Fact-checked by the MyFinancial101 editorial team

Quick Answer

Managing your finances after quitting your job without another offer requires immediate action across five fronts: calculate your true monthly burn rate, secure health insurance within 60 days, verify unemployment eligibility (most voluntary quits are denied), cut spending to essentials, and set a hard timeline before savings run out. Most job searches take 6–9 months or longer when you’re already unemployed.

Leaving a job without another one lined up is one of the fastest ways to put real pressure on your finances, and the damage compounds quickly if you don’t act in the first two weeks. Managing your finances after quitting your job requires more than a vague plan to “figure it out”; it requires knowing your exact monthly burn rate, understanding which benefits vanish on your last day, and facing some uncomfortable truths about unemployment eligibility and job search timelines. According to the U.S. Bureau of Labor Statistics, roughly 3.0 million Americans voluntarily left their jobs in April 2026 alone, a figure that signals how common this decision is, even if the financial aftermath catches most people off guard.

The timing matters more in 2026 than it did a few years ago. Hiring has slowed in several sectors, inflation has kept essential costs elevated, and many employers are openly favoring candidates who are currently employed over those with a gap. That doesn’t mean quitting without a backup plan is always the wrong call, toxic environments, health impacts, and family demands are real, but it does mean the financial runway you have is shorter and more fragile than most people estimate when they hand in their notice.

This guide walks through every financial consequence of a voluntary quit, in the order you’ll likely encounter them. If you quit last week or are still weighing the decision, the steps here will help you protect what you’ve built, avoid the mistakes that extend a gap into a financial crisis, and find your footing faster.

Key Takeaways

- 3.0 million Americans quit their jobs voluntarily in April 2026, according to BLS Job Openings and Labor Turnover data, making this one of the most common financial transitions adults face.

- Only 46% of Americans have enough emergency savings to cover three months of expenses, per Bankrate’s 2026 Emergency Savings Report, meaning most people who quit have less runway than the standard advice assumes.

- 24% of Americans have no emergency savings at all, according to the same Bankrate 2026 report, a situation that makes a voluntary quit immediately precarious without a plan.

- Most states deny unemployment benefits to voluntary quits unless the worker can prove “good cause” connected to the job itself, personal burnout, a better opportunity, or general dissatisfaction typically does not qualify.

- COBRA continuation coverage costs up to 102% of the full premium, including the portion your employer previously paid, and is one of the largest surprise expenses in the first month after leaving.

- Job searches average 6–9 months, and searches conducted while already unemployed frequently take two to three times longer than those conducted from a currently employed position, based on recruiter and career site data.

In This Guide

- Step 1: What to Do With Your Money in the First 30 Days

- Step 2: Health Insurance and Benefits, The Hidden Monthly Hit

- Step 3: How Long Does Your Emergency Fund Actually Last?

- Step 4: Unemployment Benefits After a Voluntary Quit

- Step 5: Job Search Realities in 2026 and Their Real Costs

- Step 6: Debt, Credit, and Long-Term Wealth Erosion

- Step 7: Side Income and Financial Recovery

- Frequently Asked Questions

Step 1: What to Do With Your Money in the First 30 Days

The first month after your last paycheck sets the financial tone for everything that follows. Before you update your resume or take a week to decompress, sit down and account for every dollar that will leave your accounts in the next 30 days, because many of those charges will arrive before you’ve had time to think clearly about them.

How to Do This

Start by pulling three months of bank and credit card statements and tallying your average monthly spend by category. Most people underestimate this number by 20–30% because they forget annual charges (insurance premiums, subscriptions billed yearly, professional memberships) that can hit at any time. Once you have the real figure, separate it into two lists: non-negotiable essentials, rent or mortgage, utilities, groceries, minimum debt payments, insurance, and everything else. Streaming services, gym memberships, dining out, and delivery apps move to a secondary list that you pause or cancel immediately. Free resources can fill some of those gaps; for example, your local library likely provides free streaming, digital magazines, and more that cost you nothing during the transition.

