

Key Takeaways

- The RMD starting age is 73 for anyone born between 1951 and 1959, per IRS retirement plan guidance. Those born in 1960 or later will not face mandatory withdrawals until age 75, beginning in 2033.

- Missing a 2026 RMD now triggers a 25% excise tax on the shortfall, down from the previous 50%, and the penalty drops to 10% if corrected within the IRS’s two-year window for IRA accounts, according to SECURE 2.0 provisions.

- Retirees who delayed their first RMD to April 1, 2026, must take a second RMD by December 31, 2026, stacking two years of taxable income into one calendar year and potentially triggering higher Medicare IRMAA surcharges.

- Roth accounts inside 401(k) and 403(b) plans have been exempt from lifetime RMDs since January 1, 2024, eliminating a major reason retirees used to roll these balances into a Roth IRA before retirement.

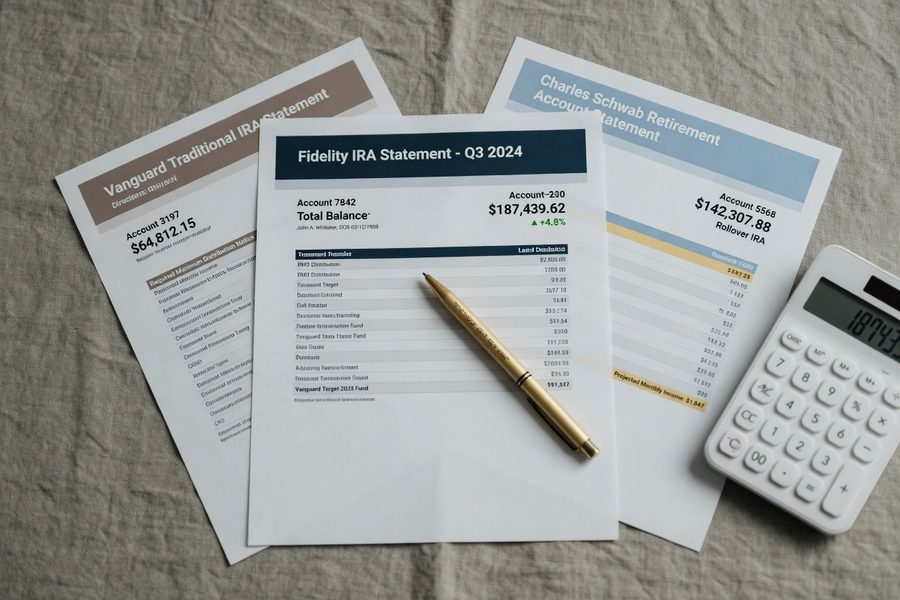

- A qualified charitable distribution (QCD) of up to $111,000 in 2026 per Vanguard’s 2026 figures can satisfy your IRA RMD while keeping the money out of your adjusted gross income entirely.

- A new 2026 provision allows penalty-free withdrawals from retirement plans to pay long-term care insurance premiums, capped at the lesser of 10% of the vested benefit or $2,500 per year, a detail most competing guides skip entirely.

In This Guide

- Step 1: What RMDs Are and Why They Hit Harder Now

- Step 2: Who Must Start RMDs in 2026 and the Exact Timing Rules

- Step 3: How to Calculate Your 2026 RMD Amount

- Step 4: Deadlines, First-Year Choices, and the Double-RMD Trap

- Step 5: Tax-Smart Strategies, Roth Accounts, and Special Cases

- Frequently Asked Questions

Step 1: What RMDs Are and Why They Hit Harder Now

Most retirees understand that a traditional IRA or 401(k) grew tax-deferred, but the IRS eventually collects its share, and required minimum distributions are the mechanism. The government mandates annual withdrawals from pre-tax retirement accounts precisely because it cannot wait indefinitely for taxes on money that was never taxed when contributed. Every dollar you withdraw counts as ordinary income in the year you take it, taxed at your marginal rate.

