Fact-checked by the MyFinancial101 editorial team

Key Takeaways

- Nearly 90% of VA-backed home loans are made with zero down payment, according to the U.S. Department of Veterans Affairs, a benefit available to every eligible first-time user with full entitlement.

- First-time VA purchase users pay a funding fee of 2.15% (with 0% down) on the loan amount, significantly lower than the 3.3% charged on subsequent uses, and fully exempt for those receiving service-connected disability compensation.

- VA loans carry no monthly private mortgage insurance, which saves most first-time buyers between $150 and $300 per month compared to conventional loans with less than 20% down.

- 118,898 VA purchase loans went to first-time homebuyers in fiscal year 2024, confirming the program remains an active and widely used path to ownership for military families.

- Since 2020, first-time VA users with full entitlement face no maximum loan amount, as long as the home appraises and they qualify financially, there is no cap on purchase price.

- The VA funding fee is tax-deductible, a relatively recent change that reduces the true net cost of buying for eligible military homebuyers who itemize their federal deductions.

In This Guide

- Why VA Loans Stand Out for First-Time Military Homebuyers

- Verifying Eligibility and Obtaining Your Certificate of Eligibility

- The VA Funding Fee Explained for First-Time Users

- Step-by-Step Process from Prequalification to Closing

- Qualification Standards Lenders Actually Use

- VA Appraisal Standards vs. Conventional: What First-Timers Need to Know

- Seller Concessions and How They Work With a VA Loan

- Potential Roadblocks and How First-Timers Overcome Them

- What Happens After You Use the Benefit the First Time

Why VA Loans Stand Out for First-Time Military Homebuyers

For a service member who has spent years living in base housing or renting near post, buying a home can feel like starting from zero. No substantial down payment savings, no long credit history with a mortgage, and often a move-heavy background that makes lenders nervous. The VA loan first time buyer experience is designed precisely for that situation, and the numbers prove it works. According to the U.S. Department of Veterans Affairs, nearly 90% of VA-backed home loans are made with no down payment at all.

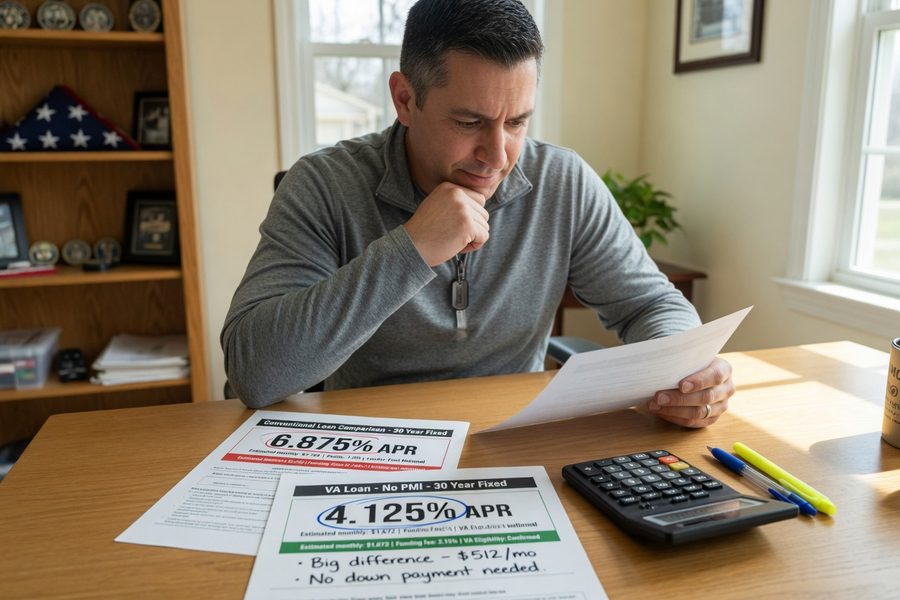

That single fact reshapes the entire affordability math. On a $350,000 home, a conventional loan at 5% down requires $17,500 upfront, plus private mortgage insurance (PMI) of roughly $150 to $300 per month until you reach 20% equity. A first-time VA buyer pays neither. Skipping the down payment keeps cash in the bank. Skipping PMI saves real money every single month for years.

