Reviewed by the MyFinancial101 Editorial Team

Our Take

For most workers in the 12% or 22% federal tax bracket today, the Roth IRA wins, paying taxes now at a known, historically moderate rate beats deferring into an uncertain future. The case for the Traditional IRA is strongest when you’re in the 24% bracket or higher right now and have clear reason to expect lower income in retirement. With the Tax Cuts and Jobs Act provisions set to expire after 2025, current brackets may already be the lowest you’ll see for a decade; that shifts the calculus further toward Roth for most middle-income savers.

The Roth IRA vs Traditional IRA question is one of the most consequential decisions a retirement saver can make, and it’s getting more urgent. According to the Investment Company Institute’s 2025 report, 44% of U.S. households owned some type of IRA as of mid-2024, yet most account holders never stress-test their choice against their actual tax trajectory. The decision you make today determines whether your retirement withdrawals are taxed, or completely free.

This article is for workers at any stage who want a defensible framework, not just a vague “it depends.” What makes the recommendation hold is your current and projected tax bracket. What breaks it is a genuinely high income today paired with a certain drop in retirement spending.

Key Takeaways

- 44% of U.S. households owned an IRA in mid-2024, but only 26% owned a Roth IRA, according to ICI’s 2025 data, meaning millions may be defaulting to Traditional without running the numbers.

- The 2026 contribution limit is $7,000 for savers under 50 and $8,000 for those 50 and older, per IRS guidance; both account types share this same annual cap.

- Roth IRA eligibility phases out between $150,000 and $165,000 MAGI for single filers in 2026, per IRS rules, high earners above that threshold must use a backdoor strategy or choose Traditional.

- Traditional IRAs require required minimum distributions (RMDs) starting at age 73, while Roth IRAs have no lifetime RMDs, a structural advantage for heirs and estate planning, per IRS rules.

- In my experience working through these scenarios with readers, the single most overlooked factor is how Roth withdrawals don’t count toward the income threshold that triggers IRMAA Medicare premium surcharges, a real cost most pre-retirees never see coming.

How the Tax Timing Works, and Why It’s the Whole Ballgame

The entire Roth IRA vs Traditional IRA debate reduces to one question: when do you want to pay taxes? With a Traditional IRA, you contribute pre-tax dollars, growth is tax-deferred, and you pay ordinary income tax on every dollar you withdraw in retirement. With a Roth IRA, you contribute after-tax dollars, growth is tax-free, and qualified withdrawals in retirement cost you nothing.

