Fact-checked by the MyFinancial101 editorial team

Quick Answer

A CD laddering strategy splits a lump sum across multiple CDs with staggered maturities, typically 1 through 5 years, so one CD matures every year. On $80,000 divided equally into five $16,000 rungs, top 2026 rates can generate roughly $3,200–$3,600 in annual interest while keeping principal fully protected under FDIC insurance.

Most retirees hold more cash than they admit, parked in savings accounts earning far less than available CD rates. A CD laddering strategy fixes that directly: instead of locking all your money into a single long-term certificate, you split it across staggered maturities so liquidity returns every 12 months without sacrificing the higher rates that longer terms provide. According to FDIC deposit insurance rules, up to $250,000 per depositor per institution is fully guaranteed, making CDs one of the few income tools that carry essentially zero credit risk.

In a May 2026 environment where sequence-of-returns risk still looms over equity-heavy retirement portfolios, the predictability of a CD ladder matters. This guide walks through a real $80,000 example, including exact allocations, realistic monthly income figures, honest trade-offs, and the mechanics of converting maturing principal into ongoing cash flow without touching the original nest egg.

Key Takeaways

- An $80,000 CD ladder split into five $16,000 rungs maturing annually provides a natural 20% liquidity event each year, no early-withdrawal penalties required (per Bankrate’s CD ladder guide).

- Top 5-year CD rates in early 2026 hovered above 4.00% APY, enabling approximately $3,200–$3,600 in blended annual interest on an $80,000 ladder when averaged across all five terms (per Bankrate’s April 2026 rate survey).

- FDIC insurance covers up to $250,000 per depositor per institution, so an $80,000 ladder held across two or three banks remains fully protected even if a bank fails (per FDIC deposit insurance overview).

- Reinvesting only the interest portion at each maturity preserves the original $80,000 principal indefinitely, sustaining income without depleting the base (per Vanguard’s CD ladder explainer).

- Brokered CDs traded on the secondary market can provide monthly coupon payments, filling the income gap that standard bank CDs, which typically pay at maturity, leave open (per Fidelity’s brokered CD resource).

In This Guide

- Why Retirees Are Turning to CD Ladders for Predictable Income

- One Retiree’s $80,000 CD Ladder: From Lump Sum to Monthly Cash Flow

- How a Standard 5-Rung CD Ladder Actually Works with $80,000

- Realistic Monthly Income Expectations from an $80k Ladder in 2026

- Key Risks and Honest Trade-Offs Retirees Face

- How the Ladder Interacts with Social Security and Taxes

- Practical Steps to Build and Maintain Your Own Ladder Today

Why Retirees Are Turning to CD Ladders for Predictable Income

Sequence-of-returns risk, not average market performance, is what actually breaks retirement plans. A significant drawdown in the first few years of retirement forces you to sell equities at depressed prices, and that damage never fully reverses even if markets recover. CD ladders address this precisely because the principal cannot decline in value; the only variable is the interest rate you lock in at purchase.

For retirees sitting on a lump sum from a pension, an IRA rollover, or the sale of a home, a CD ladder provides something a dividend portfolio cannot guarantee: a fixed, contractual return with a known maturity date. That certainty allows for disciplined budgeting. You know, to the dollar, what each rung will return and exactly when.

The Rate Environment in May 2026

Rates have moderated slightly from 2023 peaks, but top-tier 5-year CDs from online banks and credit unions still offer above 4.00% APY as of spring 2026, according to Bankrate’s current CD rate survey. That is meaningfully above the long-run average savings account rate, which the FDIC’s national rate data has historically pegged well below 1% for most of the 2010s. Retirees who spent that decade in savings accounts and money market funds left significant guaranteed income on the table. The current window, while it lasts, rewards action.

During the decade from 2010 to 2020, the national average savings account rate rarely exceeded 0.10% APY. Retirees who locked into 5-year CDs in 2023 and 2024 captured rates that were literally 40 to 50 times higher than that historical floor.

One Retiree’s $80,000 CD Ladder: From Lump Sum to Monthly Cash Flow

Consider a 68-year-old retiree who rolled over $80,000 from a traditional IRA into a CD ladder in early 2026, choosing to supplement Social Security rather than draw down investments. She divided the funds into five equal $16,000 CDs with terms of 1, 2, 3, 4, and 5 years. The goal was simple: never touch principal, collect interest as income, and reinvest each maturing CD into a new 5-year term to keep the ladder alive.