Contact your creditors proactively. Many lenders offer hardship programs, reduced minimum payments, interest rate freezes, or deferred billing cycles, that are not advertised and require you to call and ask. Document every conversation in writing. The goal at this stage is to buy time without damaging your credit or draining reserves faster than necessary.

What to Watch Out For

Avoid the temptation to treat the initial relief of quitting as permission to spend freely. The psychological lift of leaving a stressful situation is real, but it frequently leads to a week or two of lifestyle spending that your future self will regret. Set a hard spending ceiling on day one, before the emotional high fades.

Open a separate checking account and transfer exactly three months of essential expenses into it before you quit, if you have the option. Treating it as a dedicated “bridge account” makes it far easier to track your true burn rate and resist dipping into reserves for discretionary spending.

Step 2: Health Insurance and Benefits, The Hidden Monthly Hit

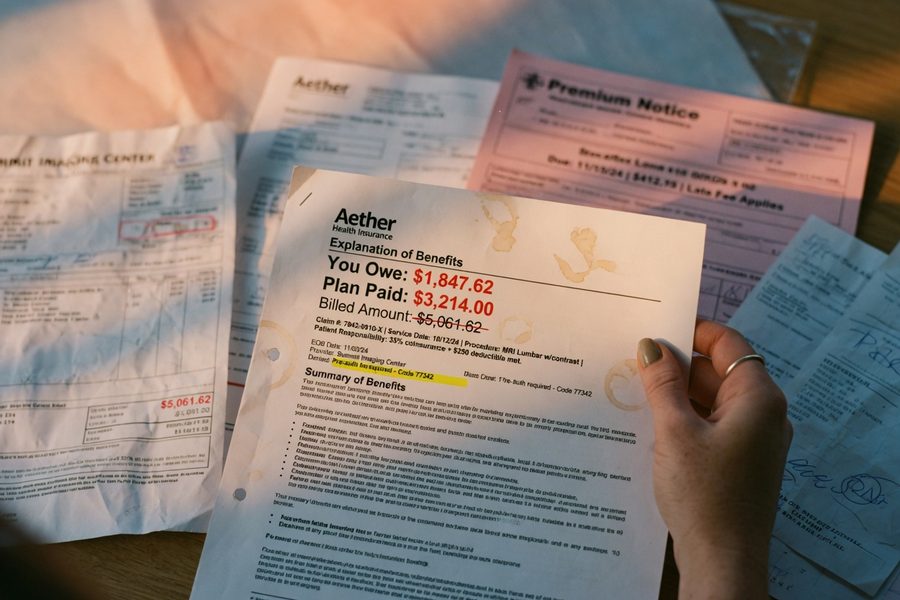

Health insurance is almost always the largest and most time-sensitive financial consequence of leaving a job. Employer-sponsored coverage ends on your last day of employment or the last day of the month in which you quit, depending on your plan, check your HR documents for the exact date, because that window matters.

Your two primary options are COBRA continuation coverage and a plan through the Affordable Care Act (ACA) marketplace at healthcare.gov. COBRA lets you keep your exact current plan, but you’ll pay up to 102% of the full premium, including the portion your employer was covering on your behalf. For a single adult, that can run $500–$700 per month; for a family, $1,500–$2,000 or more is not unusual. You have 60 days from losing coverage to elect COBRA, and coverage is retroactive to the day after your employer plan ended, so you can wait until you actually need care before enrolling, though this is a calculated risk, not a strategy for everyone.

The ACA marketplace, by contrast, prices plans based on your projected annual income for the year. If your income drops significantly after quitting, you may qualify for substantial subsidies, or even Medicaid, depending on your state and household size. A single person earning less than roughly $21,000 in 2026 may qualify for Medicaid in expansion states. Losing job-based coverage is a qualifying life event, which opens a Special Enrollment Period of 60 days. If you have an HSA, those funds remain yours and can continue to cover qualified medical expenses tax-free.

If you have an FSA through your employer, those funds are often forfeited when you leave, unlike an HSA, which you own outright. Use any remaining FSA balance on eligible expenses before your last day: prescriptions, glasses, dental work, or over-the-counter items covered under your plan.

Step 3: How Long Does Your Emergency Fund Actually Last?