The SECURE 2.0 Context

Before the SECURE Act of 2019 and its 2022 sequel, RMDs began at age 70½, then shifted to 72. SECURE 2.0 pushed the age to 73 for those born between 1951 and 1959, adding one to three extra years of potential tax planning before mandatory withdrawals begin. That window is not trivial. An extra year or two gives retirees time to convert traditional balances to a Roth IRA, harvest capital losses, or simply defer income while their marginal rate is lower. If you want a broader picture of how retirement savings decisions compound over time, this breakdown of prioritizing retirement savings over college funding offers useful context on long-term account growth.

Why the Stakes Are Higher in 2026

The larger account balances many retirees carry today, built through decades of market gains, translate directly into larger RMD dollar amounts. A bigger RMD means more ordinary income, which can push retirees into a higher federal bracket, increase Social Security taxation, and trigger Medicare IRMAA surcharges that add hundreds of dollars per month to Part B and Part D premiums. Understanding the full tax picture before your first distribution lands is no longer optional if you want to protect what you have built.

The IRS requires RMDs from traditional IRAs, SEP IRAs, SIMPLE IRAs, 401(k) plans, 403(b) plans, 457(b) governmental plans, and profit-sharing plans. Roth IRAs are the one major account type exempt from lifetime RMDs for the original owner.

Step 2: Who Must Start RMDs in 2026 and the Exact Timing Rules

The birth year of the account owner determines everything here. If you were born between 1951 and 1959, your RMD starting age is 73. If you were born in 1960 or later, you will not face mandatory withdrawals until age 75, meaning the first cohort in that group hits age 75 in 2035, not 2026. Anyone born in 1953 who has not already begun distributions is starting their mandatory first RMD year now.

The Required Beginning Date

Your required beginning date (RBD) is April 1 of the year following the year you turn 73. Someone born in 1953 turned 73 in 2026; their RBD is technically April 1, 2027, but that means their first RMD is calculated based on the 2026 account balance and covers the 2026 distribution year. Someone born in 1952 turned 73 in 2025; if they delayed their first RMD, they must take it by April 1, 2026. The IRS RMD FAQ confirms these deadlines in detail, including exactly which birth years fall under each rule.

The Still-Working Exception

One exception many retirees miss: if you are still employed and participate in your current employer’s 401(k) or 403(b), you can delay RMDs from that specific plan until April 1 of the year after you retire, but only if you own less than 5% of the company. This exception does not apply to IRAs, and it does not apply to old 401(k) accounts at former employers. You must coordinate with your plan administrator each year to confirm you remain eligible. If you cross the 5% ownership threshold at any point, the exception disappears immediately.

The still-working exception applies only to the plan at your current employer. If you have an IRA or an old 401(k) from a previous job, those accounts require RMDs based on your age alone, regardless of your employment status.

Step 3: How to Calculate Your 2026 RMD Amount

Your 2026 RMD is calculated by dividing your account’s December 31, 2025 balance by the life expectancy factor assigned to your age in the IRS Uniform Lifetime Table, found in IRS Publication 590-B. That factor reflects your statistical remaining life expectancy and shrinks each year, which means your required withdrawal percentage increases as you age.

A Worked Example

Say you turn 73 in 2026 and your combined traditional IRA balance on December 31, 2025, is $500,000. The Uniform Lifetime Table factor for a 73-year-old is 26.5. Dividing $500,000 by 26.5 gives an RMD of approximately $18,868 for the year, or about $1,572 per month if you choose to spread distributions. The following year, at age 74, the factor drops to 25.5, so the same $500,000 balance (ignoring gains or losses) would produce an RMD of approximately $19,608. The math compounds: both the shrinking factor and any remaining account growth determine each year’s mandatory amount.

Aggregation Rules Across Multiple Accounts

Here is where retirees with several accounts often get confused. For traditional IRAs, you calculate the RMD for each account separately, but you can take the total combined amount from any one or combination of those IRA accounts. For 401(k) and 403(b) plans, that aggregation rule does not apply, each employer plan requires its own separate RMD withdrawal. You cannot satisfy a 401(k) RMD by pulling extra from an IRA, and you cannot use a 403(b) distribution to cover a 401(k) obligation. The IRS treats each employer plan as a standalone obligation.