The mechanics are straightforward. Her 1-year CD matures in early 2027. At that point, she collects the interest earned (roughly $688 at a 4.30% APY, the approximate top 1-year rate in early 2026 per Bankrate), then reinvests the $16,000 principal into a new 5-year CD. She repeats this process every year as each rung matures. Over time, all five rungs will be in 5-year CDs, and the ladder self-perpetuates with one maturity annually.

Converting Annual Maturities into Monthly Cash Flow

One practical challenge: a standard bank CD typically pays interest at maturity, not monthly. This retiree solved it two ways. First, she placed two of her five rungs in brokered CDs purchased through Fidelity’s brokered CD marketplace, which offer monthly coupon payments. Second, she directed annual interest payouts from the remaining three bank CDs into a high-yield savings account and drew from that account in equal monthly installments throughout the year. The result was a synthetic monthly income stream of roughly $270–$300 per month before federal taxes.

How a Standard 5-Rung CD Ladder Actually Works with $80,000

Equal allocations are the standard starting point, and for good reason. Five rungs at $16,000 each create an annual 20% liquidity event: every 12 months, a full rung becomes accessible without any early-withdrawal penalty. That is the structural advantage a single 5-year CD never offers.

The table below shows a sample allocation using rates available to consumers in spring 2026. Rates are illustrative based on top-tier online bank offerings tracked by Bankrate; your specific institution may vary by 0.10–0.30 percentage points.

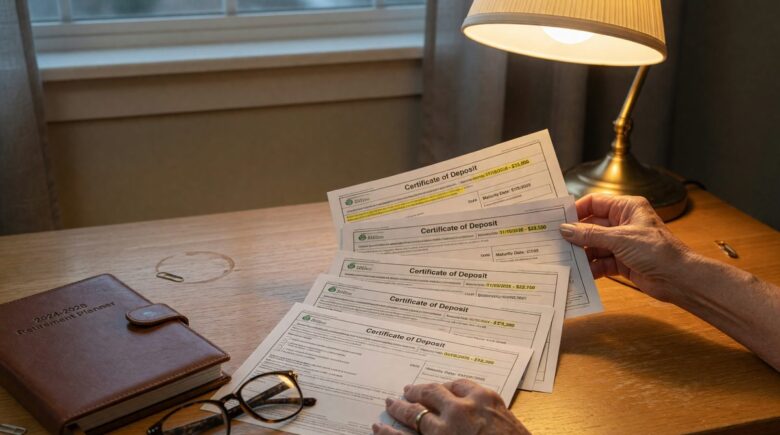

| Rung | Term | Amount | Sample APY | Annual Interest |

|---|---|---|---|---|

| 1 | 1 Year | $16,000 | 4.30% | $688 |

| 2 | 2 Years | $16,000 | 4.20% | $672 / yr |

| 3 | 3 Years | $16,000 | 4.10% | $656 / yr |

| 4 | 4 Years | $16,000 | 4.05% | $648 / yr |

| 5 | 5 Years | $16,000 | 4.00% | $640 / yr |

| Total | $80,000 | 4.13% avg | ~$3,304 / yr |

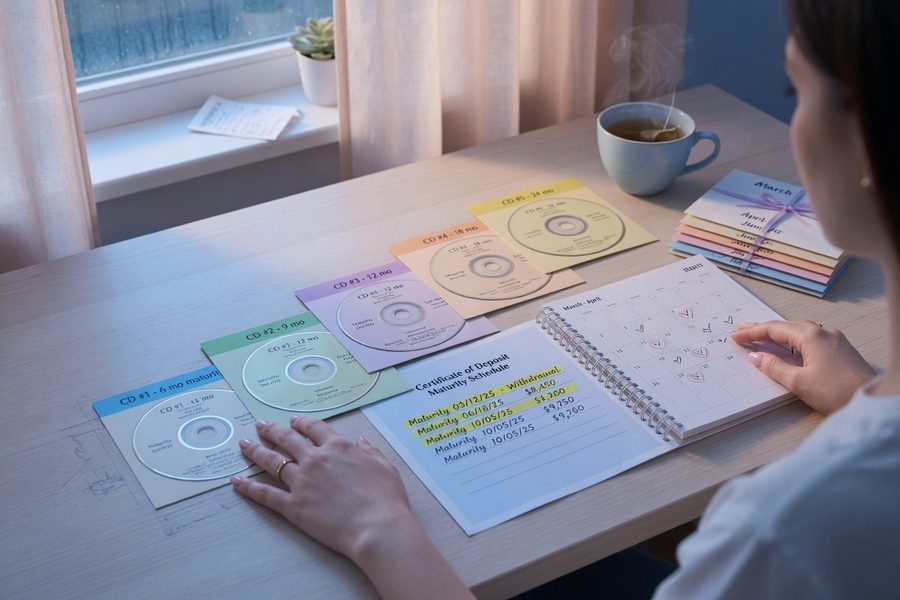

What Happens at Each Maturity

At each annual maturity, you face a fork: reinvest the full $16,000 plus interest into a new 5-year CD (growing the ladder), or pocket the interest and reinvest only the principal. The second option preserves your $80,000 base exactly. Either way, the ladder continues. The only scenario that shrinks principal is spending it, which is a deliberate choice rather than an unavoidable cost of the strategy.

