Reviewed by the MyFinancial101 Editorial Team

Our Take

For most full-time freelancers earning between $50,000 and $150,000 in net self-employment income, a Solo 401(k) is the strongest retirement plan for freelancers available, it permits nearly triple the annual contribution of a SEP IRA at the $50K income level, and it opens the door to the Mega Backdoor Roth. The case for the SEP IRA wins when you are in your first year of freelancing and cannot open a Solo 401(k) before December 31, or when your income is genuinely too unpredictable to commit to a plan document. Start with the SEP IRA if you missed the deadline; switch to a Solo 401(k) once your income stabilizes.

The freelance economy now includes 72.9 million independent workers in the United States, according to industry workforce data compiled in 2026, yet a large share of them are building their working lives without any structured plan to fund retirement. That is not a minor oversight. Every year without a tax-advantaged account is a year of compound growth permanently forfeited, and it shrinks the Social Security benefit calculation in ways most freelancers never see coming.

This article is for self-employed workers, independent contractors, and freelancers with no employer-sponsored plan who want a clear, mechanically honest answer to how retirement savings actually work at their income level. The recommendation holds best for those earning at least $30,000 in net self-employment income; the math changes below that threshold, and we name those exceptions directly.

Key Takeaways

- 72.9 million Americans work as freelancers or independent contractors, per SQ Magazine’s workforce analysis, the vast majority without any employer retirement contribution.

- A Solo 401(k) allows up to $70,000 in total contributions in 2025, per Fidelity’s IRS-sourced contribution guide, versus roughly $11,600 for a SEP IRA at $50K net self-employment income, a gap of more than $23,000 per year.

- 65% of Americans believe their retirement savings are off track or are unsure, according to the Federal Reserve’s 2024 household economics report via SmartAsset, freelancers face this challenge without a payroll auto-deduction to offset inertia.

- The SEP IRA can be opened and funded as late as the tax-filing extension deadline (October 15 the following year), making it the right first-year fallback when a freelancer misses the Solo 401(k)’s hard December 31 setup cutoff.

- In my experience reviewing freelancer finances, the single most common mistake is conflating an emergency fund with a retirement fund, a freelancer needs three to six months of baseline expenses in a liquid account before directing cash toward retirement accounts, or the retirement fund becomes the emergency fund.

The Real Retirement Gap Freelancers Face

The problem is worse than most freelancers realize, and it is mostly behavioral. Only about 39% of working Americans hold any tax-preferred retirement account, per the Federal Reserve’s 2024 Survey on Household Economic Decisionmaking, but participation drops far lower among the self-employed in single-person businesses, where no payroll system auto-enrolls anyone and no employer contributes a match.

There is also a Social Security problem that almost no freelancer retirement guide addresses honestly. The Social Security Administration calculates your benefit using your 35 highest-earning years. If you spent your 20s or early 30s freelancing at low reported income, or took any career gap years, those years count as zeros in the formula and drag your eventual benefit down permanently. A W-2 worker with identical peak-decade earnings but a steadier earnings history will receive a structurally higher benefit. That is not a theoretical risk; it is a predictable arithmetic penalty for anyone with more than a few low-income years on record.

There is also the underreporting trap to name plainly. Some freelancers aggressively reduce reported self-employment income to cut their 15.3% self-employment tax bill. What those tax strategies do not show on the return is the downstream cost: every dollar of SE income you legally shelter from the SE tax is also a dollar that does not count toward your SSA benefit calculation. The short-term tax win can produce a long-term retirement loss. The trade-off should be a conscious decision, not a surprise.

What I see in practice: Freelancers who start tracking this issue tend to discover it at tax time, not during the year when they could act on it. By then, the Solo 401(k) window has usually closed. The behavioral fix is simple: review account type in October, not April.

How Much Should a Freelancer Actually Save?

The standard 15% of gross income target assumes a W-2 paycheck that arrives on schedule. Freelancers need a tiered model instead: a floor contribution in lean months, even $200 counts, and a surge contribution when a large payment lands. A fixed percentage transfer the same day client payments arrive removes the willpower variable entirely.

For a concrete target: using the 4% withdrawal rule, a freelancer who wants $40,000 per year from savings in retirement needs roughly $1,000,000 in their retirement accounts. At a 7% average annual return and a 25-year savings horizon, that requires contributing roughly $1,500 per month, which underscores why account type and contribution ceiling matter more for freelancers than for employees with automatic payroll deductions. If you are still building the income base to fund retirement savings, reviewing higher-income opportunities available in 2026 may be a practical first step.

The Four Main Accounts, And Which One Wins at Your Income Level

At most income levels above $40,000 in net self-employment earnings, the Solo 401(k) wins, and the margin is larger than most comparisons show. Here is the actual dollar-level breakdown.