This benefit also arrives without a loan ceiling for eligible first-time users. Since a 2020 change to federal law, borrowers with full entitlement, which includes every veteran or service member who has never used the VA loan benefit before, face no maximum loan amount, provided the home appraises at the purchase price and the borrower qualifies financially. That removes one of the last remaining barriers for buyers in higher-cost markets.

The PMI Savings in Plain Dollars

Consider what PMI actually costs over time. A buyer purchasing a $350,000 home with 5% down on a conventional loan would carry PMI at an average rate of around 0.85% annually on the loan balance. That works out to roughly $2,800 per year, or about $233 per month, during the first several years of the loan. Over five years before reaching the equity threshold to cancel PMI, that is nearly $14,000 spent on insurance that builds zero equity.

A VA buyer in the same scenario pays $0 per month in mortgage insurance, ever. The upfront funding fee (discussed in detail later) is a one-time cost, not a recurring drain. For service members who have been disciplined about saving but simply haven’t had the time or stability to accumulate a large down payment, this structure is genuinely advantageous, not just marginally better.

118,898 VA purchase loans went to first-time homebuyers in fiscal year 2024, according to the U.S. Department of Veterans Affairs Annual Benefits Report, a figure that reflects how actively military families are using this program to enter homeownership.

Competitive Interest Rates

Historically, VA loans have carried interest rates 0.25% to 0.50% below comparable conventional loans. The reason is the VA’s guaranty: the federal government backs a portion of each loan, which reduces lender risk and allows institutions like Chase, Navy Federal, and SoFi to offer better terms to qualifying borrowers. On a $350,000 loan over 30 years, a half-point rate difference saves approximately $35,000 in total interest. That is not a rounding error; it is a meaningful long-term advantage for a first-time buyer choosing between loan types.

Verifying Eligibility and Obtaining Your Certificate of Eligibility

Eligibility for the VA home loan benefit is tied to military service, not to income or first-time buyer status. The U.S. Department of Veterans Affairs outlines four primary eligibility categories: active duty service members, veterans, National Guard and Reserve members (with qualifying service), and surviving spouses of veterans who died in service or from a service-connected disability.

Service length requirements differ by era and component. Most active duty members become eligible after 90 continuous days of service. Veterans who served after August 2, 1990 generally need 24 months of continuous service or the full period for which they were called to active duty. Guard and Reserve members typically need six years of service in their component, though this can be shorter if they were activated to federal active duty under certain orders. These details matter; a lender or VA regional loan center can clarify your specific situation quickly.

What the Certificate of Eligibility Actually Does

The Certificate of Eligibility (COE) is the official document that confirms to a lender that you have earned the VA home loan benefit. It shows the amount of entitlement available, which for first-time users with no prior VA loan is full basic entitlement. The VA describes requesting the COE as the first step in the home-buying process for eligible military homebuyers new to the program.

One practical point most first-time users miss: you do not need the COE in hand before you start shopping or get pre-approved. Many VA-approved lenders, including large military-focused shops and national banks like Chase, can pull your COE directly through the VA’s automated system in minutes. You can also request it yourself through the VA’s eBenefits portal, by mail, or through your lender. Do not let an absent COE slow down your search.

Common Eligibility Myths

Several misconceptions keep eligible buyers from even applying. Owning a home previously does not disqualify you; the VA loan benefit has no restriction based on prior homeownership. Having used a VA loan before does not block access either, it affects entitlement amounts and the funding fee rate, but does not bar reuse. A less-than-perfect FICO Score does not automatically disqualify you; VA underwriting places significant weight on residual income, which is a meaningfully different risk framework from how conventional lenders typically assess creditworthiness.

Surviving spouses who remarried on or after December 16, 2003, and who were at least 57 years old at the time of remarriage, may still be eligible for the VA home loan benefit. Eligibility rules for surviving spouses are more nuanced than many assume, always verify directly with the VA.

The VA Funding Fee Explained for First-Time Users

The VA funding fee is a one-time charge paid to the Department of Veterans Affairs that helps sustain the loan guarantee program for future borrowers. For a first-time user putting 0% down, the current rate is 2.15% of the loan amount. On a $350,000 purchase, that equals $7,525. With a down payment of 5% or more, the rate drops to 1.5%; at 10% or more down, it falls to 1.25%.

Subsequent use of the VA loan, meaning buyers who have used a VA loan before and are doing so again, incurs a fee of 3.3% with 0% down. That gap between 2.15% and 3.3% is one of several concrete reasons to use the benefit deliberately the first time, rather than deferring it.