Standard personal finance advice says to keep 3–6 months of expenses saved; more conservative guidance pushes that to 12 months if you’re self-employed or in a volatile field. But the real question after quitting isn’t how many months of savings you have, it’s how many months of your actual post-quit burn rate you have.

How to Do This

The arithmetic here is straightforward but frequently gets glossed over. Take your pre-quit monthly expenses and add the costs that were previously invisible: health insurance (let’s say $600/month for a single adult on COBRA), any payroll taxes you were splitting with an employer (relevant if you take any freelance income), and one-time job search costs like resume help, interview clothes, or travel. A person who spent $3,000/month while employed might find their true burn rate is closer to $3,800–$4,200 once those additions land.

Run this worked example: if you have $18,000 saved and your real monthly burn rate is $3,600, your runway is exactly five months, not six, not twelve. At $4,000/month, that same $18,000 lasts four and a half months. The difference between an optimistic estimate and an accurate one can be the difference between finding a job comfortably and accepting the first offer out of panic.

According to Bankrate’s 2026 Emergency Savings Report, only 46% of Americans have enough savings to cover even three months of expenses, and 24% have no emergency savings at all. If you’re in the latter group or the former and close to the edge, the recovery strategies in Step 7 of this guide become critical from day one, not after you’ve been searching for a few months.

What to Watch Out For

Resist the impulse to tap retirement accounts early unless all other options are exhausted. A 10% early withdrawal penalty applies to most 401(k) and traditional IRA distributions before age 59½, on top of ordinary income tax, so a $10,000 withdrawal could net you as little as $6,500 after taxes and penalties, depending on your tax bracket. A Roth IRA is more flexible: contributions (not earnings) can be withdrawn at any time without penalty, making it a last-resort bridge that’s less costly than a traditional 401(k) withdrawal.

24% of Americans have zero emergency savings, according to Bankrate. For those individuals, quitting without a lined-up job requires an immediate income bridge, not just a budget cut.

“If you are relying on unemployment, or drawing down an emergency fund, you’ll want to use a bare bones budget.”

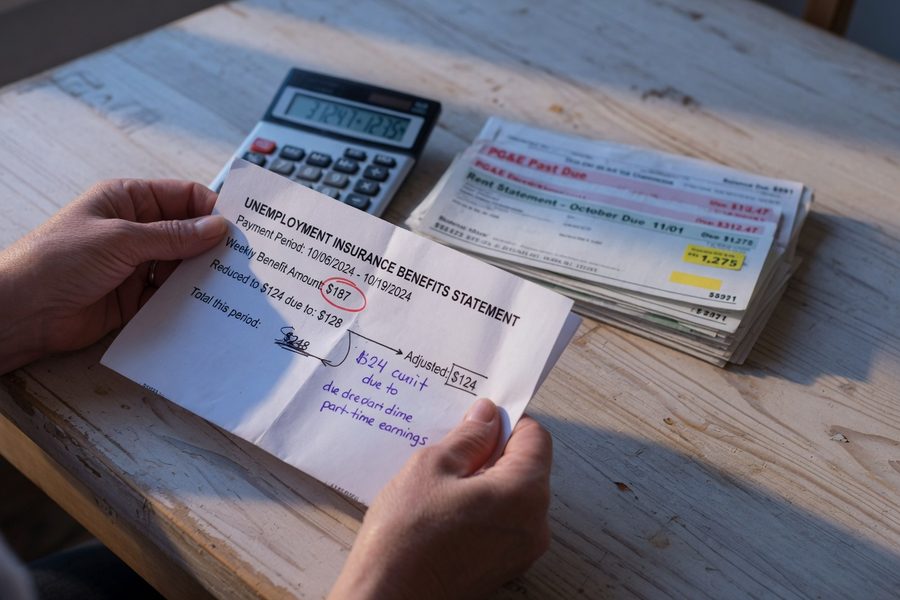

Step 4: Unemployment Benefits After a Voluntary Quit, Why Most Claims Get Denied

Most people who quit voluntarily do not qualify for unemployment benefits, and this assumption, that unemployment is a financial backstop after any job separation, is one of the most expensive misconceptions in personal finance. The reality is state-dependent and far more restrictive than most workers realize.