A retiree with a $500,000 IRA at age 73 owes roughly $18,868 in mandatory withdrawals in 2026. By age 80, that same balance, if it remained flat, would require nearly $24,390 in annual distributions, using the Uniform Lifetime Table factor of 20.2 for that age.

| Account Type | RMD Required? | Aggregation Allowed? | Still-Working Exception? |

|---|---|---|---|

| Traditional IRA | Yes, starting at 73 | Yes, pool IRAs and take from any | No |

| Roth IRA | No lifetime RMD for original owner | N/A | N/A |

| 401(k), current employer | Yes, unless still working and under 5% owner | No, each plan separate | Yes |

| 401(k), former employer | Yes, starting at 73 | No, each plan separate | No |

| 403(b) | Yes, starting at 73 | Yes, pool 403(b)s only | Yes (current employer only) |

| Roth 401(k) / Roth 403(b) | No, exempt since Jan 1, 2024 | N/A | N/A |

| 457(b) Governmental | Yes, starting at 73 | No, each plan separate | No |

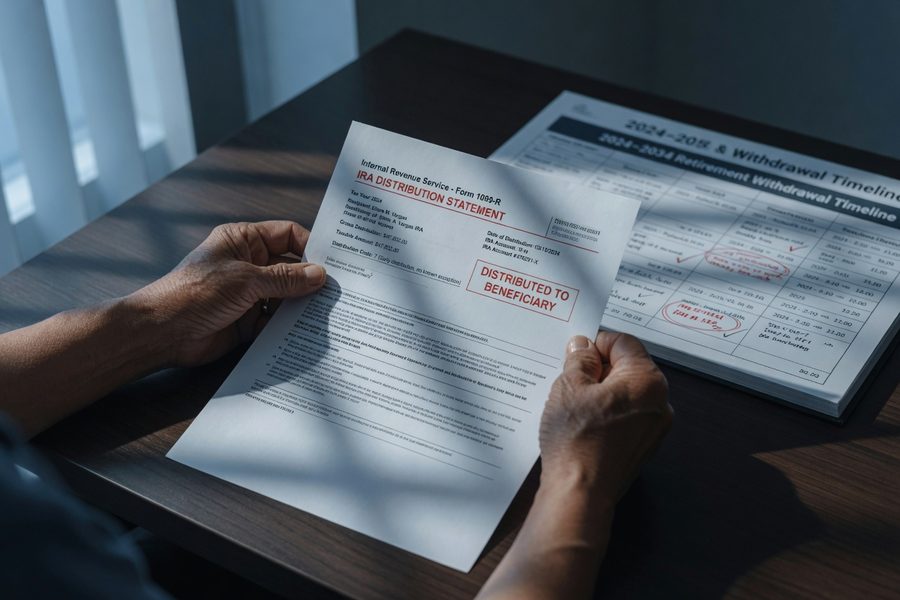

Step 4: Deadlines, First-Year Choices, and the Double-RMD Trap

The first-year delay option sounds appealing until you run the numbers. The IRS confirms that you may delay your very first RMD until April 1 of the year after you turn 73, but your second RMD is still due by December 31 of that same year. That means two full RMDs land in one tax year, stacking additional ordinary income that can push you into a higher bracket, increase how much of your Social Security benefit is taxable (up to 85% of benefits become taxable above certain income thresholds), and trip Medicare’s IRMAA income lookback, which uses your income from two years prior to set surcharges.

For most retirees, taking the first RMD by December 31 of the year they turn 73, rather than delaying to April 1, produces a better tax outcome. The delay is rarely worth it unless your income happens to be unusually low in the delay year and unusually high in the year prior.

If you turned 73 in 2025 and delayed your first RMD to April 1, 2026, consider spreading both distributions evenly across 2026, for example, taking the 2025 RMD in January and the 2026 RMD in July, rather than front-loading. Your tax bill is the same, but spreading reduces the risk of a large lump-sum triggering withholding surprises.