Who Pays Zero, and Why It Matters

Certain borrowers are fully exempt from the funding fee. These include veterans receiving VA compensation for service-connected disabilities, active duty service members with a pre-discharge disability rating, surviving spouses of veterans who died in service or from service-connected causes, and Purple Heart recipients on active duty. The Veterans Benefits Administration confirms these exemptions as part of the core VA home loan benefit structure. For exempt buyers, the total upfront cost of closing on a VA loan is substantially lower than any comparable loan product.

If you are not exempt, you have two choices: pay the funding fee at closing as part of your closing costs, or roll it into the loan balance. Rolling it in avoids any out-of-pocket payment but increases the amount you are financing and therefore the interest you pay over the life of the loan. On a $350,000 loan at 6.5%, financing that $7,525 fee adds roughly $16,000 in total interest over 30 years. That is a real tradeoff worth understanding before you decide.

The 2026 Tax Deductibility Change

The VA funding fee is tax-deductible for borrowers who itemize their federal deductions. This provision, which lapsed for several years and was restored, reduces the net effective cost of the fee for buyers in higher tax brackets. A first-time buyer in the 22% federal tax bracket who pays a $7,525 funding fee could reduce their federal tax liability by approximately $1,655 in the year of purchase, per IRS Publication 936 guidance on home mortgage interest deductions. That does not eliminate the cost, but it meaningfully narrows the gap between the VA funding fee and conventional mortgage insurance costs over the first year of ownership. If you plan to itemize, talk to a tax professional about timing your closing accordingly.

Rolling the funding fee into your loan balance increases the amount you owe from day one; your loan may start slightly underwater relative to the purchase price. In a flat or declining market, this creates a small risk of negative equity early in ownership. Buyers who anticipate a short hold period should weigh this carefully.

Step-by-Step Process from Prequalification to Closing

The VA home loan process follows a recognizable sequence, but a few steps are unique to this program and catch first-time users off guard. Knowing the order, and what can happen at each stage, prevents costly delays.

Getting Pre-Approved With the Right Lender

Pre-approval starts with selecting a VA-approved lender, which is not the same as any lender who offers mortgage products. VA-approved lenders have been vetted by the VA and are authorized to originate loans backed by the federal guarantee. Choosing a lender with a dedicated military lending team, whether that is a specialist like Veterans United, USAA, or Navy Federal, versus a generic mortgage officer at a large retail bank, makes a real difference in how smoothly the process goes. VA-specific lenders understand residual income calculations, know how to read a Leave and Earnings Statement (LES), and are familiar with deployment scenarios that can complicate timelines.

Documentation required for pre-approval typically includes your last two years of W-2s or tax returns, recent pay stubs or your LES if active duty, two months of bank statements, and a list of monthly debt obligations. If you receive Basic Allowance for Housing (BAH) or Basic Allowance for Subsistence (BAS), gather documentation for those as well; lenders can count these non-taxable allowances as qualifying income, which often materially improves your debt-to-income ratio (DTI).

The VA Appraisal and What Comes After

Once you have an accepted offer, the lender orders a VA appraisal through the VA’s roster of approved appraisers. This appraisal does two things simultaneously: it establishes the home’s fair market value and confirms the property meets the VA’s Minimum Property Requirements (MPRs). VA appraisals were completed in an average of 6.8 business days in fiscal year 2024, a turnaround time that has improved notably in recent years and is now broadly comparable to conventional appraisal timelines in most markets.

If the home appraises at or above the purchase price and meets MPRs, the process proceeds to underwriting and then closing. If it appraises below the purchase price, you have three options: negotiate the price down with the seller, pay the difference in cash, or walk away under the VA’s escape clause without losing your earnest money. That escape clause is a protection most conventional buyers do not have by default.

The VA’s Tidewater Initiative allows appraisers to request additional comparable sales data before completing a low appraisal. If your lender or agent gets a Tidewater notice, it is an early signal, not a final decision, and provides an opportunity to submit supporting comps before the appraisal is finalized.