The Pre-Tax vs After-Tax Math

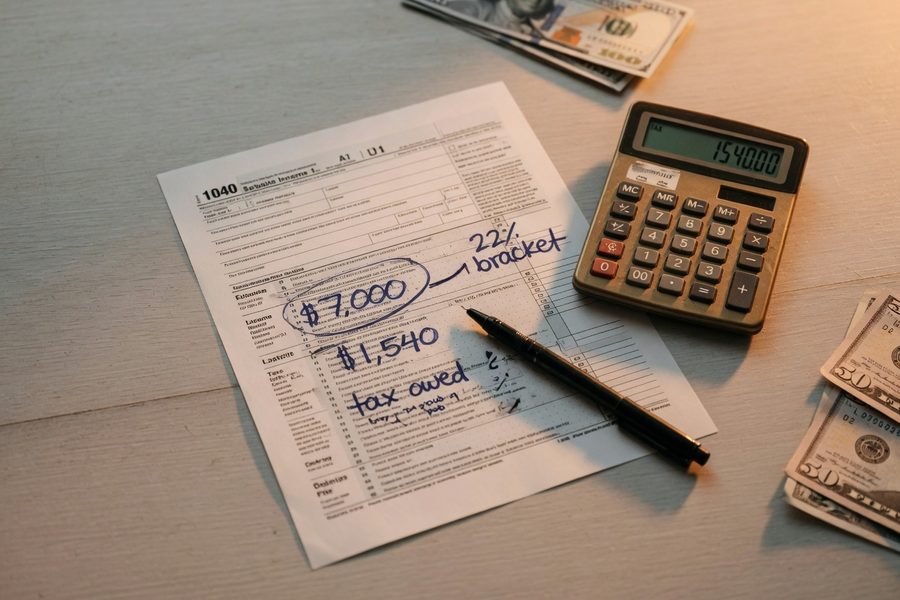

Here’s a worked example worth running. Say you’re in the 22% federal bracket today and contribute $7,000 to a Traditional IRA. You save $1,540 in taxes this year. That same $7,000 in a Roth costs you the full amount upfront with no deduction. Both accounts grow identically over time, the difference shows up entirely at withdrawal. If you’re still in the 22% bracket at retirement, the outcome is a wash. But if rates rise to 25% or higher (a real possibility if TCJA provisions expire), the Roth wins by a meaningful margin on every dollar withdrawn.

Tax-deferred growth sounds powerful until you realize you’ve been deferring a liability, not eliminating it. That’s the frame most people miss.

What I see in practice: Readers often assume their retirement income will be lower than their working income. That’s frequently wrong. Between Social Security, RMDs from a 401(k), and other income sources, many retirees land in a higher effective bracket than expected, and wish they had more Roth money available.

“When I work with accountants, their three favorite words are defer, defer, defer.”

Pope’s point cuts both ways. Deferral is a legitimate strategy for high earners who will genuinely step down in income. For everyone else, it’s often just postponing a higher bill.

2026 Contribution Limits, Income Rules, and Who Qualifies

Both accounts share the same annual contribution ceiling. For 2026, the limit is $7,000 if you’re under 50, and $8,000 if you’re 50 or older, per the IRS. Where the accounts diverge sharply is eligibility.

Roth IRA Income Limits

Roth contributions phase out based on your modified adjusted gross income (MAGI). For single filers in 2026, the phase-out runs from $150,000 to $165,000. For married filing jointly, it runs from $236,000 to $246,000. Above those ceilings, you cannot contribute directly to a Roth IRA. High earners in that position often turn to the backdoor Roth strategy: contribute to a non-deductible Traditional IRA, then convert to Roth. It works cleanly if you have no pre-existing Traditional IRA balance; if you do, the pro-rata rule complicates the math significantly.

Traditional IRA Deductibility

Anyone with earned income can contribute to a Traditional IRA, but the deduction isn’t guaranteed. If you or your spouse has access to a workplace retirement plan like a 401(k), the deduction phases out at moderate income levels. For single filers covered by a workplace plan, that phase-out starts at $79,000 MAGI in 2026. Above $89,000, the deduction disappears entirely. If you’re above those thresholds, a Traditional IRA contribution is still allowed, it just becomes non-deductible, which weakens the core argument for choosing it over Roth.

| Feature | Roth IRA (2026) | Traditional IRA (2026) |

|---|---|---|

| Contribution Limit (under 50) | $7,000 | $7,000 |

| Contribution Limit (50+) | $8,000 | $8,000 |

| Income Phase-Out (Single) | $150,000 – $165,000 | $79,000 – $89,000 (if covered by workplace plan) |

| Income Phase-Out (Married, Joint) | $236,000 – $246,000 | $126,000 – $146,000 (if covered by workplace plan) |

| Tax on Contributions | After-tax (no deduction) | Pre-tax (deductible, if eligible) |

| Tax on Qualified Withdrawals | None | Ordinary income tax |

| Required Minimum Distributions | None (owner’s lifetime) | Starting at age 73 |

| Early Withdrawal of Contributions | Penalty-free anytime | 10% penalty + taxes before 59½ |

Withdrawals and RMDs: Where Roth’s Flexibility Compounds

Roth accounts carry a structural advantage in retirement that most savers underestimate until they’re living it. Traditional IRAs force you to start taking RMDs at age 73, whether you need the money or not. Those distributions are taxable income, which can push you into a higher bracket, trigger taxation of Social Security benefits, and trip IRMAA surcharges that add hundreds of dollars per month to your Medicare Part B and Part D premiums.