How to Do This

Every state requires that you demonstrate “good cause” to collect benefits after a voluntary quit, and the bar is specifically tied to conditions at work, not personal circumstances. According to the Washington Employment Security Department, depending on why you quit your job, you might qualify for unemployment benefits if you have good cause, but the ESD sets a high evidentiary standard. Similarly, the Texas Workforce Commission states plainly that most people who quit their jobs do not receive unemployment benefits unless for good cause connected with the work. New Jersey’s Department of Labor is equally direct: workers who leave for personal reasons may not be eligible unless good cause is shown, per NJ Department of Labor and Workforce Development guidelines.

What counts as good cause varies, but courts and agencies have generally accepted: documented harassment or a hostile work environment, a substantial and involuntary reduction in pay or hours, a move required by a spouse’s relocation, or serious medical conditions that made work impossible. Personal burnout, general dissatisfaction, a better opportunity elsewhere, or wanting time off do not qualify in most states. If you believe you have a valid good-cause claim, document everything, emails, HR complaints, medical records, before you file. File your claim anyway, because some states allow a formal appeal process if you’re initially denied.

What to Watch Out For

Even if you qualify for benefits, unemployment insurance replaces only a portion of prior wages, typically 40–50%, and is subject to a weekly maximum that varies by state. Do not build a budget around receiving it before your claim is approved. Treat any benefits as a supplement to your emergency fund, not a replacement for it.

| Reason for Quitting | Typical Unemployment Eligibility | Documentation You’ll Need |

|---|---|---|

| Hostile work environment / harassment | Often qualifies as good cause | HR complaints, emails, witness statements, dates of incidents |

| Pay cut or hours reduction | Often qualifies if substantial (>20% in many states) | Pay stubs, offer letter, written notice of change |

| Spouse relocation / military move | Qualifies in many states | Military orders, lease agreements, relocation documents |

| Medical condition | May qualify with doctor documentation | Physician letter, FMLA denial if applicable |

| General burnout or stress | Rarely qualifies | No documentation typically accepted |

| Better opportunity / career change | Does not qualify | N/A, ineligible in virtually all states |

| Personal reasons / family care | Usually denied unless domestic violence or medical | Documentation varies by state, call your state agency |

Even if your initial unemployment claim is denied after a voluntary quit, most states allow you to appeal within 10–30 days of the denial notice. If you have documented evidence of workplace conditions that forced your departure, an appeal is worth filing, some claimants succeed on appeal who were denied at the initial review stage.

Step 5: Job Search Realities in 2026, Timeline and Hidden Costs

Job searches are almost universally longer and more expensive than people expect, and both problems get worse when you’re searching from an unemployed position rather than a currently employed one.

How to Do This

The broad consensus among career sites and recruiters in 2026 is that a job search averages 6–9 months, and can easily stretch to 12 months or more for mid-to-senior roles in slower markets. Candidates who are currently employed tend to receive more callbacks and better initial offers; the perception that someone is “choosing” to leave carries more social proof than a gap on a resume. This is not a universal rule, but it’s common enough to factor into your financial plan. Budget for the longer end of the range, and set a milestone: if you’re at month four with no offers, it’s time to reassess strategy, not just keep applying.

The direct costs of job searching add up fast: professional resume review ($100–$300), LinkedIn Premium ($40/month), interview clothing if your wardrobe needs updating ($200–$500), and travel for in-person interviews ($50–$300 per round trip). None of these appear in a standard monthly budget. If you’re looking to generate cash during the gap, hourly jobs paying $19 or more are still available in 2026 across several sectors and can bridge income without derailing a professional search.

What to Watch Out For

Resume gaps affect more than just callbacks. Some employers, especially in finance, government contracting, and healthcare, ask about gaps explicitly, and a vague answer can hurt you in salary negotiations even after you receive an offer. Have a clear, confident narrative ready: whether you were addressing a personal matter, caregiving, or making a deliberate career transition, prepare the short version before you need it in a room.