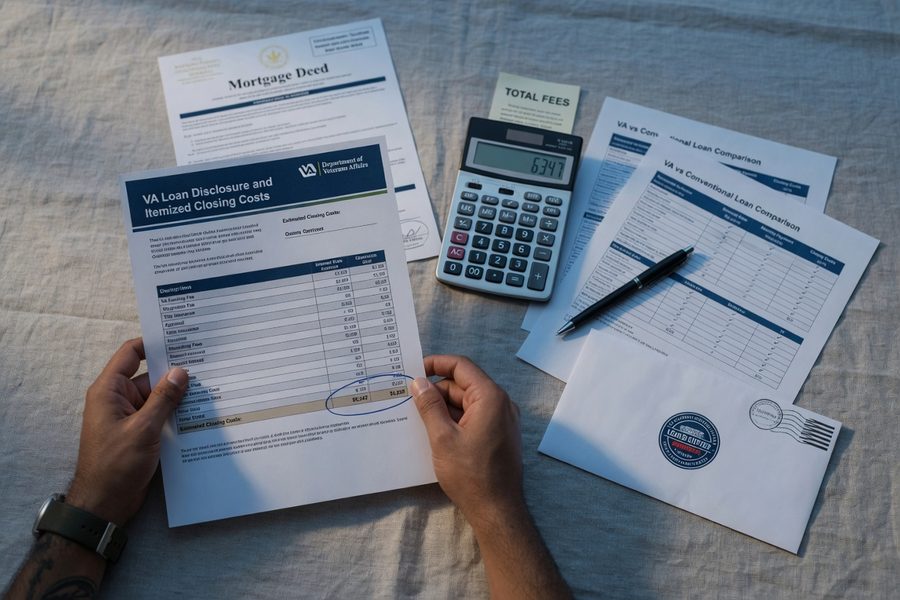

Closing Costs and What Sellers Can Pay

VA loans restrict what fees lenders can charge borrowers (the “non-allowable fees” rule), which generally keeps closing costs lower than conventional alternatives. Buyers still pay for items like the appraisal, title insurance, recording fees, and prepaid interest, but certain origination charges and junk fees are prohibited. Sellers can contribute up to 4% of the loan amount in concessions, which can cover the funding fee, prepaid taxes and insurance, or even outstanding debt balances. In a buyer-friendly market, negotiating seller concessions is a straightforward way to arrive at closing with minimal cash out of pocket.

Qualification Standards Lenders Actually Use

The VA does not set a minimum credit score for its loan guarantee. Program guidelines focus heavily on residual income, a measure of how much money a borrower has left over each month after paying all debts and living expenses, rather than relying on a strict debt-to-income ratio (DTI) alone. In practice, however, lenders impose their own overlays. Most VA-approved lenders require a minimum FICO Score of 620 for a smooth approval, though some lenders work with scores as low as 580 with compensating factors. Lenders like SoFi and Rocket Mortgage publish their specific minimums; it is worth checking before you apply, since overlays vary considerably across institutions.

How Residual Income Works

Residual income is one of the VA loan program’s most distinctive features, and one of its least understood. After calculating your proposed monthly mortgage payment, all other monthly debts, taxes, insurance, and estimated maintenance costs (typically $0.14 per square foot of the home), the VA requires a specific dollar amount to remain. These minimums vary by region and family size.

As a rough example: a family of four in the South purchasing a 1,800-square-foot home must have at least $1,003 remaining per month after all obligations. In the Northeast, that floor is $1,025. These figures are conservative; most buyers comfortably exceed them. The calculation can create complications, though, for buyers carrying high consumer debt or sporadic military pay structures. If you are carrying significant credit card debt heading into a VA loan application, paying down balances before applying can materially improve your residual income picture, and it will also improve the FICO Score that Experian, Equifax, and TransUnion report to lenders.

How BAH and Military Allowances Factor In

BAH, BAS, and similar tax-free military allowances are fully countable as qualifying income under VA guidelines. Because these allowances are not taxed, lenders often gross them up by approximately 25% when calculating income, meaning a $1,500 monthly BAH might be treated as $1,875 in qualifying income. For active duty members stationed in high-cost-of-living areas, this adjustment can be the difference between qualifying for the home they want and being pushed into a smaller price range. Make sure your lender documents and includes these correctly from the start; errors here are more common than they should be.

If your FICO Score sits between 580 and 619, do not assume you are disqualified. Some VA-specialized lenders work in that range with compensating factors such as strong residual income, substantial cash reserves, or a long history of on-time rent payments. Shop at least two or three lenders before accepting a denial.