Roth IRAs have no RMDs during the original owner’s lifetime. You can let the account compound indefinitely, and your heirs inherit a tax-free asset. For savers who expect to have more income in retirement than they need, or who want to preserve wealth across generations, that flexibility has real dollar value. If you’re already thinking about how retirement income affects your broader financial picture, the post on prioritizing retirement savings over college funding covers related tradeoffs worth reading.

Where this gets tricky: IRMAA is the hidden tax almost no one plans for. Roth withdrawals don’t count as income for IRMAA purposes; Traditional IRA withdrawals do. For a couple with substantial Traditional IRA balances, that distinction can mean $400 or more per month in added Medicare costs at exactly the time when healthcare spending peaks.

Roth IRA vs Traditional IRA: Your Current Bracket Is the Core Decision

If you’re in the 12% or 22% federal bracket today, the Roth is the better default, pay a known, relatively low rate now rather than risk a higher rate later. The math is especially favorable right now because the Tax Cuts and Jobs Act’s individual rate reductions are scheduled to expire after December 31, 2025. Unless Congress acts, the 22% bracket reverts to 25% and the 24% bracket reverts to 28%. That means the tax environment in 2026 and beyond may already be more expensive than what you’re calculating with today’s rates.

When Traditional Actually Wins

The Traditional IRA earns its spot for savers in the 32%, 35%, or 37% federal bracket who have strong reason to believe their retirement income will be significantly lower. A surgeon at peak earnings who plans to retire on a modest fixed income has a genuine case for deferral. So does someone with a variable-income year, a layoff, a career break, or an early retirement phase before Social Security kicks in. Those low-income windows are ideal for Roth conversions, moving Traditional IRA or 401(k) money into the tax-free bucket at a known favorable rate. If your income is already inconsistent, the post on jobs that pay $19 or more per hour may also be relevant as you plan your total income picture.

One more angle worth flagging: state income taxes matter. Several states, including Pennsylvania and Illinois, exempt Traditional IRA withdrawals from state tax, which tilts the math back toward deferral for residents of those states. Others tax all retirement income at full rates. Your state’s treatment of IRA distributions should factor into the calculation, not just the federal rate.

What clients often miss: Contributing to a Traditional IRA can reduce MAGI enough to qualify for the Saver’s Credit or other income-tested credits in the contribution year. That’s a real benefit, but it’s one-time, while Roth’s tax-free growth is permanent. Don’t let a short-term credit override a long-term structural advantage.

For readers just getting started with investing generally, this guide to starting with zero investing experience provides helpful foundational context before you commit to a specific account type.

Where This Recommendation Falls Short

The Roth-first stance I’ve argued above is not right for everyone. Let me be direct about where it breaks down.

The biggest drawback of the Roth is cash flow. When you contribute $7,000 to a Roth, you’re paying taxes on that money this year, which means you’re effectively contributing more than $7,000 out of pocket (you’re funding the account with after-tax dollars). For someone living paycheck to paycheck or carrying high-interest credit card debt, the immediate tax relief of a Traditional IRA deduction is worth taking. Paying down 20% APR debt beats the long-run value of tax-free growth almost every time.

The case for Traditional is also stronger than I’ve implied for anyone in the 24% bracket or above who has a documented plan to draw down substantially in retirement. A couple planning to live on $60,000 a year in retirement will pay very little tax on those Traditional IRA withdrawals. The Roth premium they paid upfront may never recoup itself.