Solo 401(k) vs. SEP IRA at $50K Net Income

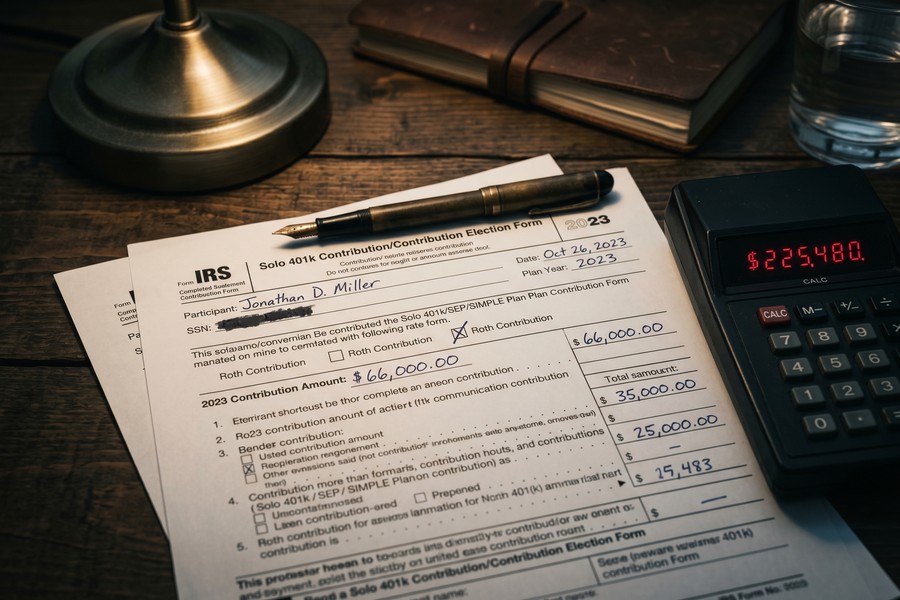

A Solo 401(k) has two contribution components: an employee deferral of up to $23,500 in 2025, plus an employer profit-sharing contribution of up to 25% of net self-employment compensation. At $50,000 net SE income, the employer share comes to roughly $11,600, so total contributions reach approximately $35,000. A SEP IRA, which accepts only the employer-side 25% contribution, lands at that same $11,600. The Solo 401(k) allows roughly three times as much at this income level, a gap of about $23,000 per year that compounds dramatically over a 20-year career.

The IRS outlines all four plan types available to self-employed individuals, Solo 401(k), SEP IRA, SIMPLE IRA, and traditional/Roth IRA, and the contribution rules for each. The Department of Labor’s SEP guide for small businesses confirms that sole proprietors can establish and contribute as their own employer, with no employees required. If you are new to investing structures and want to understand the broader principles before choosing an account, this primer on starting to invest with no prior experience covers the fundamentals.

The Comparison at a Glance

| Account Type | 2025 Max Contribution | Roth Option? | Setup Deadline | Best For |

|---|---|---|---|---|

| Solo 401(k) | $70,000 (+ $7,500 catch-up age 50+) | Yes (Roth deferrals allowed) | December 31 of contribution year | Net SE income $40K+, wants max shelter |

| SEP IRA | $70,000 (capped at 25% of eligible comp) | No (traditional only at contribution) | Tax-filing deadline + extension (Oct 15) | First-year freelancers, high earners with late filing |

| SIMPLE IRA | $16,500 employee deferral | No | October 1 of the year it will be effective | Freelancers with a few employees |

| Traditional/Roth IRA | $7,000 (+ $1,000 catch-up age 50+) | Yes (Roth IRA) | Tax-filing deadline (April 15) | Low-income years, income below Roth phase-out |

Tax professionals who specialize in self-employed clients consistently point to one behavioral truth: most freelancers do not think about this until tax time, and by then the planning window has closed. The mechanics of which account to open matter less than opening one before December 31.

The Solo 401(k)’s One Hard Constraint

The plan must be opened before December 31 of the tax year for which you want to make employee deferrals. Miss that date and you lose the employee-deferral component entirely, which is the piece that gives the Solo 401(k) its advantage over the SEP IRA at moderate income levels. For first-year freelancers who discover this in January, the practical move is to open a SEP IRA immediately, fund it through the October extension deadline, and then open the Solo 401(k) before the following December 31 once income is more predictable. Also worth noting: the IRS Publication 560 contains the official contribution worksheets and deduction limits, and the IRS self-employed contribution calculator explains the circular calculation required to determine your exact deductible amount.

Saving When Your Income Is Unpredictable

Irregular income is the most cited reason freelancers give for not saving, and it is a real friction, not an excuse. The practical fix is behavioral, not structural: transfer a fixed percentage of every client payment into a separate retirement account on the day the payment clears. Ten percent of a $3,000 project payment is $300 set aside before it blends into operating expenses.