Career advisors consistently flag one specific risk with unplanned time off: people who quit intending to take a few months to regroup often find that “a few months” expands without a hard end date on the calendar. The financial damage of a nine-month gap versus a three-month one is not proportional, it compounds, as retirement contributions pause, credit utilization climbs, and the psychological pressure to accept any offer grows. Set a specific date, not a vague intention, for when active applications begin, and treat it as a commitment.

Step 6: Debt, Credit, and Long-Term Wealth Erosion

A period of reduced income puts existing debt in a new light, and the decisions you make during the gap have consequences that outlast the gap itself.

How to Do This

While your income is interrupted, focus on making at least the minimum payment on every account to protect your credit score. Missing a payment by 30 days or more triggers a derogatory mark that stays on your credit report for seven years and can push your score down by 60–110 points, according to general FICO impact data, which, in practical terms, means higher interest rates on every future loan, lease, or credit card you apply for. If you’re carrying high-interest credit card debt, review how to prioritize and negotiate with creditors during a low-income period, many issuers will work with you before you miss a payment, not after.

On the wealth side, every month without retirement contributions is compounding interest you don’t earn. If you were contributing $500/month to a 401(k) and take nine months off, the lost contribution alone is $4,500, but the compounded growth loss at a 7% average annual return over 20 years is closer to $17,000. That’s a real, calculable cost of the gap that rarely appears in the initial “I’ll be fine” math people do when they quit. Pausing contributions isn’t always avoidable, but knowing the true cost makes the decision to return to them as quickly as possible much easier to prioritize.

What to Watch Out For

High credit utilization, using more than 30% of your available credit limit, can hurt your credit score even without a missed payment. If you’re charging essentials to a card because cash is tight, monitor your utilization weekly using your card issuer’s app. Paying a partial amount mid-cycle, before the statement closes, can keep utilization lower and protect your score during a tight period. If you’re feeling pressure from existing card balances, you may also be able to negotiate your credit card APR directly, a call that costs nothing and can meaningfully reduce the cost of carrying a balance.

Early 401(k) withdrawals before age 59½ carry a 10% penalty plus ordinary income tax. A $10,000 withdrawal in the 22% federal tax bracket nets you roughly $6,800 after penalties and taxes, less if you owe state income tax. Exhaust all other options first, including Roth IRA contributions (which can be withdrawn penalty-free) and personal loans with lower effective costs.

Step 7: Side Income and Financial Recovery After Quitting

Bridging the income gap while job searching keeps your financial position stable enough that you can afford to wait for the right offer instead of accepting the first one out of desperation.

How to Do This

Freelance consulting in your field is the highest-return option if you have marketable skills: it pays well, reinforces your resume, and produces networking contacts. The micro-freelancing market has grown significantly, making it feasible to pick up short, project-based work without committing to a client relationship that conflicts with a job search. Platforms like Toptal, Upwork, and industry-specific networks (Catalant for business professionals, Expertly for consultants) can surface paid work within days of signing up if your profile is strong.

For more immediate cash flow, hourly and gig work, delivery, tutoring, event staffing, doesn’t require a ramp-up period and can be adjusted around interview schedules. If you’re open to it, local school and event jobs that require no prior experience can fill gaps in a weekly schedule without demanding long-term commitment.

Tax Implications to Keep Straight

Any self-employment or freelance income during the transition year creates a tax obligation that doesn’t come with automatic withholding. If you earn more than $400 from freelance work in a calendar year, you owe self-employment tax (currently 15.3% on net earnings up to the Social Security wage base) on top of ordinary income tax. Pay estimated quarterly taxes, due in April, June, September, and January, to avoid an underpayment penalty at filing. Keep every receipt for job search expenses; some costs (professional development, resume services related to your current field) may be deductible.

What to Watch Out For

Once you’re re-employed, rebuild your emergency fund before adding back discretionary spending. The instinct to reward yourself after a stressful gap is understandable, but a second gap, whether by choice or by layoff, hits far harder without reserves. Automate a fixed transfer to savings on the same day as each paycheck, making the rebuild a default rather than a monthly decision.