There’s also an uncertainty problem that cuts against the Roth. Tax rates could fall. Congress could expand Traditional IRA deductibility or change Roth rules. Required minimum distribution rules have already shifted once (the SECURE Act moved the age from 70½ to 72, and SECURE 2.0 moved it again to 73). Betting heavily on any one account type is a concentration risk. Holding both, a Traditional 401(k) at work and a Roth IRA, gives you flexibility to manage taxable income in retirement regardless of what the tax code looks like in 20 years.

The catch is that most savers can’t fully fund both. That’s where the bracket test comes back: the best single account for you is the one that matches your current rate against your best estimate of your future rate, with a small bias toward Roth given the TCJA expiration risk. But “small bias” isn’t “always Roth.” Context changes the answer.

How We Sourced This

This article draws primarily from the IRS’s official guidance on Traditional and Roth IRAs, which covers contribution limits, income phase-outs, RMD rules, and withdrawal requirements as updated for the 2026 tax year. Household ownership statistics come from the Investment Company Institute’s 2025 IRA ownership data release, which reflects mid-2024 survey results. The Devin Pope quote is sourced from an Acorns editorial published at acorns.com. Contribution limit figures and MAGI phase-out ranges reflect IRS announcements applicable to the 2026 tax year. IRMAA and Social Security benefit taxation thresholds are drawn from Social Security Administration and Medicare.gov published guidelines. This article was written and verified; readers should confirm current-year limits directly with the IRS before contributing.

Frequently Asked Questions

Can I contribute to both a Roth IRA and a Traditional IRA in the same year?

Yes, but your combined contributions across both accounts cannot exceed the annual limit, $7,000 under age 50, or $8,000 at 50 or older. Splitting contributions between the two is a legitimate strategy for tax diversification if you’re within the income thresholds for both.

What happens to my Traditional IRA if tax rates rise after the TCJA expires?

Every dollar you eventually withdraw gets taxed at whatever ordinary income rate applies in that year. If brackets increase after the TCJA sunset, your deferred tax liability grows with them. That’s why many planners recommend converting some Traditional IRA balance to Roth during the 2025–2026 window while current rates still apply.

Does a Roth IRA affect eligibility for government benefits?

Roth IRA assets are generally counted in net worth calculations for some programs, but Roth withdrawals don’t appear as income on your tax return, which matters for income-tested benefits. Traditional IRA withdrawals, by contrast, count as ordinary income and can affect benefit eligibility, IRMAA surcharges, and Social Security benefit taxation. If you’re tracking federal assistance programs, the discussion of 2026 poverty guideline changes provides useful context on income thresholds.

Can I withdraw Roth IRA contributions before retirement without penalty?

Contributions, not earnings, can be withdrawn from a Roth IRA at any time, at any age, without taxes or penalties. Earnings are subject to the 5-year rule and the age-59½ requirement for a penalty-free qualified withdrawal. This makes Roth accounts more flexible as an emergency backstop than Traditional IRAs.

What is the backdoor Roth IRA, and who needs it?

The backdoor Roth is a two-step workaround for high earners who exceed the Roth income limits: contribute to a non-deductible Traditional IRA, then convert it to a Roth. It works cleanly if you have no other Traditional IRA balances. If you do, the pro-rata rule means part of your conversion will be taxable, reducing the strategy’s efficiency.

At what income level should I seriously consider a Traditional IRA over Roth?

A Traditional IRA becomes the stronger choice when your current federal bracket is 24% or higher and you have a credible plan to withdraw at a lower rate in retirement. Below 24%, the Roth’s permanent tax-free growth typically outperforms the upfront deduction, especially given current TCJA expiration risk.

Sources

- IRS, Traditional and Roth IRAs (Official Rules and Limits)

- Investment Company Institute, IRA Ownership in the United States, 2025 Release

- Acorns, Roth IRA vs. Traditional IRA: Which Is Right for You?

- Medicare.gov, Understanding Medicare Costs

- IRS, Topic No. 451: Individual Retirement Arrangements (IRAs)