Step 5: Tax-Smart Strategies, Roth Accounts, and Special Cases

There are several legitimate ways to reduce how much of your RMD hits your taxable income, and some apply specifically to 2026 rules that most guides do not cover. The right approach depends on whether you are charitably inclined, whether you carry long-term care insurance, and how much pre-tax money remains in your accounts.

Qualified Charitable Distributions

A qualified charitable distribution (QCD) allows IRA owners aged 70½ or older to transfer money directly from a traditional IRA to a qualifying charity. The amount never appears in your adjusted gross income, which means it satisfies the RMD obligation without triggering Social Security taxation increases or Medicare IRMAA surcharges. The 2026 annual QCD limit is $111,000 per Vanguard’s 2026 figures, enough to cover the RMD obligation for the vast majority of retirees with moderate balances. The check must go directly from the IRA custodian to the charity; if you receive the funds first and then donate, the tax exclusion disappears.

The 2026 Long-Term Care Withdrawal Provision

SECURE 2.0 added a provision that most 2026 RMD guides skip entirely: starting in 2026, retirees can take penalty-free distributions from retirement plans to pay long-term care insurance premiums, capped at the lesser of 10% of the vested account balance or $2,500 per year. This is not an RMD reduction strategy per se, but it allows retirees already taking distributions to direct a portion toward a specific expense without triggering the 10% early-withdrawal penalty for those under 59½. For retirees in their early 60s who have long-term care premiums, this is a meaningful new tool.

Roth Conversions Before RMDs Begin

If you have not yet reached your RMD starting age, converting a portion of your traditional IRA to a Roth IRA each year reduces the future balance subject to mandatory withdrawals. Every dollar converted is taxed now at your current rate but grows tax-free and carries no future RMD obligation for you as the original owner. The math favors conversion in years when your marginal rate is lower than what you expect it to be when RMDs begin, typically the gap between retirement and age 73. If you are also working through other debt obligations during this window, reviewing how to prioritize and negotiate credit card debt can free up cash flow to cover the tax bill on conversions without tapping savings.

Roth 401(k) and 403(b) Accounts Since 2024

A significant SECURE 2.0 change took effect on January 1, 2024: Roth balances held inside employer-sponsored 401(k) and 403(b) plans are now exempt from lifetime RMDs for the original owner. Before this change, even Roth 401(k) money was subject to mandatory distributions, forcing many retirees to roll balances into a Roth IRA just to avoid the requirement. That workaround is no longer necessary. If your 401(k) includes a Roth contribution component, those funds can remain in the plan indefinitely during your lifetime without triggering any withdrawal obligation.

Inherited IRAs and Non-Spouse Beneficiaries

Non-spouse beneficiaries who inherited an IRA after December 31, 2019, are subject to the 10-year rule: the account must be fully distributed by the end of the tenth year following the original owner’s death. The IRS issued additional clarification, after years of confusion, that most non-spouse beneficiaries who inherited from an owner who had already begun RMDs must also take annual distributions within that 10-year window. This is a separate set of rules from the retiree’s own RMD obligation but affects many adult children of retirees who are simultaneously managing both their own retirement accounts and inherited ones.

Planning your RMD strategy intersects directly with your annual tax return. If you need help navigating the tax filing side of retirement income, the guide covering free IRS tax help and overlooked credits is worth reviewing before filing season. Understanding what assistance is available can reduce the cost of professional tax prep during your first RMD years.

Frequently Asked Questions

What happens if I miss my 2026 RMD deadline?

Missing a 2026 RMD deadline triggers a 25% excise tax on the amount you failed to withdraw, a significant reduction from the previous 50% penalty that applied before SECURE 2.0. For IRA accounts, that penalty drops further to 10% if you correct the shortfall within two years of the missed deadline. You report and pay the penalty using IRS Form 5329, and you can also request a waiver by attaching a statement of reasonable cause. The lower penalty is a meaningful improvement, but it still represents a steep cost on large missed amounts.

Can I take more than my required minimum distribution in 2026?