The SEP IRA has a built-in advantage for volatile earners that the Solo 401(k) cannot match: there is no minimum annual contribution requirement. You can contribute heavily in a strong year and contribute nothing in a bad one without penalty or plan disqualification. Once a Solo 401(k) plan document is in place, amendments have more procedural weight. That flexibility is a genuine reason to keep the SEP IRA as a fallback, even after you have switched to a Solo 401(k) as your primary vehicle.

One clarification most articles conflate: an emergency fund and a retirement fund are not interchangeable. A freelancer without three to six months of baseline expenses in a separate liquid account, a high-yield savings account, not a brokerage, will inevitably pull from retirement savings when a slow month hits. Fund the emergency buffer first. Retirement contributions then stay untouched and avoid the early-withdrawal penalties and lost compounding that make premature withdrawals so costly. If credit card debt is currently eating into your ability to build that buffer, address it in parallel, high-interest debt destroys the return on any savings strategy sitting beside it.

What clients often miss: Most freelancers I work with underestimate how much their quarterly estimated tax payments compete with retirement contributions for the same cash. Earmarking retirement contributions immediately after each project payment, before the estimated tax reserve builds, is the only cadence that consistently works.

Advanced Tax Moves Most Freelancers Overlook

The Mega Backdoor Roth is one of the most powerful legal tax shelters available exclusively to the self-employed, and most freelancer retirement guides either skip it entirely or mention it in a single sentence. Here is what it actually means: because a Solo 401(k) is exempt from nondiscrimination testing (there are no other employees to discriminate against), a self-employed worker can make after-tax contributions to the plan and then convert them to Roth. This potentially shelters the full $70,000 2025 contribution limit on a tax-free growth track, with no income ceiling, a route unavailable to W-2 employees whose workplace 401(k) plans fail nondiscrimination tests. The DOL and IRS joint publication on retirement solutions for small businesses confirms the Roth options available to self-employed individuals under SECURE 2.0.

The HSA as a Third Tax Bucket

A freelancer with a qualifying high-deductible health plan can contribute to a Health Savings Account, invest the balance, and withdraw it tax-free for qualified medical expenses in retirement. That creates a third tax-advantaged bucket alongside pre-tax and Roth accounts, and medical costs in retirement are substantial enough that a dedicated HSA balance is not redundant with a Solo 401(k) Roth. The 2025 HSA contribution limit is $4,150 for individual coverage and $8,300 for family coverage, per IRS guidelines.

The SECURE 2.0 Catch-Up Rule for 2026

Starting in 2026, Solo 401(k) participants who earned over $150,000 in the prior year must make their catch-up contributions on a Roth basis, they can no longer be made pre-tax. This is a new compliance requirement that virtually none of the currently ranking freelancer retirement guides have addressed. If you are in that income range and have been making pre-tax catch-up contributions, your plan administrator needs to confirm your plan document has been updated for this requirement. Separately, SECURE 2.0 introduced an enhanced catch-up limit of up to $11,250 additional contributions for ages 60–63 in 2026, versus $8,000 for ages 50–59, a legitimate accelerant for late starters, but only if the account is already properly structured and open.

Where this gets tricky: The Mega Backdoor Roth requires a Solo 401(k) plan document that explicitly allows after-tax contributions and in-plan Roth conversions. Not every brokerage’s off-the-shelf Solo 401(k) includes this language. Confirm with your provider before assuming the feature is available.

Where This Recommendation Falls Short

The Solo 401(k) recommendation has real drawbacks, and I want to name them plainly rather than bury them at the end of a section.

The most honest concession: the Solo 401(k) is not for everyone in the freelancer category. If you have any employees, even a part-time assistant, you cannot use a Solo 401(k). The plan is strictly for businesses with no employees other than the owner and a spouse. The moment you hire someone, the Solo 401(k) must be terminated or converted, which triggers administrative and potentially tax consequences. For freelancers who expect to hire within the next two to three years, a SEP IRA or SIMPLE IRA may be the more durable choice, precisely because it scales with employees rather than disqualifying when the first one appears.

The catch with the Solo 401(k)’s December 31 setup deadline is real and consequential. A freelancer who discovers this article in January has already missed the window for that tax year’s employee deferrals. The SEP IRA wins on simplicity and timing flexibility for anyone who is learning this mid-year. That is not a minor edge case, most freelancers do not engage with retirement planning on a December calendar.

The tradeoff in the social security math also cuts both ways. Maximizing deductible retirement contributions reduces your taxable self-employment income, which reduces your SE tax, but it also reduces the income figure that feeds your SSA benefit calculation. At moderate income levels, the long-term Social Security cost of aggressive tax-sheltering is real, even if it is impossible to calculate precisely without a Social Security benefit projection. Freelancers should run both numbers before assuming that maxing contributions is always the right call.