VA Appraisal Standards vs. Conventional: What First-Timers Need to Know

The VA appraisal process is frequently misunderstood, and misrepresented. A common claim is that VA appraisals are stricter and more likely to kill deals than conventional appraisals. The reality is more nuanced. VA appraisers assess value using the same basic methodology as conventional appraisers: comparable sales, location adjustments, and condition. The key difference is the Minimum Property Requirements (MPRs).

What the VA’s Minimum Property Requirements Cover

MPRs are designed to ensure the home is safe, sound, and sanitary, the VA’s three S’s. Common issues that trigger MPR flags include: exposed wiring or electrical hazards, a roof with less than two years of remaining life, evidence of active pest infestation, broken windows, missing handrails on stairs, and peeling lead-based paint in homes built before 1978. These are not cosmetic concerns; they are health and safety standards that the Consumer Financial Protection Bureau (CFPB) and VA alike consider essential to responsible lending.

| Issue Type | VA Appraisal Impact | Conventional Appraisal Impact |

|---|---|---|

| Peeling paint (pre-1978 home) | Repair required before closing | Noted; typically not required to close |

| Roof condition (under 2 years remaining) | Repair or replacement required | Flagged; buyer discretion |

| Exposed electrical wiring | Repair required before closing | Noted; subject to lender’s judgment |

| Active pest infestation | Treatment required; inspection report needed | Varies; often buyer’s choice |

| Structural concerns | Engineering inspection may be required | Noted; flagged for buyer review |

When MPR issues arise, the seller can make the repairs, the buyer can request the seller credit money toward repairs at closing, or the buyer can pay for repairs directly. In competitive markets where sellers resist repair demands, VA buyers sometimes direct their seller concession allowance toward repair costs rather than asking for a price reduction. That is a practical workaround, but it requires a VA-experienced agent who knows to structure the offer that way from the start.

Seller Concessions and How They Work With a VA Loan

VA loan rules permit sellers to contribute up to 4% of the loan amount in concessions toward the buyer’s costs. On a $350,000 purchase, that ceiling is $14,000. Concessions can cover the funding fee, prepaid property taxes, homeowner’s insurance escrow, discount points to buy down the APR, or even the payoff of existing debt balances. This last option, using seller concessions to pay off buyer debt, is unusual in the mortgage world but explicitly allowed under VA guidelines, and it can be a creative tool for buyers whose DTI needs improvement.

In a slow market or a motivated-seller situation, negotiating the full 4% in concessions means arriving at closing with virtually no out-of-pocket expense beyond the home inspection fee. That scenario is not a loophole; it is the program functioning exactly as designed for buyers who lack the reserves that civilian buyers with longer savings histories might have.

With a 4% seller concession on a $350,000 VA purchase, a buyer could receive up to $14,000 toward closing costs, more than enough to cover the $7,525 funding fee (at 2.15% for first-time use with 0% down) plus prepaid taxes and insurance escrow at most price points.

Potential Roadblocks and How First-Timers Overcome Them

First-time VA loan users most commonly hit problems in three areas: appraisal outcomes that require repairs, finding lenders and agents who actually understand military-specific nuances, and timing pressures created by PCS orders or deployments.

Property Condition Issues

Older homes, particularly those built before 1978, are the most frequent source of VA appraisal complications. Lead paint, outdated electrical panels, deteriorating roofs, and foundation concerns all appear at higher rates in pre-1980 housing stock, which makes up a significant share of inventory in many military-adjacent markets. The solution is not to avoid older homes entirely, but to price the repair risk into your offer. A buyer’s inspection before the VA appraisal gives you leverage to request seller repairs or price reductions before the appraiser flags the same issues. If you find a property you love that has known condition problems, negotiate accordingly from the offer stage, do not wait for the appraiser to surface them.

Finding the Right Lender and Agent

Not every mortgage lender who is technically VA-approved has meaningful experience processing VA loans. The difference shows up in how accurately they calculate residual income, how efficiently they order and track the appraisal, and whether they understand how deployment income, hazardous duty pay, or gap employment from military transitions affects underwriting. Ask prospective lenders directly: how many VA loans did you close last year? What percentage of your total volume is VA? Experienced VA lenders will answer confidently with specific numbers.