Yes, you can always withdraw more than the required amount from your IRA or 401(k). Taking extra does not reduce next year’s RMD calculation; each year’s required amount is computed independently based on the prior year-end balance and your age factor. Withdrawing above the minimum simply means more taxable income in the current year, so consider the bracket impact before pulling additional funds.

Do required minimum distributions affect my Medicare premiums?

RMDs count as ordinary income and can trigger Medicare IRMAA surcharges, which use your income from two years prior to set Part B and Part D premium adjustments. If your 2026 RMD (or a double-RMD from delayed first distributions) pushes your modified adjusted gross income above IRMAA thresholds, you could face surcharges on your 2028 Medicare premiums. Using a QCD to satisfy part of your IRA RMD keeps that income out of your AGI, which is one of the most direct ways to avoid this outcome. If you are also managing other retirement-period expenses, the article on rising poverty guidelines in 2026 covers income-related benefit thresholds that may also be relevant to your planning.

Should I delay my first RMD to April 1, 2026, or take it before December 31, 2025?

For most retirees, taking the first RMD by December 31 of the year you turn 73, rather than delaying to April 1 of the next year, produces a better tax result. Delaying forces two full RMDs into one calendar year, which stacks taxable income, increases Social Security taxation, and can trigger Medicare IRMAA surcharges. The delay only makes sense if your income in the year you turn 73 is unusually high and you expect the following year to be significantly lower.

How do I calculate my RMD if I have multiple IRAs and a 401(k)?

Calculate each account’s RMD separately using the December 31 prior-year balance divided by the Uniform Lifetime Table factor for your age. For traditional IRAs, you can pool the total and take the combined amount from any one or more IRA accounts. For 401(k) plans, each account requires its own separate withdrawal, you cannot use an IRA distribution to satisfy a 401(k) RMD, or vice versa. 403(b) plans follow their own pooling rule: you can aggregate multiple 403(b) accounts and take the total from any of them, but 403(b) distributions cannot cover 401(k) obligations.

Is my Roth 401(k) subject to RMDs in 2026?

No. Roth balances held inside 401(k) and 403(b) plans have been exempt from lifetime required minimum distributions since January 1, 2024, under SECURE 2.0. You no longer need to roll Roth 401(k) funds into a Roth IRA to escape the RMD requirement. Roth IRAs have always been exempt from lifetime RMDs for the original owner, so both account types now share that advantage.

What is a qualified charitable distribution and how much can I give in 2026?

A qualified charitable distribution (QCD) is a direct transfer from a traditional IRA to a qualifying 501(c)(3) charity, available to account owners aged 70½ or older. The transferred amount is excluded from your adjusted gross income and counts toward satisfying your annual RMD obligation. The 2026 annual QCD limit is $111,000 per person, per Vanguard’s 2026 data. The distribution must go directly from the IRA custodian to the charity, if you receive the funds personally first, the tax exclusion is lost.

What is the new long-term care premium withdrawal rule in 2026?

Starting in 2026, SECURE 2.0 permits penalty-free distributions from retirement plans specifically to pay long-term care insurance premiums. The annual cap is the lesser of 10% of your vested account balance or $2,500. The amount is still taxable as ordinary income, the benefit is the elimination of the 10% early-withdrawal penalty for those under 59½, and the ability to use pre-tax retirement funds for a specific healthcare expense. For retirees already past 59½, the primary benefit is the designated purpose rather than a penalty waiver.

Can I use my spouse’s IRA to satisfy my own RMD?

No. RMDs are calculated per account owner, and each spouse must take their own required distributions from their own accounts. You cannot use your spouse’s IRA withdrawal to satisfy your RMD obligation, and your spouse’s distribution does not reduce or offset yours. Spouses who inherit each other’s IRAs do have a spousal rollover option that allows them to treat the inherited IRA as their own, which resets the RMD calculation to the surviving spouse’s own age and required beginning date.

Sources

- IRS, Retirement Topics: Required Minimum Distributions (RMDs)

- IRS, Retirement Plan and IRA Required Minimum Distributions FAQs

- IRS Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs)

- Vanguard, What Are RMDs? 2026 Limits and Rules

- IRS, About Form 5329: Additional Taxes on Qualified Plans