An $80,000 CD ladder at a blended 4.13% APY generates approximately $3,304 per year in interest, or about $275 per month, without touching principal. Compound that interest back into the ladder over five years and the total balance grows to roughly $97,700.

Realistic Monthly Income Expectations from an $80k Ladder in 2026

Gross monthly income of $275–$300 is the realistic base case. That figure rises toward $350–$400 if you hold the longer rungs in top-yielding 5-year CDs and use brokered CDs for the monthly payment schedule described above. What most guides omit is the after-tax figure.

CD interest is taxed as ordinary income at both the federal and, in most states, state level. A retiree in the 22% federal bracket with $3,304 in annual CD interest owes approximately $727 in federal tax, leaving about $2,577, or roughly $215 per month after federal taxes. If you live in a state without income tax on interest (Florida, Texas, and Nevada are among the nine states with no income tax), that number holds. State residents elsewhere lose another $100–$200 annually depending on the rate. This is a real cost that glossy ladder calculators often skip.

Using Brokered CDs for True Monthly Income

Brokered CDs, available through firms like Charles Schwab and Fidelity, pay interest in regular coupon payments, often monthly or semi-annually, rather than at maturity. This solves the timing problem directly. The trade-off: brokered CDs generally offer slightly lower rates than direct-to-consumer bank CDs, and they carry secondary market price risk if you need to sell before maturity. Held to maturity, however, they pay exactly as promised. For income-focused retirees who want genuine monthly deposits, the minor rate difference is often worth it.

Key Risks and Honest Trade-Offs Retirees Face

Three risks deserve direct acknowledgment, not buried footnotes.

First, inflation erosion. At 4% APY, a CD roughly keeps pace with the Federal Reserve’s 2% inflation target, but it does not protect against inflation running hotter, as it did from 2021 through 2023. If prices rise faster than your CD yield, purchasing power quietly shrinks even though your nominal balance grows. Second, reinvestment risk: if rates fall sharply before your shorter rungs mature, you will be rolling $16,000 into a new 5-year CD at, say, 2.50%, cutting annual income nearly in half on that rung. A CD ladder is not immune to rate cycles; it just smooths them. Third, the $250,000 FDIC limit per depositor per institution is not a concern for an $80,000 ladder, but retirees scaling this strategy beyond $500,000 across two banks need to track exposure carefully, as the FDIC’s deposit insurance rules explain in detail.

How the Ladder Interacts with Social Security and Taxes

This is the angle most CD ladder articles miss entirely. CD interest counts as provisional income for Social Security taxation purposes. Under IRS rules, if your combined provisional income (adjusted gross income plus nontaxable interest plus half of Social Security benefits) exceeds $34,000 for single filers, up to 85% of your Social Security benefit becomes taxable, according to the Social Security Administration’s income tax guidance.

For a retiree receiving $18,000 per year in Social Security, $3,304 in CD interest can push provisional income past that threshold depending on other income sources. One mitigation: holding CDs inside a Roth IRA eliminates the interest from provisional income calculations entirely, though Roth CDs at banks are less common than taxable ones. Another option is spacing maturities to control when interest is recognized in a given tax year. If you are also managing broader retirement savings priorities, the tax interaction with Social Security deserves a conversation with a CPA before you build the ladder.

A single filer whose provisional income exceeds $34,000 may have up to 85% of Social Security benefits subject to federal income tax. CD interest counts in full toward that threshold, making tax planning a core part of any CD ladder strategy for retirees.

Practical Steps to Build and Maintain Your Own Ladder Today

Start with rate shopping, not a brand name. Online banks and credit unions consistently offer rates 0.50–1.00 percentage points higher than traditional brick-and-mortar banks on the same CD terms, per Bankrate’s ongoing rate tracking. The National Credit Union Administration’s credit union locator is a free tool for finding federally insured credit unions near you that may offer competitive rates.