The same logic applies to real estate agents. A military buyer relocation specialist, ideally one with a Military Relocation Professional (MRP) designation, understands VA offer strategies, knows how to communicate with listing agents about VA financing concerns, and can structure offers that account for appraisal contingencies without putting you at a disadvantage in a competitive situation. If you are building income as a military family, perhaps picking up extra work as described in our guide to $19+ hourly jobs available in early 2026, a knowledgeable agent helps ensure that income is documented correctly for your loan file.

PCS and Deployment Timing

Permanent Change of Station (PCS) orders create a specific challenge: you may be trying to buy a home at a new duty station before you have started work there, or while wrapping up your current assignment. VA guidelines allow buyers to qualify based on income they will receive at their new duty station, provided the orders are documented. Your lender needs a copy of the official orders, and the income must be verifiable. Deployments add another layer; a power of attorney can allow a spouse or designated representative to complete the purchase in your absence, though lenders and title companies have specific requirements for how that POA must be structured. Plan ahead, do not assume any POA document is sufficient.

| Loan Type | Down Payment Required | Monthly PMI | Loan Limits (Full Entitlement) |

|---|---|---|---|

| VA (First-Time Use) | $0 | None | None |

| FHA | 3.5% (with 580+ score) | 0.55%–1.05% annually | $524,225 (2025 baseline) |

| Conventional (5% down) | 5% | 0.5%–1.5% annually | $806,500 (2025 conforming) |

| Conventional (20% down) | 20% | None | $806,500 (2025 conforming) |

What Happens After You Use the Benefit the First Time

Using the VA loan benefit for the first time does not exhaust it permanently. Once you sell the home and pay off the VA loan, your entitlement is fully restored and available for a subsequent purchase, again with no down payment and no loan limits, but at the higher subsequent-use funding fee of 3.3%. If you buy again while still carrying the original VA loan, you may be able to use remaining entitlement for a second simultaneous VA loan in some circumstances, though this gets complex and typically requires a VA-approved lender with specific expertise in entitlement calculations.

The VA notes that first-time users typically have full basic entitlement available without prior restrictions, and that this entitlement can be restored after loan payoff or in certain other qualifying situations. Treat the first use as the beginning of a long-term housing strategy, not a one-time event. If you are thinking ahead about broader financial planning that includes homeownership, our overview of how to start investing with zero experience pairs well with the equity-building potential that owning a home provides over time.

Veterans with a remaining entitlement amount (rather than full entitlement) can still use the VA loan benefit, but they may be subject to loan limits in their county and may need a down payment if the purchase price exceeds those limits. First-time users with no prior VA loan avoid this complexity entirely.

| Use of VA Loan Benefit | Funding Fee (0% Down) | Funding Fee (5%+ Down) | Entitlement Status |

|---|---|---|---|

| First Use | 2.15% | 1.50% | Full, no loan limits |

| Subsequent Use | 3.30% | 1.50% | Full (if restored) or partial |

| Service-Connected Disability | 0% (exempt) | 0% (exempt) | Full, no loan limits |

Real-World Example: Army Sergeant Purchasing a Home Near Fort Liberty

Consider an illustrative example: a Sergeant with eight years of active duty service, never previously used the VA loan benefit, and is purchasing a home near their current duty station. The purchase price is $320,000. They have a 640 FICO Score, $8,000 in savings, and a monthly income of $5,200 including base pay plus BAH. Their only monthly debt obligations are a $380 car payment and a $120 student loan payment.

Under a conventional loan with 5% down, they would need $16,000 at closing, plus PMI of approximately $175 per month (at 0.65% on the $304,000 balance). Their monthly mortgage payment at 7.0% on the conventional loan would be approximately $2,023 plus $175 PMI, totaling $2,198 before taxes and insurance. They do not have the $16,000 needed, so this path is effectively closed without additional savings.

On a VA loan with 0% down and a 6.5% rate (reflecting the typical VA rate advantage), the loan amount is $320,000 plus the 2.15% funding fee ($6,880), for a financed total of $326,880. Monthly principal and interest comes to approximately $2,067, with no PMI. Compared to the conventional payment of $2,198 (PI only, before PMI), the VA loan saves $131 per month in payment alone, plus the $175 in PMI they would have owed. Total monthly savings: $306. Over five years, that is $18,360 in retained cash flow, before accounting for the $16,000 down payment they never had to pull out of savings.