If your new job comes with a 401(k) match and you were pausing contributions during the gap, contribute at least enough to capture the full employer match from day one. A 50% match on the first 6% of salary is an immediate 50% return on that portion of your paycheck, no investment carries that guarantee.

Frequently Asked Questions

Can I get unemployment if I quit my job because of stress or burnout?

In most states, quitting due to stress or burnout does not qualify as good cause for unemployment benefits. State agencies require that the cause be connected to actual working conditions, documented harassment, unsafe environments, or substantial involuntary changes to pay or hours, rather than subjective emotional strain. If your burnout was caused by conditions your employer refused to address after a formal complaint, document everything and file anyway; an appeal may succeed where an initial claim does not.

How much money do I actually need saved before quitting without a job?

Most financial planners recommend 6–12 months of expenses, but calculate based on your real post-quit burn rate, not your current one. Add health insurance (COBRA can run $500–$2,000/month depending on your plan), job search costs, and any annual bills that may fall within the gap. Someone spending $3,500/month pre-quit may have an actual burn rate of $4,500/month, which changes a “six-month cushion” into a four-month runway.

How long does it realistically take to find a new job when you’re unemployed?

Expect 6–9 months as a realistic baseline, and plan for longer if you’re in a specialized field or a slow hiring market. Candidates currently employed receive more callbacks and tend to receive stronger initial salary offers than those with an active gap. Set a hard six-month milestone review, if offers aren’t materializing, it’s time to expand the target role list or geographic range, not simply wait longer.

Is COBRA worth it, or should I go with an ACA marketplace plan?

COBRA is worth it when continuity of care is critical, ongoing treatment, specific providers in network, or specialty medications, because you keep your exact plan without interruption. For most healthy adults whose income drops significantly after quitting, an ACA marketplace plan with income-based subsidies will cost substantially less per month. Compare quotes at healthcare.gov before defaulting to COBRA; a subsidized silver-level plan may cost a fraction of COBRA’s full premium.

What happens to my 401(k) when I quit my job?

Your vested 401(k) balance belongs to you and stays in the account after you leave. You have several options: leave it in your former employer’s plan (check for administrative fees), roll it into a new employer’s 401(k) when you’re rehired, or roll it into an individual IRA without triggering taxes or penalties. Avoid cashing it out, doing so before age 59½ costs you a 10% early withdrawal penalty plus ordinary income tax on the entire amount, often reducing a $10,000 withdrawal to $6,500 or less in hand.

Can I negotiate severance if I quit voluntarily?

Severance is generally not owed to voluntary quits under U.S. law, but negotiation is not off the table in every case. If you have an employment contract, check whether it specifies any separation payment. In some situations, particularly if you’re leaving due to working conditions the employer wants to avoid publicizing, a mutual separation agreement that includes a small severance in exchange for a non-disparagement clause is possible. Ask before assuming the answer is no, but go in with realistic expectations.

Will quitting without a job lined up hurt my credit score?

Quitting itself has no direct effect on your credit score, employment status does not appear on credit reports. The indirect risks are what matter: missing a payment by 30+ days, allowing credit utilization to exceed 30%, or taking on new high-interest debt to cover expenses can all cause meaningful score damage. Proactively managing minimum payments and calling creditors before you miss anything gives you the best chance of exiting the gap with your credit score intact. Resources like those on top credit counseling services can help you build a plan if debt management feels unmanageable during the transition.

Sources

- U.S. Bureau of Labor Statistics, Job Openings and Labor Turnover Summary (JOLTS), April 2026

- Bankrate, Emergency Savings Report 2026

- Washington Employment Security Department, Unemployment Eligibility When You Quit

- Texas Workforce Commission, Unemployment Benefits Eligibility and Benefit Amounts

- New Jersey Department of Labor and Workforce Development, Quit or Fired Eligibility

- HealthCare.gov, COBRA Coverage and Health Insurance After Job Loss

- The Muse, How to Budget After a Layoff (featuring Amy Coroso, CFEI)

- CNBC, How to Financially Prepare If You Quit With the Intent to Take Time Off (featuring Cady North, CFP)

- IRS, Retirement Topics: Tax on Early Distributions

- U.S. Department of Labor, COBRA Continuation Coverage