Banks, Brokerages, and Staying Organized

Spread your rungs across at least two institutions to stay well under the $250,000 FDIC cap and to avoid having all CDs subject to the same auto-renewal terms. When a CD matures, most banks will auto-roll it into the same term at the current rate, which may not be the best available. Set a calendar alert for 7–10 days before each maturity so you have time to shop and move funds if a better rate exists elsewhere.

For brokered CDs, both Fidelity and Schwab provide inventory screens that let you filter by maturity date, coupon frequency, and yield. You can also find secondary market CDs with maturities of 14 or 18 months, filling gaps that standard bank term options do not offer. If you are new to structured investing, brokerage platforms often provide step-by-step tutorials for purchasing CDs that make the process less intimidating than it sounds.

Pairing the Ladder with a Cash Buffer

A two-year cash buffer held in a high-yield savings account alongside the ladder creates what retirement planners call a “bucket strategy.” The first bucket covers 12–24 months of expenses in liquid cash. The CD ladder occupies the second bucket, refilling the cash buffer annually as rungs mature. This pairing neutralizes the one genuine weakness of CDs: the gap between when you need money and when a CD is scheduled to mature. It is also a natural complement to managing other fixed expenses, similar to how households use tools covered in our guide to managing utility and fixed cost programs to smooth monthly cash needs.

On the tax reporting side: each year you will receive a 1099-INT from every institution holding a CD. If you hold five CDs across three banks, expect three 1099 forms. Interest accrued on multi-year CDs may be reportable annually even if you have not yet received payment, under the IRS’s original issue discount (OID) rules for zero-coupon style products. Standard coupon-paying CDs do not trigger OID reporting. It is a detail worth confirming with each institution before you commit. For broader help navigating retirement-year tax filings, the free IRS tax assistance programs available to retirees can be a practical resource.

Frequently Asked Questions

What is the minimum amount needed to start a CD laddering strategy?

There is no regulatory minimum, but most banks require at least $500–$1,000 per CD. A functional 5-rung ladder is easier to manage with at least $10,000 total, so each rung holds $2,000 or more. Smaller amounts narrow your bank choices and reduce the income enough that a high-yield savings account may be more practical.

Can you build a CD ladder inside an IRA?

Yes, and it can be advantageous. Holding CDs inside a traditional IRA defers taxes on interest until withdrawal; a Roth IRA makes the interest tax-free entirely. The mechanics are the same as a taxable ladder, though you need to coordinate maturities with required minimum distribution rules if you are over age 73.

What happens if you need money before a CD matures?

Breaking a CD early typically triggers an early-withdrawal penalty, commonly 60 to 150 days of interest depending on the term and the institution. On a $16,000 CD, that penalty could run $107–$267 at a 4% APY. Brokered CDs avoid this by allowing secondary market sales, but secondary prices may be below face value if interest rates have risen since you purchased.

How does a CD ladder compare to U.S. Treasury bonds for retirement income?

Treasuries and CDs often carry similar yields on comparable terms, but they differ on two points. Treasury interest is exempt from state income tax, which benefits residents of high-tax states significantly. CDs, by contrast, are FDIC-insured per institution, while Treasuries are backed by the full faith and credit of the U.S. government. For state-tax purposes, Treasuries frequently win; for simplicity and FDIC familiarity, many retirees prefer CDs.

Does CD interest affect Medicare premium calculations?

Yes. Medicare Part B and Part D premiums use income-related monthly adjustment amounts (IRMAA), calculated from your tax return filed two years prior. CD interest raises modified adjusted gross income (MAGI), which can push you into a higher IRMAA tier. On $80,000 of CDs at 4%, the additional $3,300 of annual interest is unlikely to move the needle on its own, but combined with other income sources it can.

Is a CD ladder better than an annuity for guaranteed retirement income?

For most retirees with modest sums, a CD ladder offers more flexibility and full principal recovery at maturity, whereas a fixed annuity typically surrenders principal in exchange for lifetime payments. Annuities can make sense when longevity risk is the primary concern, but they carry surrender charges and lack the FDIC insurance backstop. A CD ladder is the better starting point for retirees who want control over their principal.

How often should you review and adjust a CD ladder?

Review it at every maturity, at minimum once per year. The primary question each time is whether the new 5-year rate justifies re-locking at that term, or whether a shorter extension makes more sense given the rate outlook. Major life changes such as a required minimum distribution increase, a change in Social Security benefits, or a move to a different state also warrant a ladder review outside the normal cycle.

Set a recurring calendar reminder 10 days before each CD maturity. That window gives you enough time to compare current rates on Bankrate or Deposit Accounts, contact your bank about renewal terms, and transfer funds to a higher-yielding institution if rates have shifted in your favor, all before the auto-roll deadline locks you into the same term.