In this scenario, the VA funding fee financed into the loan costs roughly $15,000 in total interest over 30 years at 6.5%. The 2026 tax deduction on the $6,880 fee saves approximately $1,514 at the 22% bracket in year one, per IRS Publication 936. The net effective cost of the funding fee, accounting for that deduction, is closer to $5,366, a cost fully offset by less than 18 months of PMI savings. By any reasonable measure, the VA loan is the stronger financial choice for this buyer.

Your Action Plan

-

Confirm Your Eligibility Before Shopping

Pull your DD-214 if you are a veteran, or gather your current orders and service documentation if active duty. Cross-reference your service dates and length against the VA’s published eligibility criteria at VA.gov. If you are not certain about qualifying service periods or discharge characterization, contact a VA regional loan center directly, they provide free eligibility guidance with no obligation to proceed.

-

Request Your Certificate of Eligibility

Apply for your COE through the VA’s eBenefits portal, or ask a VA-approved lender to pull it on your behalf through the automated system. Most lenders retrieve it in under 24 hours. Having the COE in hand strengthens your position with sellers and confirms to your lender that your entitlement is clear and available for first-time use. If you have any outstanding credit card balances, addressing them now, before you apply, can also sharpen your residual income picture, as our breakdown of how credit card debt affects household finances explains in more detail.

-

Shop at Least Three VA-Approved Lenders

Interest rates and lender fees vary more than most buyers expect. On a $320,000 VA loan, a 0.25% rate difference saves roughly $17 per month and over $6,000 over 30 years. Request a Loan Estimate (the standardized federal disclosure form) from each lender so you are comparing on identical terms. Pay specific attention to how each lender counts your BAH and BAS; differences in how they handle allowances can shift your qualifying amount by tens of thousands of dollars. Lenders like Veterans United, USAA, and Navy Federal each have different overlays, and comparing APRs across all three is worth the time.

-

Get Pre-Approved and Understand Your Numbers

Pre-approval (not just pre-qualification) puts you in a strong position with sellers. Ask your lender to walk you through the residual income calculation for your specific family size and region, not just whether you meet it, but by how much. Knowing your buffer helps you understand your true purchasing power. Also confirm whether you qualify for the funding fee exemption; if you have any service-connected disability rating at all, verify this directly with the VA before closing, since exemption status confirmed after closing does not automatically trigger a refund without proactive follow-up.

-

Hire an Agent With Documented VA Experience

Ask agents directly how many VA transactions they closed in the past 12 months and whether they hold an MRP designation. A VA-experienced agent knows how to write offers that address seller concerns about VA financing, how to negotiate MPR repairs without killing a deal, and when to use seller concessions strategically. In competitive markets where multiple offers are common, your agent’s ability to present your VA offer compellingly often matters more than the loan program itself. If you need to bolster your financial position before buying, perhaps by adding income streams, our guide to turning seasonal skills into cash offers practical starting points.

-

Review the VA Appraisal Results Carefully and Act Fast

When the VA appraisal comes back, review it the same day it is received. If MPR issues are flagged, immediately discuss the repair options with your agent, seller repair request, seller credit, or buyer-paid repair, and move to resolution quickly. Most VA appraisal complications are solvable; the deals that fall apart are usually those where the parties took too long to respond. If the appraisal comes in below the purchase price, use the VA escape clause if needed; you are not obligated to proceed, and you will not lose your earnest money.

Frequently Asked Questions

Do I need a down payment to use a VA loan for the first time?

No. First-time VA users with full entitlement can purchase a home with zero down payment, regardless of the purchase price, as long as the home appraises at or above the purchase price and the borrower qualifies financially. The VA’s Home Loan Guaranty Buyer’s Guide confirms that first-time homebuyers with full entitlement can enjoy VA backing with no down payment and no loan limits under qualifying conditions.

What credit score do I need for a VA loan?

The VA itself sets no official minimum credit score. In practice, most VA-approved lenders require at least a 620 FICO Score for standard approval. Some lenders work with scores in the 580–619 range with strong compensating factors, particularly high residual income or substantial cash reserves. A score below 580 will face significant challenges with most lenders, though the program’s residual income focus means that creditworthiness is assessed more holistically than with conventional loans. Checking your credit report through Experian, Equifax, or TransUnion before applying can help you catch errors that are dragging your score down.

Can I use the VA loan benefit if I have owned a home before?