Finally, the risk is behavioral more than structural for many freelancers. The best-designed retirement account is useless without consistent contributions. If the mechanics of a Solo 401(k) create enough friction that you delay opening it for two years, a SEP IRA you actually use on day one is worth more. Starting is the strategy, and if you want to understand how that same principle applies to building retirement savings earlier than most people think to start, the case for prioritizing retirement over college savings makes a related point worth reading.

How We Sourced This

This article draws primarily from IRS Publication 560 and the IRS retirement plans page for self-employed individuals, both verified, for contribution limits, deadlines, and deduction rules. Contribution limit figures for the Solo 401(k) and SEP IRA ($70,000 for 2025) are sourced from Fidelity’s IRS-cited contribution guides, published in 2025. The workforce size figure (72.9 million) comes from SQ Magazine’s 2026 industry data compilation; the retirement savings gap statistics come from Federal Reserve survey data for 2024, as cited by The Motley Fool and SmartAsset. DOL publications 4333 and the DOL/IRS joint small-business retirement guide were reviewed for SEP IRA and SECURE 2.0 Roth provisions. SECURE 2.0 catch-up contribution figures for 2026 reflect IRS guidance current as of the article’s publication date; readers should verify these limits have not been subsequently revised before acting.

Related reading: Are Client Meal Expenses Deductible for Freelancers in California? Tax Rules.

Frequently Asked Questions

What is the best retirement plan for freelancers with no employees?

For most full-time freelancers earning above $40,000 in net self-employment income, a Solo 401(k) offers the highest contribution ceiling and the most tax flexibility, including Roth options. If you missed the December 31 setup deadline, open a SEP IRA instead, it can be funded as late as October 15 of the following year via tax extension.

Can a freelancer contribute to both a Solo 401(k) and an IRA?

Yes, a freelancer can contribute to both a Solo 401(k) and a traditional or Roth IRA in the same year, subject to the standard IRA income and contribution limits. The IRA adds up to $7,000 in additional tax-advantaged savings ($8,000 for those 50 and older in 2025), making it a useful complement when the goal is maximizing total shelter.

How does self-employment affect Social Security benefits?

Freelancers do qualify for Social Security and pay the full 15.3% self-employment tax covering both employee and employer shares. The 35-year averaging formula means that years with zero or very low reported self-employment income count as zeros, permanently pulling down the eventual benefit, a penalty W-2 workers with steady income histories do not face in the same way.

What is the Solo 401(k) December 31 deadline, and what happens if I miss it?

The Solo 401(k) plan document must be established by December 31 of the tax year for which you want to make employee salary deferrals. Missing this deadline does not prevent you from making employer profit-sharing contributions the following year in some cases, but you lose the employee-deferral component, the piece that makes the Solo 401(k) superior to a SEP IRA at moderate income levels. Open a SEP IRA if you missed it; revisit the Solo 401(k) before next December 31.

Is a SEP IRA or Solo 401(k) better at $100,000 in freelance income?

At $100,000 in net self-employment income, the Solo 401(k) still wins by a wide margin. The employer profit-sharing contribution alone approaches $18,500, and adding the $23,500 employee deferral brings the total near $42,000, well above the SEP IRA’s $25,000 ceiling at the same income level. The Solo 401(k)’s advantage narrows only near the top of the $70,000 combined limit.

What is the Mega Backdoor Roth, and can any freelancer use it?

The Mega Backdoor Roth allows a Solo 401(k) holder to make after-tax contributions to the plan and convert them to Roth, potentially sheltering the full $70,000 2025 contribution limit on a tax-free growth track with no income ceiling. It is available only through a Solo 401(k), not a SEP IRA, and only if the plan document explicitly permits after-tax contributions and in-plan Roth conversions. Confirm with your brokerage before assuming this feature is included in a standard off-the-shelf plan.

Sources

- Internal Revenue Service, Retirement Plans for Self-Employed People

- IRS Publication 560, Retirement Plans for Small Business (SEP, SIMPLE, and Qualified Plans)

- IRS, Self-Employed Individuals: Calculating Your Own Retirement Plan Contribution and Deduction

- U.S. Department of Labor, SEP Retirement Plans for Small Businesses (Publication 4333)

- DOL/IRS, Choosing a Retirement Solution for Your Small Business

- Fidelity, Solo 401(k) Contribution Limits 2025

- The Motley Fool, Retirement Savings Gap Statistics (Federal Reserve 2024 Survey Data)

- SmartAsset, Average Retirement Savings: Are You Normal? (Federal Reserve 2024 Data)