Yes. Prior homeownership does not affect VA loan eligibility. What matters is whether you have used the VA loan benefit before, not whether you have owned property through other financing. A veteran who purchased five homes using conventional financing retains their full, never-used VA entitlement and qualifies as a first-time VA user.

How long does the VA loan process take compared to a conventional loan?

The overall timeline is broadly comparable, typically 30 to 45 days from application to closing. VA appraisals averaged 6.8 business days to complete in fiscal year 2024, which is competitive with conventional appraisal timelines in most markets. The main variable is how experienced your lender and agent are with VA-specific requirements. An inexperienced team can add two to three weeks of unnecessary delay; a seasoned VA team keeps the process moving efficiently.

Is the VA funding fee refundable?

In certain circumstances, yes. If a veteran pays the funding fee and later receives a VA disability rating that would have qualified them for an exemption at the time of closing, they may be entitled to a refund of the fee. This requires proactive follow-up with the VA, it does not happen automatically. Veterans who believe they may have a pending disability claim should discuss timing with a VA-accredited claims agent before closing.

Can I use the VA loan to buy a multi-family property?

VA loans can be used to purchase properties with up to four units, provided the borrower occupies one of the units as their primary residence. This is a meaningful opportunity for military buyers interested in generating rental income while building equity. Lenders will typically count a portion of projected rental income from the other units when calculating your qualifying income, though documentation and experience requirements vary by lender.

What happens to my VA loan benefit if I sell the home?

Once you sell the home and the VA loan is paid in full, your entitlement is restored and available for a future VA purchase. The restoration is not automatic in all cases, you may need to request it formally through the VA with documentation of the payoff. After restoration, you have full entitlement again, but subsequent-use funding fees apply (3.3% with 0% down versus the 2.15% you paid the first time).

Do VA loans require mortgage insurance?

No, and this is one of the program’s most financially significant features. There is no monthly private mortgage insurance requirement on a VA loan, regardless of how much you put down. The VA’s guaranty to the lender replaces the function that PMI serves on conventional loans. The one-time funding fee is the program’s substitute for ongoing mortgage insurance, and for most buyers it is substantially less expensive over time.

Can surviving spouses of veterans use the VA loan benefit?

Eligible surviving spouses, specifically, unremarried spouses of veterans who died in service or from a service-connected disability, and certain remarried spouses who meet age requirements, can use the VA home loan benefit. Surviving spouses who remarried on or after December 16, 2003, and who were at least 57 years old at the time of remarriage, may still qualify. The rules for surviving spouse eligibility are more nuanced than for veterans and service members; contact the VA directly or work with a VA-accredited attorney or claims agent to confirm your specific status before beginning the purchase process.

Is the VA loan a good option if I plan to move in three to five years due to PCS orders?

It can be, but the short time horizon deserves careful analysis. If you finance the funding fee into the loan, you start with slightly more debt than the home’s purchase price. In a flat market with a short hold period, you may sell before the home appreciates enough to cover selling costs and the financed fee. The stronger argument for using the VA benefit even on a short-term basis is the monthly savings: no PMI and a lower rate mean your monthly payment is lower than it would be with conventional financing, which frees up cash during the assignment. Many military families also convert their first VA-purchased home into a rental property when PCS orders arrive, retaining the asset and continuing to build equity remotely. Planning ahead with solid financial habits, including keeping long-term savings priorities in order, helps ensure that a short-horizon VA purchase remains a net positive decision.

Sources

- U.S. Department of Veterans Affairs, VA Home Loan Eligibility Requirements

- Veterans Benefits Administration, VA Home Loans Overview

- U.S. Department of Veterans Affairs, VA Home Buying Process

- Veterans Benefits Administration, VA Home Loan Guaranty Buyer’s Guide

- U.S. Department of Veterans Affairs, VA Home Loan Limits and Entitlement

- U.S. Department of Veterans Affairs, VA Home Loans: No Down Payment Statistic

- U.S. Department of Veterans Affairs, Surviving Spouses and VA Home Loans (Appraisal Turnaround Data)

- NewDay USA, VA Loan Statistics 2026: By the Numbers (First-Time Buyer Volume, FY2024)

- Internal Revenue Service, Publication 936: Home Mortgage Interest Deduction (Funding Fee Deductibility)

- Urban Institute, Housing Finance at a Glance: Monthly Chartbook